Amazon will be reporting its first quarter 2017 earnings on April 27Â after the market close. Wall Street is expecting the retail giant to post consensus earnings per share of $1.13 and revenues of $35.31 billion -- growth of nearly 21% compared to the first quarter of 2016. Amazon’s net revenue grew 22% during the fourth quarter of last year and 27% for full fiscal 2016. Wall Street is obviously expecting the current growth trend to continue during the first quarter as well and to hit the top end of Amazon’s forecast for the first quarter.

Amazon forecasted net sales to fall in the $33.25 billion to $35.75 billion range, or to grow between 14% and 23% compared to the first quarter of 2016.

IBM (IBM, Financial) was the first cloud major to report its earnings for the current quarter. Big Blue saw its cloud revenue run rate jump by 61% during the quarter, while quarterly revenues from cloud touched $3.5 billion -- growth of 35% compared to the prior period. The cloud computing segment is still growing at strong double-digit rates despite the increasing competition. Amazon and Microsoft’s cloud revenues have been growing a bit faster than IBM’s, and Amazon should be able to keep that trend intact and post strong double-digit growth in its cloud segment.

Amazon’s North America retail segment has been growing fast, posting 22% revenue growth during the fourth quarter. With Prime membership steadily inching up, it will be a surprise if Amazon’s revenue growth in North America slips below the 20% mark. With all the big-box brick-and-mortar retailers shifting their attention towards e-commerce, customers across the country are increasingly getting used to the sophistication provided by direct home delivery. And, as the segment leader, Amazon will continue to eat into the mainstream retail market.

Amazon’s international revenues are growing as well, but not at the same speed as its cloud division or North America retail segment.

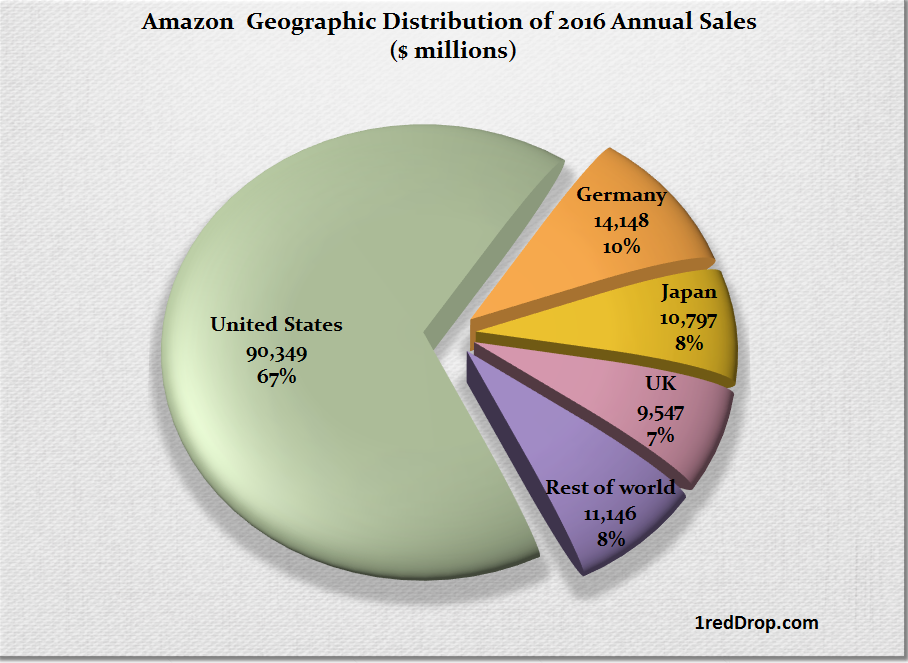

International revenues during the fourth quarter grew by 17.9%, the lowest of all three segments but not shabby by any measure. Amazon has operations in more than 10 economies around the world, but only a handful of them are at or above the $10 billion annual sales mark.

Amazon needs size and scale in each country before it can start thinking about profits, and Amazon’s International units will continue to operate at a loss, or stay barely profitable.

Amazon’s stock is up nearly 42% in the last 12 months, thanks to their solid growth numbers. The high profitability of AWS has added a lot more muscle to Amazon, allowing the company to invest with a bit more freedom, and the company is going all out to keep its sales numbers headed north inside and outside the U.S.

Even if the quarterly results turn out to be a damp squid, Amazon has already built diversified and growing revenue streams for the stock to shake that off and continue with its upward trend.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.