Salesforce (CRM, Financial) stock has roared through the last five years, pushing the company's market capitalization over $50 billion. Gone are the days when stock prices moved along with the earnings the company reported. These days as long as you can keep your top line moving, it's completely acceptable to even run into losses year after year.

In the last 10 years, Salesforce has rarely ever been profitable, and in the last five years alone, it has been expanding its losses year after year. But none of that has mattered as the stock is selling for nearly 7.6 times sales, a clear indication that the market expects the company to keep up its growth numbers. Let us take a closer look at why that is.

The Salesforce growth story continues

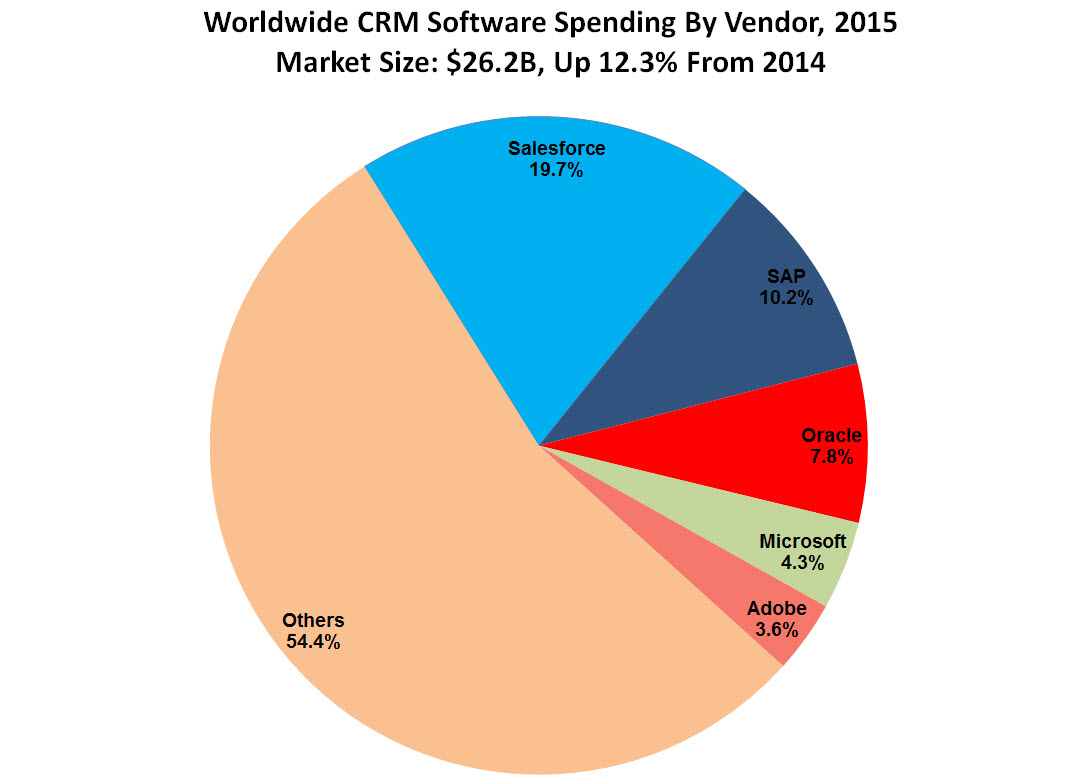

Salesforce is the leader of the Customer Relationship Management software market. As its name suggests, it has built strong expertise in building software that assists companies to take care of their entire sales lifecycle. This market was once tightly controlled by industry heavyweights Oracle (ORCL, Financial) and SAP (SAP, Financial), but Salesforce jumped in and ran away with a huge market share lead over both. To this day the company has managed to keep its deep-pocketed rivals at bay.

Source: Forbes

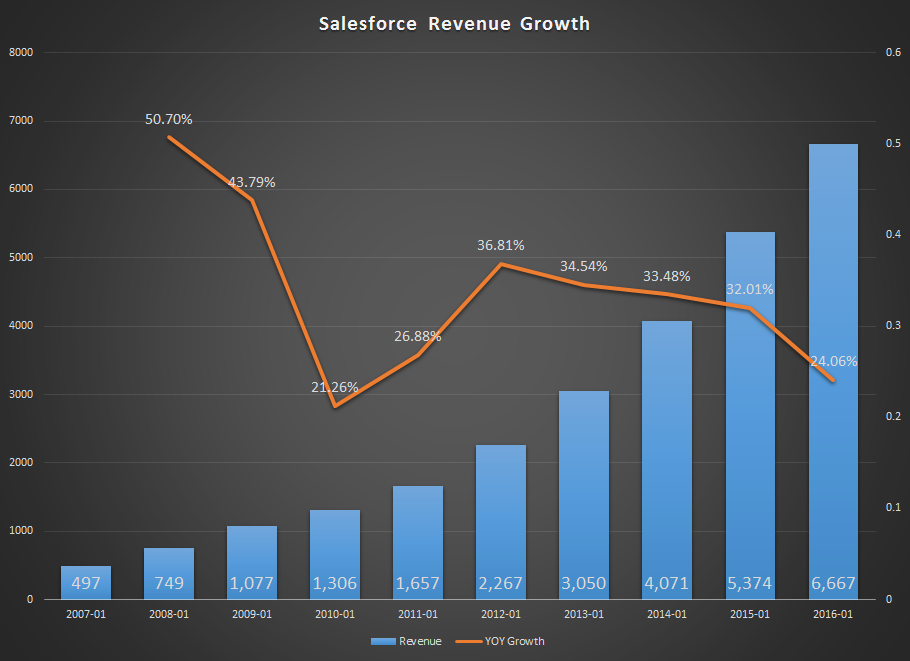

Despite its unprofitability, revenue growth has continued unabated at Salesforce for the last 10 years. Looking at the last four quarters’ results, that trend is highly likely to continue. But let’s explore the reasons for the top line growth.

Why growth is not always a good thing

The company has steadily expanded its portfolio of products, which it offers in the software-as-a-service mode. As it keeps adding more and more services to its list, it helps the company go wider and capture new audiences as well as deeper to increase revenue per client.

Within the sales and marketing niche, the company has gone both wide and deep, but it's spending proportionately more to acquire new customers and keep churn rates low on existing ones. More than 50% of its revenues go toward sales and marketing initiatives. Customer acquisition costs are sky-high, and that’s one of the reasons for its growing losses.

It’s a bit of a Catch-22 situation for the company. If it cuts back on marketing spending, it can show bottom line improvement but top line growth will inevitably slow down. On the other hand, if it continues to spend at the same rate to bring in new clients, then its bottom line will continue to bleed. The key point to note is that because the market has rewarded the company for being in this situation, Salesforce is more likely to continue this expense model.

As such this is an extremely difficult company to recommend as an investment. Salesforce’s strength in CRM is validated by the second and third position players in the segment. The potential is still huge for this market to grow, and investors seem to have given the company a free rein to pursue top line growth and not worry about profitability. But with $6 billion in annual revenues, its double-digit growth has to slow down at some point. When that happens, the valuation will inevitably have to be adjusted accordingly.

It’s a great company with great products and fantastic customer service practices, but there’s no way I can recommend the stock at this price point.

Disclosure: I have no positions in any of the stocks mentioned above and no intention to initiate a position in the next 72 hours.

Start a free 7-day trial of Premium Membership to GuruFocus.Â