Introduction

Since crushing consensus EPS estimates by an ungodly 660% two weeks ago, TravelCenters of America (TA, Financial) has seen its price rise by ~18%. Analysts at Zacks have rated the stock a strong buy, and have given the stock an A rating in every category: value, growth, and momentum. In fact, Zacks is so bullish on the stock that last week it deemed TA its "Bull of the Day."

TravelCenters of America is a full-service national travel center that offers diesel and gasoline fueling services, restaurants, heavy truck repair facilities, convenience stores, and other services. While diesel and gasoline sales account for over 80% of the company's revenue, the other services account for a disproportionate amount of the company's margin. With a growing chain of over 575 restaurants, 34 convenience stores, and 240 truck-repair facilities, the company serves hundreds of thousands of customers nationwide every month and growth in these areas will only continue to improve the company's bottom line. Due in large part to the sticky nature of retail gas price drops (retail pumps take some time passing the savings to the consumer), TravelCenters was able to generate huge fuel profits last quarter to the tune of a 65% increase year over year. With all of the free cash flow generated from this event, we feel that TA has positioned itself well for further growth in the coming year.

Before we begin our analysis, investors should know a little about our analytical style. Our analysis focuses on identifying and exploiting stock market "anomalies." We've identified a variety of different academically tested metrics that have a long track record (over +50 years) of predicting stock returns. We'll provide links to the academic papers that fuel our analysis as we progress through the report so you can see for yourself whether to trust the metrics we rely on. Click here to see a detailed breakdown of the prominent academics (many of whom manage billions of dollars) and their contributions to the field of stock research that we draw inspiration from.

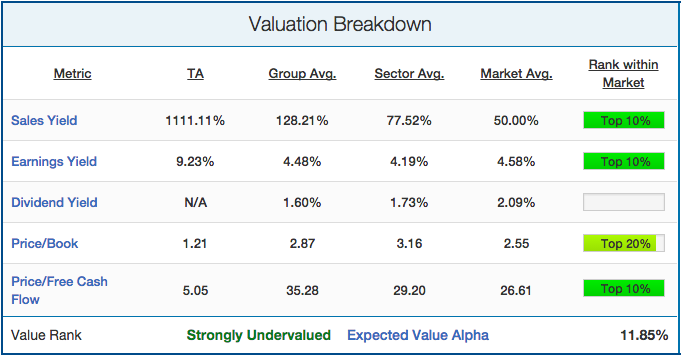

Value Breakdown

We'll start with an analysis of TA's valuation profile, looking at five valuation metrics each with a strong predictive ability. This is important to consider as Nobel Laureate Eugene Fama showed that "value stocks have higher average returns than growth stocks." The "value" anomaly is the strongest and most consistent edge in the market, as study after study has shown that cheap stocks beat expensive stocks. TA's valuation profile is shown below:

(click to enlarge)

Other than its lack of dividend, TA is attractive in every one of our value metrics. Its sales yield, although also an indicator of its traditionally low margins is extremely high at 1111%, well above the specialty retail group average of 128%. TA's most impressive value indicator is its earnings yield (inverse of the P/E ratio) that, at 9.23%, is over twice the market average of 4.58% and the highest of all stocks in the specialty retail group. Though TA continues to reinvest its free cash into the purchasing of assets - $75 million to be spent this year on 48 new locations - it's still undervalued for the amount of free cash that it generates. The company trades at only 5 times TTM free cash, which, to put in perspective, is in the 96th percentile of the market and the 97th percentile of the consumer discretionary sector. Finally, the company is also cheap from a book value perspective, trading at only 1.21 times its book value, less than half of the market average of 2.55. From these metrics it's clear that TA is grossly undervalued in today's expensive market.

