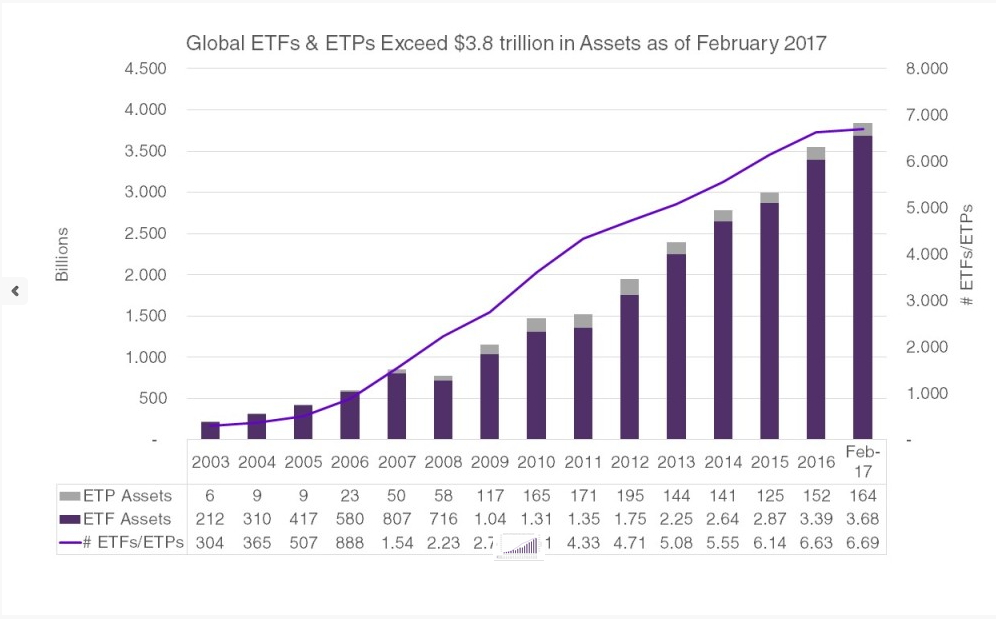

The idea behind the ETF Industry Exposure & Financial Services ETF (TETF) is simple: ETFs are the fastest-growing investment category ever. From a single fund, SPY, in 1993 ETFs now total over 6,000 different offerings.

ETFs have grown at over an annual rate of 19.4% over the last decade and now have more than $3.8 trillion in assets worldwide!!

Why not, first, design a passive index that tracks the biggest publicly traded ETF issuers, the exchanges that benefit from the highest volume of ETF trading, and the various service providers that serve the ETF industry and, second, create an ETF that tracks that index?

The first part was completed courtesy of the Toroso ETF Index. Rather than limit the index solely to those publicly traded firms that issue ETFs (the “fund sponsors”), Toroso includes the financial services firms that provide distribution, custodianship, liquidity and data as well as the actual exchanges that process a higher number of ETF trades.

The bad news is that, if you are looking for a pure play on ETF issuers, there is no index for that just yet. The good news is that you have far better diversification in an ETF that mirrors this index, which covers a lot of financial services providers as well.

