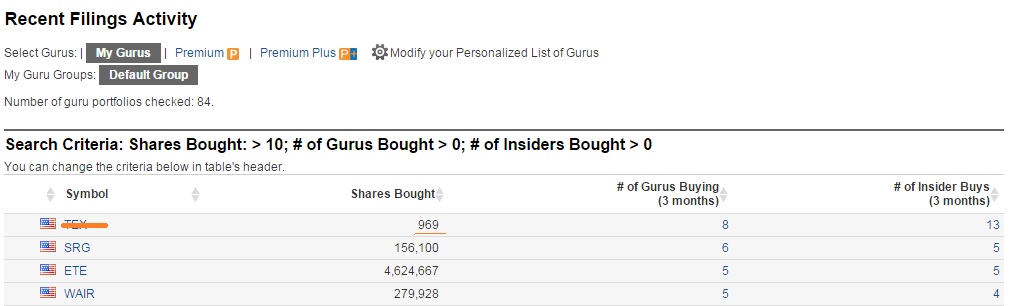

GuruFocus has various tools and screeners available to make the quest for your next great investment a little bit more efficient. A tool of which I am fond is the Double Buy screen. By employing it you can easily screen a list of stocks that have been double tapped by both gurus and insiders. Both types of events tend to trigger my interest, but when they occur simultaneously it is time to pay close attention. I regularly review the list, and these are currently the top three stocks that come up on the screen:

Source: guru screen, edited by author

Terex Corporation

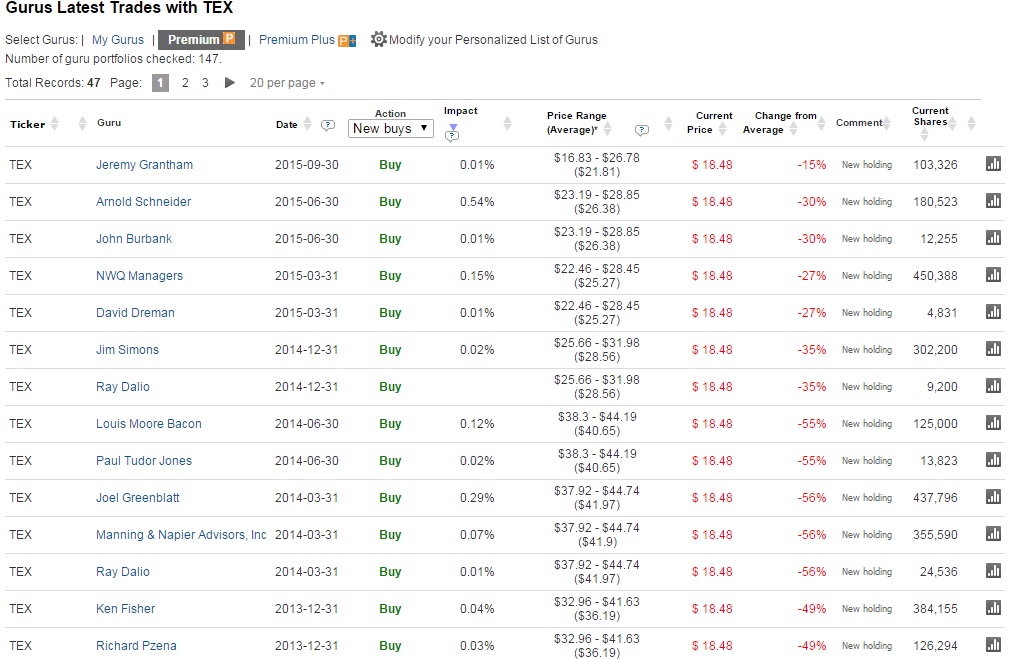

Terex Corporation (TEX, Financial) calls itself a lifting and material handling solutions company. Basically it makes all kinds of equipment that lift stuff, like cranes and aerial platforms but also less commonly seen types of equipment. The company was founded in 1925 and is based in Westport, Connecticut. I’ll discuss it only briefly because I disqualify it from this article. It has the most guru interest of all companies on the list over the time period and also a high number of insider buys but these insider buys only added up to less than $20,000 worth of shares. That’s why I’m discounting the signal value of those buys heavily.

The impact of the trades to their respective portfolios is almost negligible. Considered that the company is only $2 billion in size, this isn’t surprising, but it decreases my confidence in the value of the signal further. Based on the Guru interest it may deserve additional scrutiny but this article is about stocks with Guru AND insider buying and I don’t think it deserves a top 3 spot in such an article. However, it is in an interesting sector that may benefit from the recent passing of the U.S. highway bill.

