After peaking at $80 per share last year, Qualcomm (QCOM) has had a rough go with the stock down over 30%. Qualcomm management had to deal with multiple challenges including an investigation of licensing business practices by China and the loss of Samsung Galaxy S6 smartphone business.

Figure 1 (Source: Morningstar.com)

However QCOM remains the dominant IP force in mobile phones and virtually all mobile phone manufacturers who use 3G or 4G technologies have to pay royalties of 3% to 5% per phone to QCOM. This stream of royalties will remain for many years to come. Qualcomm also spends over $5 billion a year on R&D ensuring that it will continue to build its technological moat.

One of the greatest investors of all time, Peter Lynch, has said that "insiders might sell their shares for any number of reasons, but they buy them for only one: they think the price will rise." For the first time in two years, multiple key insiders have stepped up to acquire shares of the company at market prices. The CEO, CFO and a couple of directors have acquired shares.

Figure 2 (Source Morningstar.com)

| Insider | Position | Date | Buy/Sell | Shares | Shares Owned Following This (Direct & Indirect) | Trade Price ($) | Cost ($1000) |

Price Change Since Trade (%) | Share Ownership Details |

| VINCIQUERRA ANTHONY J | Director | 2015-09-11 | Buy | 1,000 | 1,567 | $54.7 | 54.7 | 0.51 | 1,000 (by Trust 2) 567 (by Trust) |

| MOLLENKOPF STEVEN M | CEO | 2015-07-28 | Buy | 15,815 | 159,934 | $63.31 | 1001.2 | -13.16 | 159,934 (by Trust) |

| Davis George S | EVP & CFO | 2015-07-28 | Buy | 8,100 | 58,463 | $62.34 | 505 | -11.81 | 58,463 (by Trust) |

| MCLAUGHLIN MARK D | Director | 2015-07-27 | Buy | 5,650 | 5,650 | $61.63 | 348.2 | -10.79 | 5,650 (by Trust) |

Source: Gurufocus.com

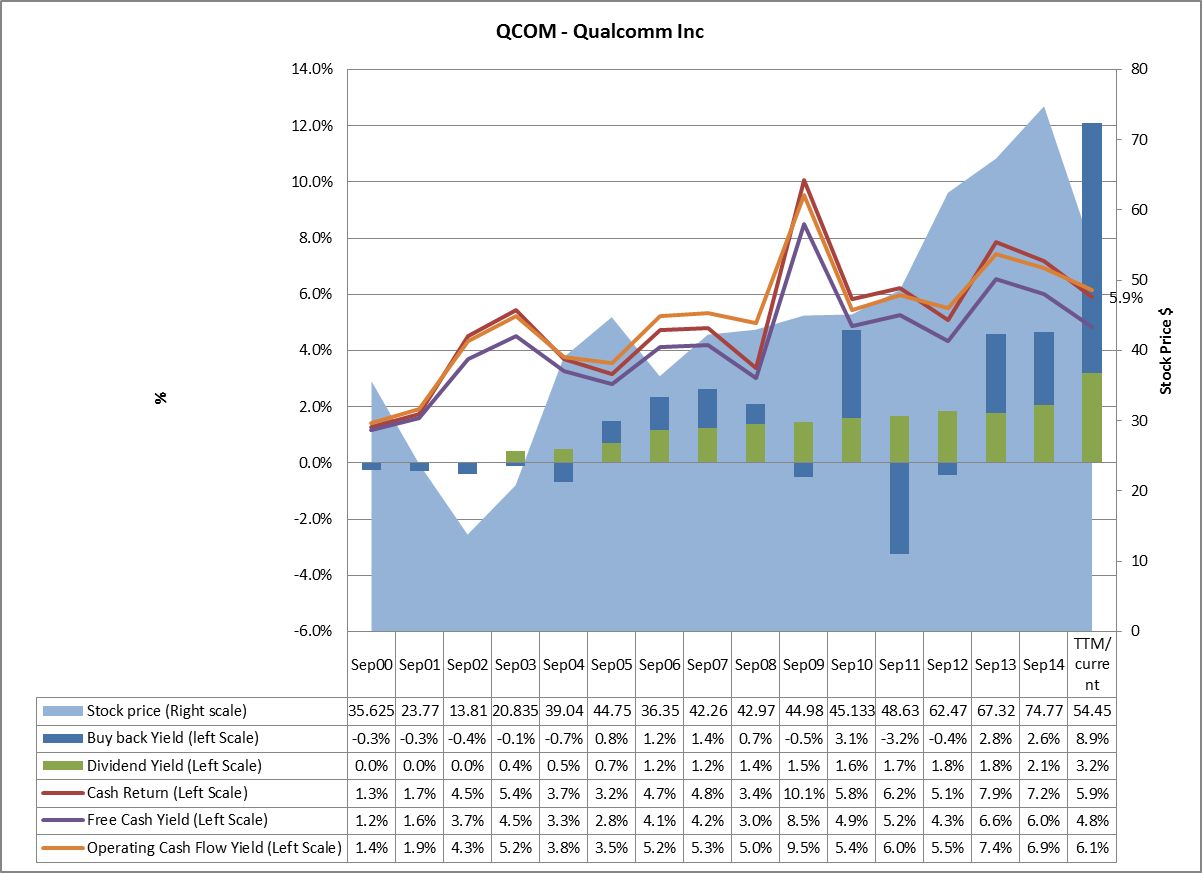

In addition, QCOM's dividend yield has reached 3.2% . Recently Qualcomm issued $10 billion in debt to buy back stock. This should put positive pressure on stock price in the months ahead by reducing the company's float. The report indicates that the company issued the debt in eight parts. Two floating rate notes of $250 million each are due in 2018 and 2020. The fixed rate notes have interest rates ranging from as low as 1.4% on $1.25 billion due in 2018 to as high as 4.8% on $1.5 billion due in 2045. This compares favorably with a cash return of 5.9% which the company generates from operations. The $10 billion debt is not really debt but balances out cash held abroad, so even after the debt issuance, QCOM will remain essentially debt free on a net basis. Plus most of this $10 billion is coming back to shareholders. Qualcomm has bought back almost 9% of its stock in the past 12 months.

All this would indicate that QCOM stock should be good value in the medium to long term.

Figure 3

Valuation

As evident from the table below (sourced from Morningstar.com) Qualcomm's stock is currently trading at or new 5 year low multiples.

Current valuation

| Â | QCOM | Industry Avg | S&P 500 | QCOM 5Y Avg* |

| Price/Earnings | 14.9 | 20.2 | 18.4 | 21.1 |

| Price/Book | 2.6 | 2.4 | 2.6 | 3.3 |

| Price/Sales | 3.4 | 2.3 | 1.7 | 5.9 |

| Price/Cash Flow | 16.7 | 9.5 | 11.0 | 15.7 |

| Dividend Yield % | 3.3 | 2.4 | 2.3 | 1.7 |

| Price/Fair Value | 0.8 | - | - | - |

Data as of Sept. 18, *Price/Cash Flow uses 3-year average.

Forward valuation

| Â | QCOM | Industry Avg | S&P 500 |

| Forward Price/Earnings | 11.7 | - | 17.6 |

| PEG Ratio | 1.5 | - | - |

Conclusion

Qualcomm stock appears to be a excellent buy at an excellent price, further validated by multiple inside purchases and supported by company stock buybacks.