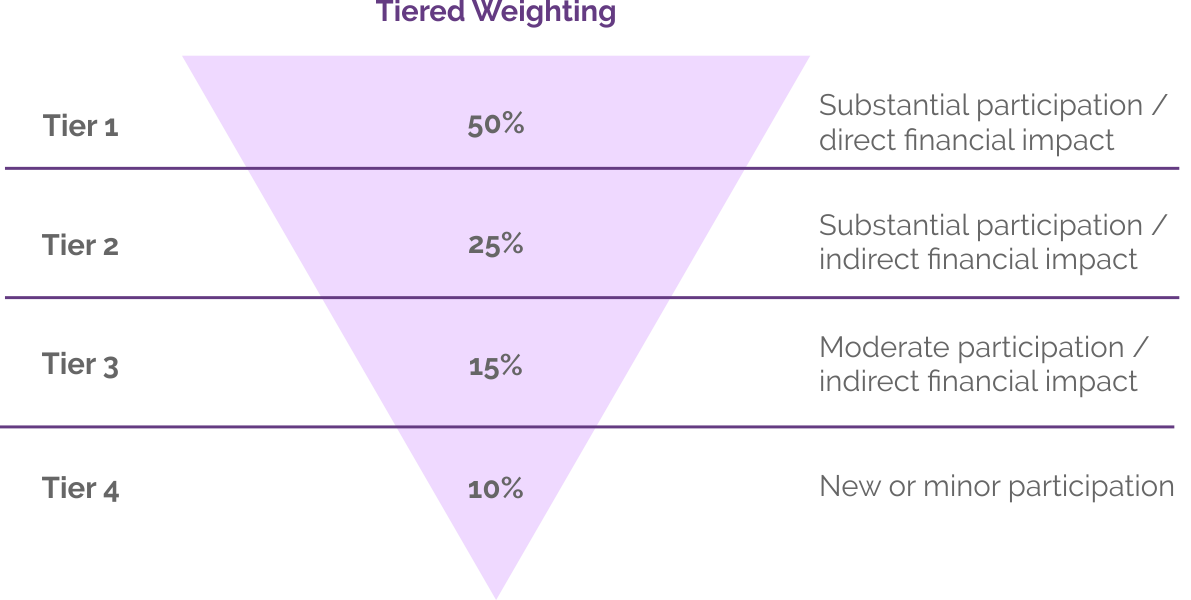

The index is constructed in such a way that fully 50% of the portfolio is comprised of those firms that have “substantial participation” in the ETF marketplace and enjoy a “direct financial impact” from that participation. This tier places 6.25% of the portfolio in each of eight major players:

- BlackRock (BLK, Financial).

- Schwab (SCHW, Financial).

- Invesco (IVZ, Financial).

- State Street (STT, Financial).

- Wisdom Tree (WETF, Financial).

- MSCI (MSCI, Financial).

- S&P Global (SPGI, Financial).

- CBOE Holdings (CBOE, Financial).

This equally weighted tier is designed to capture those companies with the purest connection to the growth of the ETF industry. (BlackRock alone, via its iShares subsidiary, has aggregated close to 40% of all U.S. ETF assets.) It also includes the CBOE, which is the dominant force in trading and indexing volatility and which derives substantial revenue from the ETF business.

The next 25% of the index is comprised of other companies that benefit from the growth of ETF trading but are not pure plays on the business. These firms still have “substantial participation” in the ETF marketplace but see a more “indirect financial impact” from their participation. Here we find seven companies that are equally weighted at 3.57% each. They are:

- DST Systems Inc. (DST, Financial)Â – an ETF sponsor.

- JPMorgan Chase & Co. (JPM, Financial)Â – an ETF sponsor.

- SEI Investments (SEIC, Financial) – a services provider.

- KCG Holdings Inc. (KCG) – a liquidity provider.

- Virtu Financial Inc. (VIRT) – A liquidity provider.

- Intercontinental Exchange Inc. (ICE) – an exchange.

- Nasdaq Inc. (NDAQ) – an exchange.

This tier includes firms like JPMorgan, an ETF issuer that also has banking, investment banking, credit cards and numerous other subsidiaries. KCG Holdings is an example of a company that is essential as a lead market maker and liquidity provider, but whose revenue from the growth of ETFs is only part of its primary business. It also provides execution and transaction services for all securities, not just ETFs.

The next tier also has seven companies, but these are weighted at just 2.14% each. These are firms with “moderate participation in the ETF industry with indirect financial impact to shareholders.”

These seven are:

- Ameriprise Financial Inc. (AMP) – an ETF sponsor.

- Northern Trust Corp. (NTRS) – an ETF sponsor.

- Virtus Investment Partners Inc. (VRTS) – an ETF sponsor.

- Bank of New York Mellon Corp. (BK) – a service provider.

- US Bancorp (USB) – a service provider.

- FactSet Research Systems Inc. (FDS) – an index and data provider.

- CME Group Inc. (CME) – an exchange.

The final tier, currently containing 15 companies, fill out the remaining 10% of the portfolio. Since they individually amount to less than a 1% impact to the index’s performance, I won’t list them all but this tier includes companies like Morningstar (MORN), TD Ameritrade (AMTD), Eaton Vance (EV) and Goldman Sachs (GS).

Finally, the index is rebalanced just twice a year, in June and December, and to be eligible for inclusion in the index, a company must have a free-float adjusted market cap of $200 million or greater for initial and ongoing index inclusion. To make sure there is adequate liquidity, constituent securities must also have three-month average daily turnover of a minimum of $1 million.

