Polaris Industries (PII, Financial) is an impressive company with a track record of growth.

The company sells off-road vehicles (ORV), snowmobiles, motorcycles and parts and accessories for its products. For off-road vehicles, the company’s brands include Sportsman® ATVs, Polaris ACE®, RANGER®, RZR® and Polaris. For motorcycles, the company’s brands include Victory, Indian and the three-wheeled Slingshot.

Over the past year, the company’s stock price has dropped from $148 per share to the current price of $86 per share. You can see the stock price movement in the first chart below. The share price has fallen for a number of reasons.

- Management has guided that revenue will decline by 2% to 3% in 2016. Revenue in 2015 was $4.7 billion.

- The company has had a number of recall issues in the past year. The most prominent issue was when 160,000 units of its RZR off-road vehicles were recalled in April. That contributed to gross margins declining by almost 2%.

- Analysts were concerned about the company’s inventory levels in 2015. Management believes it is addressing the inventory levels effectively with better retail flow management and lean manufacturing initiatives.

Polaris has been covered by a number of articles on Seeking Alpha where most of the authors are bullish on the stock. On the other hand per Yahoo! (YHOO, Financial) Finance, the stock has 18.6% of its float short as of June 15.

I won’t rehash the Seeking Alpha articles in detail but simply put the bull narrative is that Polaris is a quality company with solid fundamentals, fixable short-term problems and a cheap valuation. I agree with the first two points but am not convinced about the valuation. From the the chart below, you can see the company’s impressive growth trend particularly in the last five years where revenues had a CAGR of 18.84%. Net income had a CAGR of 25.35% over the last five years from $147 million to $455 million.

Per GuruFocus, Polaris has the following trailing 12-month metrics:

- ROE of 45.0%.

- ROA of 18.2%.

- ROC of 77.8%.

- ROIC of 36.5%.

- PE ratio of 13.8.

- Price to FCF of 18.9.

- EV / EBIT of 9.3.

- Debt to Equity of 0.57.

SWAG at ORV total addressable market

Despite its admirable financials, I’m not sold on Polaris for the following reasons. It is largely a consumer cyclical company, and I’m not optimistic about the global economy. The picture below shows the percentage of sales that are for recreational use versus work use like farming and property maintenance.

My hypothesis is that its product cycle is wearing thin. In order to conclude that the ORV market doesn’t have a lot of runway left, I made a projection for ORV's total addressable market (TAM) in Polaris' main markets, the U.S. and Canada.

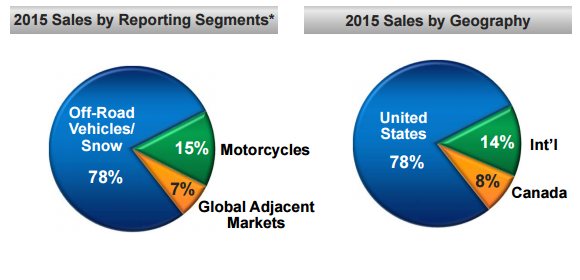

Let’s look at the company’s revenue makeup. The picture below shows 2015 sales by reporting segment and geography.

ORV revenues (excluding snowmobiles) were $2.75 billion in 2015 or 58% of total revenue. Eighty-six percent of total sales were from the U.S. and Canada which means about half of total sales can be attributed to the U.S. and Canada ORV segment.

For my SWAG on total addressable market for ORVs, I used motorcycles as a starting reference point. In this Motley Fool article, it reports that the Department of Transportation showed “8,410,255 motorcycles registered in the U.S. by private citizens and commercial organizations in 2011.” That comes out to 1 in 36 people in the U.S. I used that ratio for the most recent population figures for the U.S. and Canada. The combined population for these countries is about 355 million and if I divide that by 36, I’m guessing there are about 9.87 million motorcycles on the road for the two countries.

My assumption is that ORV TAM is less than motorcycles. From Motorcycle & Powersports News, I find that 2015 industry sales were “730,000 units [for] the grand total of motorcycle and ATV (all-terrain vehicles) sales combined.” (ATV and ORV are the same thing, different terms). Furthermore, ATV sales were 230,000 which makes motorcycle sales 500,000 for 2015. That’s a 2-1 ratio for motorcycles to ATVs.

