Anheuser-Busch (BUD, Financial) sells beer and a lot of it. With iconic brands such as Bud Light, Corona, Budweiser and Stella Artois under its banner, the world’s largest brewer is so well diversified in its portfolio that a lot of people don’t even realize they are drinking products from the same company. We have been drinking beer for many centuries, and people will drink it for many more centuries after we are gone. If you are looking for longevity in a business, Anheuser-Busch is as good as it gets.

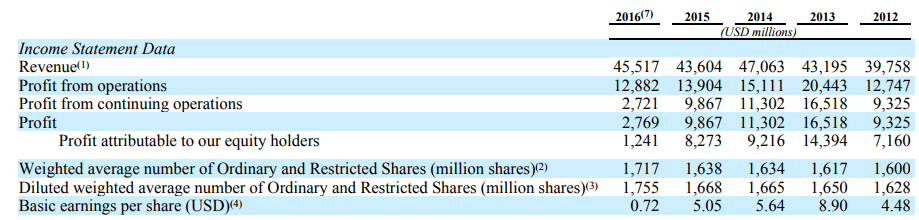

Anheuser-Busch’s revenue increased in the last five years thanks to the company’s acquisition of SABMiller for $107 billion in 2016; the combined company accounts for nearly one-third of the global beer market. The good news for investors is the size of Anheuser-Busch makes it a cash flow generator for many decades to come; but the bad news as the largest company in the world is that growth will ebb and flow along with the industry average.

The entire world drinks beer, and volumes are not going to skyrocket in the future. In the best of times it could provide a few percentage points of growth, and in the worst of times it will decline by the same amount. If you are an investor who is looking for sharp capital appreciation, please look elsewhere. This is a company that will easily outlive us, but revenue growth will always be sideways from here on out.

In a mature market, acquisition is one way for companies to grow, and that’s something Anheuser-Busch has done really well in the past. But with nearly one-third of the market under its control, there isn’t much room for buying more companies so expect acquisitions to be slow and steady in the future.

All these characteristics make Anheuser-Busch an ideal company for dividend investors. The company paid $8.45 billion in dividends in 2016, which is 65% of its operating income of $12.88 billion. Total shares outstanding increased from 1.6 billion to 1.717 billion in the last five years thanks to Anheuser’s acquisitions during the period. With the odds of more large-ticket acquisitions becoming slimmer, Anheuser will slowly start buying back its own shares and reducing the dividend it pays.

At the end of the second quarter of the current fiscal, Anheuser had $113.941 billion in long-term debt, nearly 10 times the size of its 2016 operating income, which does add a lot of pressure to its balance sheet. The high level of debt is why I am confident that Anheuser will not be thinking about any big-ticket acquisitions over the medium term as there isn’t enough room in the balance sheet. It will focus on ploughing back its cash flow toward dividends and share buybacks and reducing its leverage.

Debt load and slow growth are the risk factors that have pushed the dividend yield to go above 3.5%. But the quality of the business alone compensates for that risk, making Anheuser an extremely attractive investment for any long-term dividend investor.

Disclosure: I have no position in the stock mentioned above and no intention to initiate a position in the next 72 hours.

Also check out: (Free Trial)