Buying into a hyper-growth stock is not at all an easy decision, irrespective of your investment experience. Hyper-growth stocks tend to have over-the-top valuations because investors and analysts both love to keep piling on the growth assumptions. But when something goes wrong, even if it’s temporary or for briefly, it will hit the stock as hard as it can.

This is something Under Armour (UA, Financial) investors witnessed during the first week of April as Under Armour stock saw a shock drop shortly after the earnings release – much like the meltdown its golf ambassador Jordan Spieth experienced when he had the Masters crown in his sight.

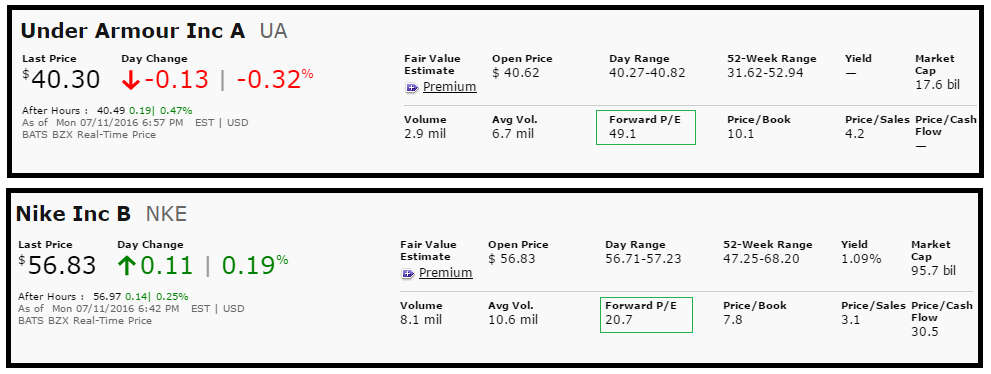

Despite the price correction, Under Armour is still trading at an eye-popping 49 times forward earnings as the market expects its growth story to continue forever. It might be right with respect to the growth prospects for the company, but at 4.2 times price to sales the company is well above the 3.1 mark where Nike is trading at the moment; and as the company gets bigger, I expect the the P/S ratio to correct itself closer to Nike’s.

Is growth potential still high?

