Peter Feld of Starboard Value LP owns 10.7% of Mellanox Technologies Ltd. (MLNX, Financial) and just sent a warning shot to the board of directors and management. We’ll dive into the specifics the letter addresses in a minute but the central message I derive is: Heed our advice or we are coming after your jobs.

Mellanox is a tech company that is involved in a lot of exciting industries and is somewhat of a counterintuitive target for Starboard.

Starboard is a great activist shop with a tremendous track record. Lately they have been moving to cash and returning cash to investors. At the same time they are going after lots of special situations and companies that don’t really trade in sync with the market. The quote below is from the Starboard letter and is followed by my commentary:

"While we appreciate the need and desire for company officers to sell some stock over time, the frequency and magnitude of insider selling at Mellanox is staggering and among the most one-sided we have ever seen. It raises serious questions as to both the level of commitment that the Board has to the Company and the level of confidence the Board has in management’s operating plan.

"In fact, no director or member of senior management has purchased a single share of stock in the open market since 2013."

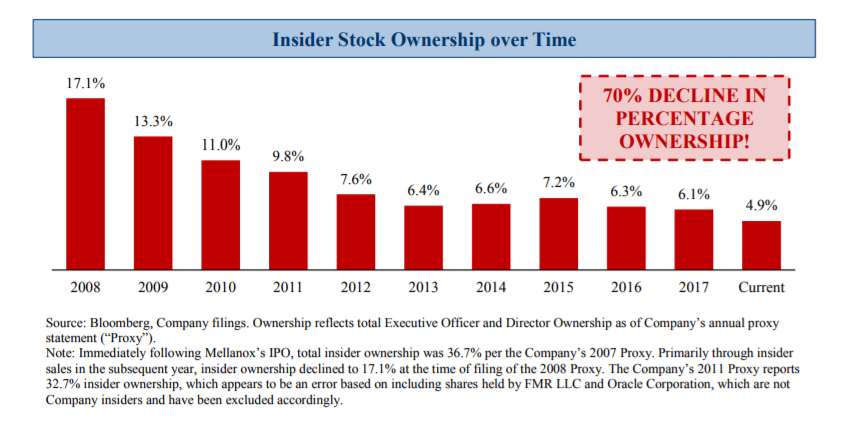

The firm goes on to quantify the insider selling in excruciating detail. The letter actually contains an extensive list with every sale attached. Insiders probably didn’t need to be reminded but with the letter leaking this could potentially open some eyes at other large shareholders like Fidelity or Neuberger Bermann.

Starboard is especially angry because Mellanox insiders have been selling while maintaining that the outlook for the company is extremely bright. A clear case of talking the talk but not walking the walk (emphasis mine):

"What strikes us as most concerning is that Mellanox’s pattern of insider selling has continued, and even intensified, following management’s release of full year guidance in December 2017.

"It is certainly confusing when management states, on the one hand, that they do not have visibility into current quarter revenue trends, while, on the other hand, stating that they have a high degree of confidence in double-digit revenue growth in both 2018 and 2019. When these statements are immediately followed by a continuation of substantial insider selling, the logical conclusion is that the Company actually has very little confidence in short-, medium-, and long-term trends."

It gets really painful when Starboard starts talking about not just the insider selling but also the height of their compensation and management's performance:

"Further, as we have discussed, shareholders have long had concerns with the level of stock-based compensation at the Company, especially given Mellanox’s long-term underperformance in terms of both operating results and stock price. High stock-based compensation is not always a problem. There are benefits for tying compensation to performance and aligning insiders’ interests with those of all shareholders. For high-performing, well-governed companies, high stock-based compensation is often the result of, and reward for, excellent performance and the achievement of long-term target metrics. Unfortunately this has not been the case at Mellanox."

Ouch.

Starboard also included a damaging graph illustrating Mellanox's underperformance in total shareholder returns and its insider compensation. The company isn’t on the right quadrant of the graph to say the least:

Notwithstanding Mellanox's flaws, Starboard is very interested in this investment:

"We believe that Mellanox is a fantastic investment today, with substantial opportunities to meaningfully outperform its peers going forward, and we are excited to be the Company’s largest shareholder."

Likely Starboard would love to pull the standard activist playbook and do something about the operating margin trend, which is moving in the opposite direction you would expect at a growth company:

If you look at the long-term financials here on GuruFocus, you'll see revenue is growing at a very respectable rate. Strangely, none of the profit metrics is keeping pace.

At $61 per share, