Amazon’s (AMZN, Financial) rise in the retail and technology sectors has been unstoppable, and its stock price has closely followed the "rise and rise" of the company for the last several years. Share price has more than quadrupled in the past five years, and the perennial question investors have in mind is: Have we missed the boat or is it still a good enough buy?

Amazon’s price-earnings (P/E) ratio is, of course, over the top. It’s not very often that you’ll find a company that is trading at a 186 times P/E ratio. But to use this metric to compare and contrast Amazon as an investment – versus other investment opportunities – will be serious mistake. Amazon’s CEO Jeff Bezos has made it clear many times in the past that he focuses on cash flow, not profit margins.

As a retail company, Amazon wants to achieve as much scale as it can, and as fast as it can. This requires Amazon to keep ploughing back almost everything it makes towards growth. A lot of the time, Amazon offers freebies, throws in a few more prime membership benefits and subsidizes customers’ shipping costs, while trying to cut down on delivery times and so on. This results in wafer-thin operating margins, and Amazon’s net income has been some of the most inconsistent you’ll ever see.

In fiscal 2014, Amazon had $88.988 billion in annual revenues, while their operating income was a mere $178 million as the company reported a net loss of $241 million for the year. As Amazon keeps hunting for top-line growth, using its earnings to value the company would be completely wrong.

The one metric that we can use is Amazon’s price-sales (P/S) ratio. Amazon is now trading at 3.31 times sales, much lower than the double-digit P/S at which its Chinese counterpart Alibaba (BABA, Financial) is trading.

However, if we compare Amazon’s P/S ratio with its retail rivals in the U.S., it is clear that Amazon does command a premium. Walmart (WMT, Financial) is trading at 0.49 times sales, Costco (COST, Financial) at 0.62 times sales and Target (TGT, Financial) at 0.44 times sales.

But Walmart, Costco and Target are growing at much slower rates than Amazon, which keeps hitting double-digit revenue growth rates on the retail front, both inside the U.S. as well as outside. As Amazon’s top line gets bigger and bigger, the growth rate will slow down, and the P/S ratio will gradually start moving down.

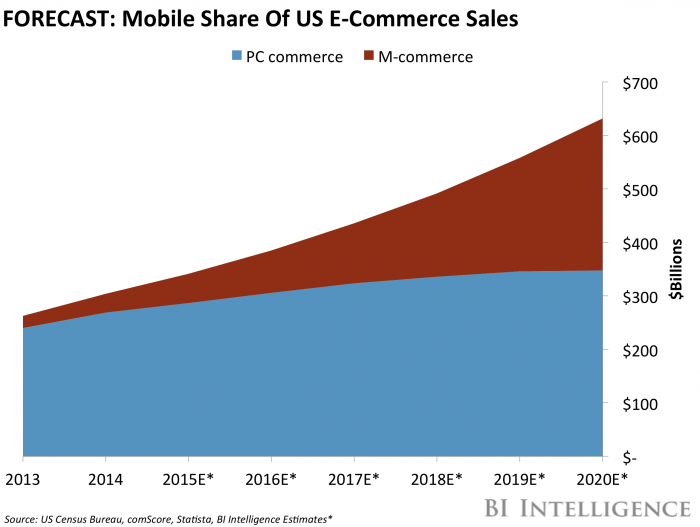

But the potential for Amazon’s top line to grow is huge. E-commerce sales account for less than 12% of retail sales in the U.S. With Amazon staying in control of the e-commerce segment, which is expected to keep its rapid growth intact for the next several years, Amazon’s U.S. revenues won’t explode from here, but they will keep growing at or above the e-commerce industry’s growth rate.

The NRF expects that online retail will grow 8% to 12%, up to three times higher than the growth rate of the wider industry. This suggests e-commerce sales are poised to fall between $427 billion and $443 billion, based on Census Bureau data.–Business Insider

With Amazon already expanding into more than 10 countries around the world, international sales will also keep increasing over the next decade. Add Amazon Web Services to the mix, and Amazon’s top line has three different pillars to keep its top line moving in the tens of billions of dollars over the next several years.

The P/S multiple will only start moving down as sales growth slows down, but that day seems to be several years away. Amazon is a good buy, and the best way to buy is to just keep buying for the next 10 years.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.