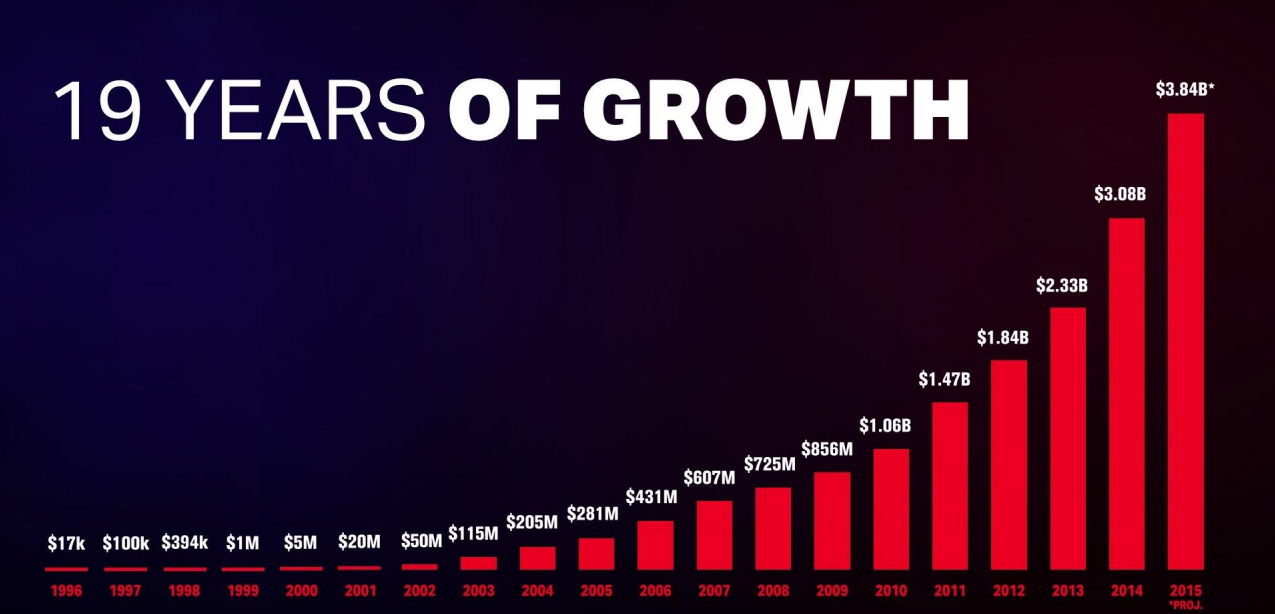

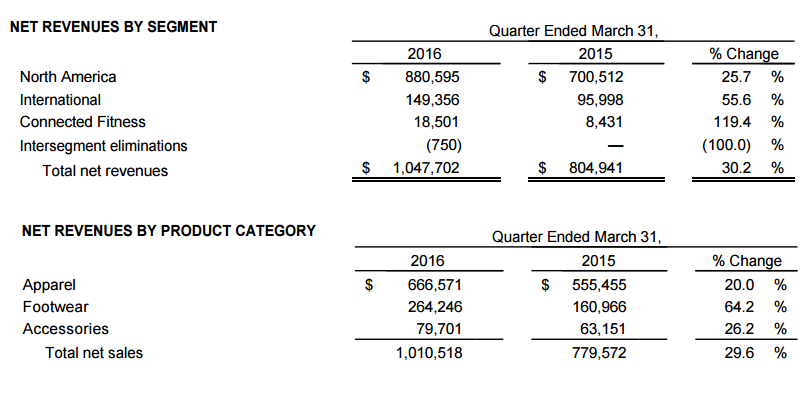

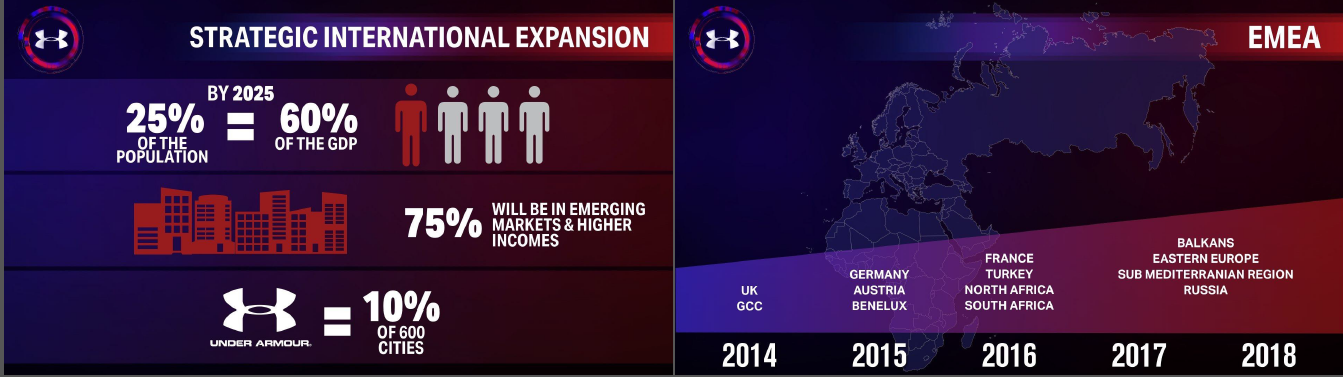

Under Armour’s revenue has grown nearly tenfold, from $431 million in 2006 to $3.96 billion in 2015, and the company is yet to open its account in some of the high volume emerging markets such as India. It is also just teeing off in China, which contributed 56% to Under Armour’s International growth during the first quarter.

CEO Kevin Plank during first quarter earnings call:

“Let's focus on how and where we are transforming and driving our brand. The first example is in China, where we have patiently built the foundation we know is needed to capture the enormous growth opportunity in that market. In this past quarter, we earned more revenue in China in 90 days than we did in the full year of 2014. We have grown judiciously in this critical market, building a solid foundation of core product with plans to add an additional 120 owned and partner brand health stores in Greater China throughout 2016.”

The international growth runway that's ahead of Under Armour – and a fast-growing footwear business – continues to make Under Armour an investor’s favorite. Why else would anyone be ready to pay nearly 50 times forward earnings for the stock?

So why did the stock to drop after the earnings release?

Under Armour’s stock declined after the earnings announcement mainly because of a not-so-enthusiastic forecast, which has become a norm after its stellar growth performance over the years.

“The company forecast that its gross margin will narrow by 100 basis points, hurt in part by the strong dollar. It expects 2016 sales to climb about 25% with operating income rising 23%."Â - Bloomberg

To invest or not to invest?

Under Armour does have plenty of room to add to its top line. Its international opportunity is huge, and it's already proved that it can give Nike a bit of a run for its money. Moreover, it's already displaced adidas (ADS, Financial) to capture the second position in the U.S. sportswear market –Â a trend that might spill over into other countries as well as Under Armour expands its footprint globally.

“Under Armour’s U.S. sales of footwear and apparel totaled $2.6 billion in the 11 months through Jan. 3, compared with $1.6 billion for adidas, according to data released Thursday by Sterne Agee and SportScanInfo” - Wall Street Journal

Even a small correction such as gross margin narrowing by 100 basis points is good enough to send the stock plummeting, and this not something that's going to change until it’s priced at a more reasonable level.

So the only way to invest in Under Armour right now is to dollar-cost average into a position that can be built over a period of time – and add more when the company goes through shocks, which I am sure will be plenty as the company moves into the next phase of growth.

Under Armour is a great company with proven business prospects, but to expect it to keep growing at the same rate now as when it was a $400 million earner is a bit unfair to say the least. Unfortunately, that’s what the current lofty expectations suggest.

If you are not a long-term investor, it’s best to avoid this hyper-growth company. If you are, then plan for a slow and steady accumulation as Under Armour moves from $4 billion in sales to $8 billion and beyond.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.