Seritage Growth

Seritage Growth (SRG, Financial)Â is a REIT spun off from Sears Holding(NASDAQ:SHLD) with a market cap of approximately $1 billion. Its 200-plus properties are almost all occupied or co-occupied by Sears and K-Mart. Gurus who own it include: Bruce Berkowitz (Trades, Portfolio), Edward Lampert (Trades, Portfolio), Jim Simons (Trades, Portfolio),Paul Tudor Jones (Trades, Portfolio) and Murray Stahl (Trades, Portfolio).

Recently, Warren Buffett (Trades, Portfolio) bought it for his personal portfolio which I commented on last month in an article titled: What does Warren Buffett see in Seritage Growth Properties. The key to the thesis is (emphasis added):

The agreement between Seritage and Sears Holding doesn’t seem to lean very much on Sears Holding continuing to pay rent. The agreement says, among other things, that Seritage can take up to half of the gross square footage of any of its properties and release this space to a third party. It can also kick out Sears entirely under some circumstances where it can make much more money.

The current rent paid by Sears is on the low side of the spectrum, not surprising given the poor state of its operations. I think Buffett’s master plan entails that either the turn-around at Sears gains traction at some point, and when leases have to be renewed, better deals can be negotiated, but he also wins if Sears fails or better tenants can be found by Seritage. Because REITs pay out so much and pay so few taxes, a in-built lever for growth is much more valuable than it is in regular companies.

Because of great respect for Buffett and while spending time trying to figure out what he sees in Seritage Growth Properties I have come to like this name but just like Terex I could have disqualified it from this article. The insider buying is being done by Bruce Berkowitz (Trades, Portfolio) and he is also a guru! Therefore the signal isn’t as strong as it could be. At 1.35x book value and with considerable room to improve operations, there is quite some upside. With its $1 billion in long term debt and $173 million of EBITDA there is definitely quite a bit of leverage but given the nature of revenue it appears manageable.

Energy Transfer Equity

Energy Transfer Equity (ETE, Financial) is a partnership owning and operating natural gas gathering systems, pipelines and processing facilities. It sports a market cap in excess of $10 billion, which is how the market values 71,000 miles of pipe. Going by construction costs reported in 2014 the replacement value of that amount of pipe on land should be in the $100 billion ballpark although construction costs can be volatile. With $35 billion in debt that means the company trades at approximately 50% of the replacement value of its pipeline assets. Leaving other assets outside of consideration, debt looks very high compared to EBITDA so that could be a problem, but so far the company hasn’t revoked its 8% dividend which now amounts to an 8% yield. Richard Perry (Trades, Portfolio), Andreas Halversen, Ronald Muhlenkamp (Trades, Portfolio), Jim Simons (Trades, Portfolio) and Daniel Loeb have recently bought in. Insiders have been buying up stock worth more than $50 million.

Wesco Aircraft Holdings

Wesco Aircraft Holdings Inc. (WAIR, Financial) offers supply chain management services to the aerospace industry. The company offers services like quality assurance, kitting, just-in-time (JIT) delivery and point-of-use inventory management. The company supplies in excess of 575,000 SKUs, like hardware, chemicals, electronic components, bearings, tools and machined parts. Customers are locked up under long-term contracts or agreements. Aircraft parts and supplies have to comply with rigorous standards and once products are approved and being used by customers switching costs are quite large. This is an industry well known for its advantageous competitive advantages. Not surprisingly it is owned by gurus like Wallace Weitz (Trades, Portfolio) who favor these traits. Weitz most recently commented on the investment in the Q1 2014 report:

The company should benefit from the multiyear commercial aerospace build-out that is under way. We expect this tailwind to provide visible growth through at least 2017. Wesco also has an opportunity to provide more services to large defense contractors as funding pressures force the industry to become more efficient. If the company can improve margins along the way, we think the resulting earnings growth could provide reasonable-to-good return potential for the stock.

Other gurus owning the stock include Joel Greenblatt (Trades, Portfolio), Chuck Royce (Trades, Portfolio) and Richard Snow (Trades, Portfolio) among many others. Board member Thomas Bancroft is responsible for most of the recent insider buying. He is a managing partner at Makaira Partners LLC, which he founded in 2007. Previously he served as a portfolio manager at Plaza Investment Managers Inc., which is a, drumroll, wholly owned subsidiary and the internal investment division of GEICO – GEICO, of course, being a premiere U.S. auto insurance company and wholly owned subsidiary of Berkshire Hathaway Inc. (BRK.A, Financial)(BRK.B, Financial).

The company has only a $1.1 billion market cap and trades at a forward P/E of 9.7x which is low given its competitive advantage and the current average market valuation multiples which on average are in the low double digits. Its debt is close to $1 billion, which is somewhat worrisome given its low level of EBITDA at only $80 million, but cash flow levels paint a more favorable picture at around $130 million.