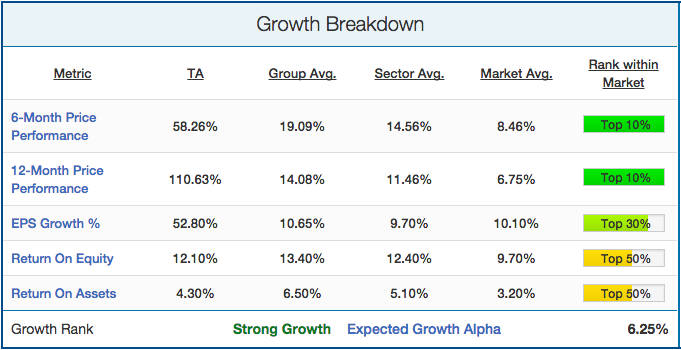

Growth Breakdown

There are a variety of different growth metrics that have been shown to predict stock returns. Most important among them is price momentum. Winning stocks keep winning (based on six-month price performance), and losing stocks keep losing. As outlined in James O'Shaughnessy's book "What Works on Wall Street," EPS growth and return on equity/assets also were shown to have predictive ability, albeit to a lesser extent. TA's growth breakdown is shown below:

(click to enlarge)

There's no question that TA is a hot pick at the moment. While the entire specialty retail group benefited from the drop in gas prices and the recovering economy - to the tune of a near 20% average price gain in the last 6 months - TA still managed to stand out by nearly tripling its group average. Its 58% price gain was in the top 5% of its group, sector, and the market as a whole. Even more impressive is that this momentum has been sustained for an entire year. At a +110% return, TA has been one of top 55 NYSE or NASDAQ stocks to own over the past 12 months.

While many investors may see this price gain as a signal of the company being overvalued, we feel that this momentum is a sign that investors have begun to seriously consider the stock and its value, and that the momentum will only continue. Its EPS growth of 52.8% over 2014 is a sign that the company is headed in the right direction.

Qualitative Analysis

While we prefer to focus our analysis on metrics proven to correlate to returns across the entire market, we understand that every stock represents a unique business with unique growth catalysts and potential risks. We will discuss these further in the coming section, but before that, I'd also like to highlight how the major institutions have been playing the stock.

With an 11% gain in institutional ownership in the past 3 months, it's clear that the institutions recognize the value and growth that TA presents. It's also valuable to note that despite its recent price appreciation, short sellers don't feel that the stock has reached its peak, as the short float is only 3.67%, well below the 5.62% average in its group.

RDG Capital Fund Management is a major shareholder who recently announced that it delivered a letter to TA's Board of Directors indicating that the fair market value for the stock is between $24-27 per share - a 45-60% increase on the current price. RDG suggested that TravelCenter conduct a sales leaseback of the company's significant real estate assets (which continue to grow) and spin off the company's growing, truck-repair services segment to realize its full value. In essence, RDG is suggesting that these two segments alone are worth more than the current +$650M market cap.

With fuel prices in both gasoline and diesel remaining persistently low, we feel that TravelCenter will continue to boast high profit margins. The low fuel prices, combined with the current economic recovery, also make travel more affordable and should increase the foot traffic at TravelCenter locations. This may be why same store sales have been increasing over the past year despite all of the expansions.

Investors may be concerned about all of the capital expenditure taking place, especially considering the somewhat nefarious reputation of Barry Portnoy - the managing director of the company - who is known for mismanaging, or managing in his own self-interest, his Equity Commonwealth REIT. However, these fears may be overblown, as his relationship with TA is slightly different. As opposed to collecting a fee on all assets (thus incentivizing him to keep acquiring despite the ROA), the REIT is paid lease payments on a fair market value basis. With the added attention brought on by the Equity Commonwealth REIT lawsuit, we feel that Barry Portnoy is less of a risk than is being potentially priced in.

In all, we feel that TA will carry its momentum into the coming months as investors recognize the value and continued growth taking place at the company. We feel that the stock will continue to outperform the S&P 500 over the coming months, and that now is as good a time as ever to take a long position in the stock.