Walmart (WMT, Financial), the world’s largest retailer by revenues, is now back on the growth track. As competition intensifies in the retail sector, the strongest companies are slowly getting on top of the industry. The decades-old Walmart has already proven with steady but positive same-store sales last year that it can take on today’s competition and come out a winner.

Despite the uptick in revenues, though, the stock price hasn’t surged that much in the last year; it increased a little less than 7% in the last 12 months, making Walmart’s current dividend yield of 2.7% a mouth-watering proposition for investors.

Revenue growth

The most important question for any dividend investor is: Does the business have the capacity to expand its revenues? Because, if the company is able to increase its revenues, it will always help address any concerns in the balance sheet. But it works the other way, too: If there is no revenue growth, balance sheet strength will only provide short-term support before it starts hurting the dividends.

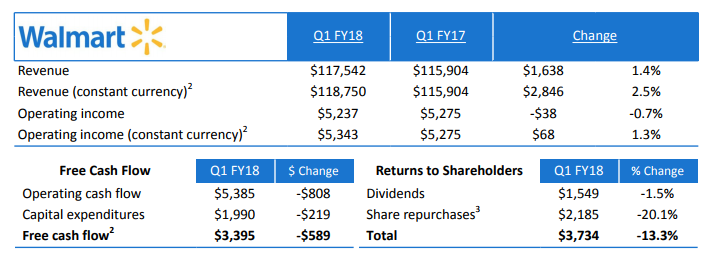

During the first quarter of 2018, Walmart’s total revenues grew by 1.4%, while revenues in constant currency grew by 2.5%. Revenue growth has been slowly increasing as Walmart put together a string of positive comparable-store sales during the past several quarters. As other brick-and-mortar stores like Target (TGT, Financial) and Kroger (KR, Financial) struggle to keep customers walking through the doors, Walmart has managed to do the opposite, despite its being the No. 1 player in the U.S. market.

“E-commerce growth at Walmart U.S. was strong, as sales and GMV increased 63% and 69%. The majority of this growth was organic through Walmart.com.” – First-Quarter 2018 press release

With e-commerce revenues accelerating, Walmart's ability to increase revenues has only become stronger by the day.

Current dividend payout and share buyback

During the first quarter of 2018, Walmart paid $1.549 billion in dividends, just 45% of its free cash flow of $3.395 billion, and 29% of its operating cash flow of $5.385 billion. One reason for the low payout ratio is that Walmart keeps buying back its shares. The company has brought down total shares outstanding from 4.072 billion in 2008 to 3.112 billion in 2017.

In the last two years, fiscal 2017 and fiscal 2016, Walmart paid $12.510 billion in dividends while spending $12.410 billion to buy back shares.

Cash position and balance sheet

At the end of first-quarter 2018, Walmart had $6.5 billion cash on hand while long-term debt stood at $33.774 billion. With quarterly operating income of $5.23 billion and interest expense of $563 million during the quarter, the balance sheet position is good enough for Walmart to keep the dividends steadily flowing for many more years, provided it keeps up its revenue expansion.

Conclusion

Considering its size, scale, strength and proven ability to compete and win in the highly competitive retail industry, Walmart’s 2.7% yield makes the retail giant an appealing investment opportunity for any dividend investor.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate positions in the next 72 hours.