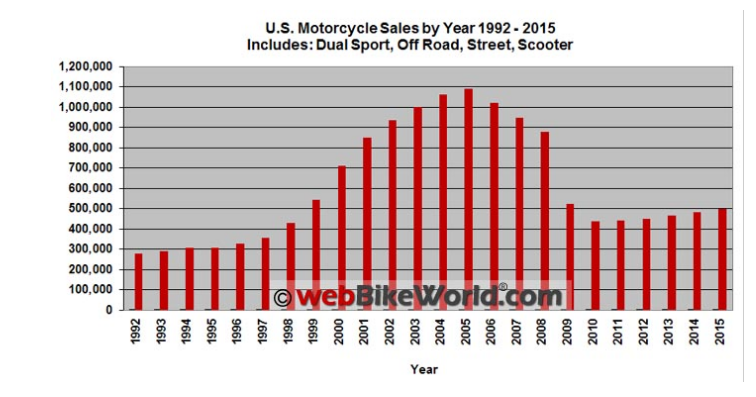

Below is a trend for U.S. motorcycle sales since 1992 from webbikeworld.com. It shows that motorcycle sales from 2010 to 2015 had a range from 450,000 to 500,000 per year.

Statista reports that ATV sales from 2012 to 2015 in the U.S. averaged about 230,000 per year. That means the sale of motorcycles to ATVs held relatively constant from 2012 to 2015 at a ratio of roughly 2-to-1. If I assume that the motorcycle-to-ATV ratio holds constant for total addressable market, the ORV TAM for the U.S. and Canada would be 9.87 million divided by 2, or 4.9 million units.

My next question is, “How long is the replacement cycle for ORVs?” My guess is at least 10 years. I base this assumption on the belief that most recreational ORV owners don’t drive their vehicles every day. My guess is that ORVs can last a long time and owners probably drive them occasionally on weekends. I feel that 10 years is a pretty safe assumption because the average age of cars on the road in 2015 was 11.5 years.

Let’s assume again that ORVs sold in the last 10 years averaged 230,000 in the U.S. That would mean 2.3 million ORVs were sold over 10 years out of a TAM of 4.9 million units or 47%. If you agree with the logic behind these numbers, you can take a glass half full or half empty interpretation. For me, 47% of TAM being purchased in the last 10 years leaves 2.6 million consumers (4.9 million - 2.3 million) who could potentially buy an ORV. These figures don’t imply that there is potential for a huge spike in sales.

Final thoughts

Polaris is a high quality company. However, the hypothesis is that its primary revenue driver will face weak demand in the next couple of years. I made a lot of assumptions which is unavoidable when making projections. I used very rough numbers to guess how much runway Polaris has in the USA / Canada ORV market which makes up 50% of their revenues. The numbers I have confidence in are the number of registered motorcycles and the sales trends for motorcycles and ORV’s. That’s because those numbers are straight from the Department of Transportation and industry trade publications. I took liberty with using the ratio of motorcycle-to-ORV sales to extrapolate ORV TAM. I also took liberty with using 10 years as the replacement cycle length.

My interpretation is that there is a ceiling on growth for the main product in its primary market. Polaris states that sales are partially correlated to the oil market. The CEO commented that sales from oil states declined 8% in the last earnings call. In addition, ORV revenue decreased 12% in the latest quarter. Compound that with the likelihood that the economy will remain sluggish, and there are more reasons for why sales will face headwinds over reasons for near-term optimism. There is no way to know how reasonable or inaccurate my projections are, but this is definitely a consumer discretionary stock which is at the mercy of customer whims. That makes it a high risk / high reward situation, and I would prefer to remain on the sidelines.

However, I acknowledge that this is a stock that could rise dramatically with an earnings beat. For those investors who are bullish on the economy and motor vehicles are in their circle of competence, I consider this a stock worth paying attention to. Would be interested in hearing other people’s views on if they disagree with my reasoning.

Disclosure: The author does not own any stocks mentioned in this article.

Start a free seven-day trial of Premium Membership to GuruFocus.