The only mutual fund, closed-end fund or ETF to create a product using the Toroso ETF Index (so far!) is the ETF Industry Exposure & Financial Services ETF, or TETF. Via TETF, we can enjoy all the benefits that ETFs offer, like improved liquidity, tax efficiency and increased transparency, but we can do so while holding a comprehensive basket of the biggest and best beneficiaries of the product itself.

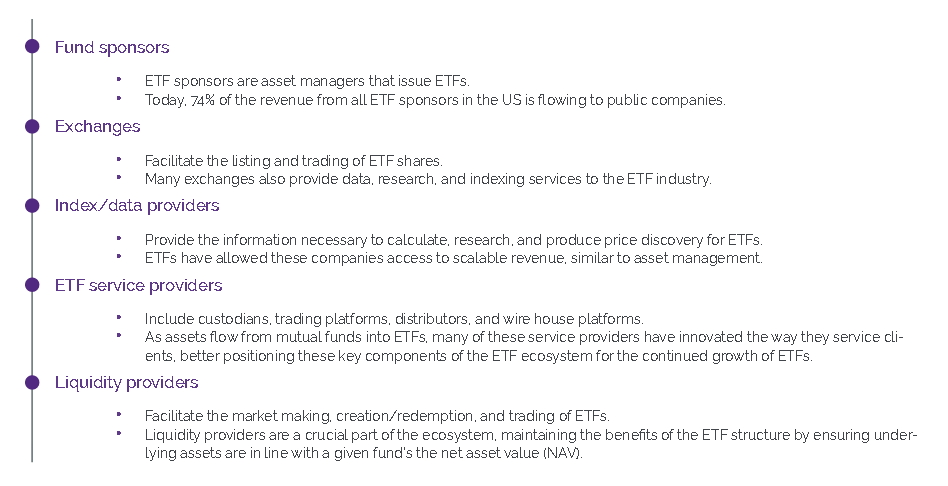

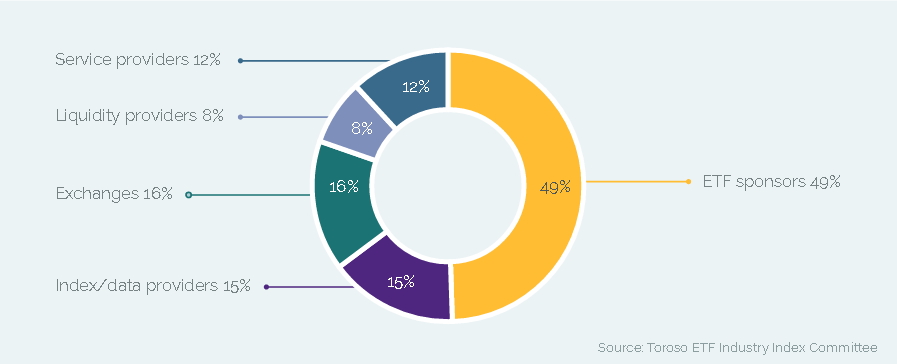

This targeted exposure to what I consider a serious growth venue is what sets TETF apart. Here is how the ETF breaks down its exposure on its website (tetfetf.com):

And here is a more visual look at how these different categories are represented in the portfolio:

.

What could go wrong with TETF as an investment?

It is currently difficult to find information on – but then it is only 1 week old.

It is thinly traded – but I believe greater exposure in coming weeks will change that very quickly. Until then, enter limit orders! If you enter market orders, especially in size, don’t be surprised if you are bringing sellers out of the woodwork who are only responding to your outsized offer.

TETF will only do exceptionally well as long as the market does well and as long as the trend away from open-end mutual funds to ETFs continues. As investors have discovered to their consternation in every bear cycle, no matter the investment, stocks, mutual funds, closed-end funds and ETFs all tend to decline.

There could easily be a major shakeout at some point of some of the sillier, narrower ETFs out there. It is natural for new funds (and companies, for that matter) to be formed and for others to die on the vine. If some of TETF’s bigger players get greedy and stupid and introduce more funds that don’t catch on, that mortality rate will increase.

Having said all that, the growth in ETF assets under management will increase at a very robust rate. Other nations and regions with well-developed exchanges and markets will soon discover the benefits of ETFs.

As a result, given the caveats above, I still see TETF as a way to own financials, but financials with a special twist -- not just financials but the growth that comes from companies that directly benefit from the expansion of the ETF marketplace. I began buying TETF this week for my family accounts and our managed portfolio clients.

Good investing,

Joe

Disclosure: I own TETF.

Start a free seven-day trial of Premium Membership to GuruFocus.