Facebook Inc.'s (FB, Financial) high valuation multiples make the stock one of the most attractive shorts on the market. At the time of writing, Facebook had a short interest of 21.06 million. The stock price has surged by nearly 32% and is now trading around 15 times sales and 40 times earnings, which is certainly an attractive short. But the problem is the company keeps reporting record-breaking revenue growth, making things extremely difficult for short sellers.

Chief Financial Officer Dave Wehner warned investors during the third-quarter earnings call he expects the revenue growth rate to come down meaningfully in 2017 as “ad load,” or the number of ads Facebook can show to its users, is already near its peak. But three quarters have passed since the topic of “ad load” surfaced, and Facebook’s revenue grew 49% during the first quarter and 45% during the second quarter of the current fiscal.

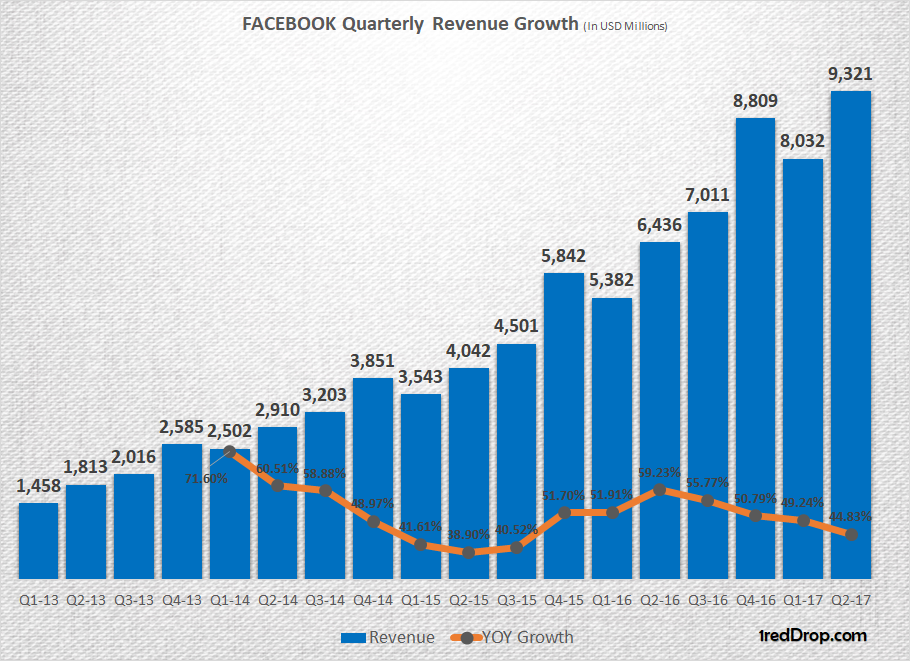

As shown in the chart above, the revenue growth rate has been slowly declining since the second quarter of 2016, when revenue grew 59.23%. Since then, revenue growth has been edging lower by a couple of percentage points; and that trend might continue throughout the rest of the year because Facebook has very little room to increase the number of advertisements it can show users.

But that does not mean Facebook’s revenue growth is going to sharply nosedive. User base growth has been as good as it ever was, crossing the 2 billion users mark during the second quarter with monthly active users expanding 17%, which was better than the 15% user base growth the company reported during second quarter of 2016.

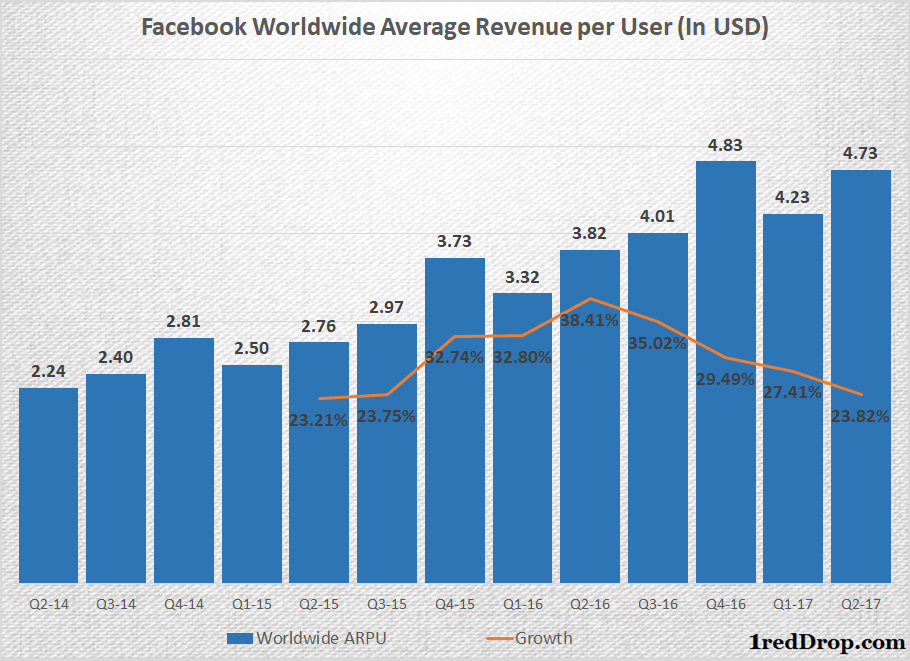

As illustrated in the chart above, average revenue per user, or ARPU, growth has been on a steady downward slope since the second quarter of 2016. This was a major factor behind Facebook’s revenue growth declining from near 60% to 45% over the last five quarters. It will be difficult for the ARPU growth rate to climb back up again as most of the user base growth Facebook is experiencing is coming from the Asia Pacific and Rest of the World regions, where advertising dollars made per user are much lower than it makes from developed economies such as the U.S., Canada and Europe.

But despite revenue growth edging lower, Facebook’s valuation multiples have moved up rather than down since the beginnning of the year. Additionally. it is not surprising to see short interest spike when that happens.

The problem with shorting Facebook, however, is there are several factors hiding in plain sight that can easily trip the shorts.

Instagram has been on a stunning growth path as the photo-sharing platform moved from 600 million to 700 million users in just four months. The networking effect could help propel Instagram’s user base growth further over the next several quarters, which will provide a huge support for Facebook’s advertising revenue. The other factor to remember is WhatsApp, the messenger platform Facebook has yet to monetize, and several more that front could push the stock price higher. Facebook recently announced it is testing a WhatsApp Business app as well as an enterprise solution, so that could happen sooner rather than later.

Right now, the risks far outweigh the returns for Facebook shorts. As a result, it is probably a good idea to just keep away from Facebook instead of going against the tide.

Disclosure: I have no positions in the stock mentioned above, and no intention to initiate a position in the next 72 hours.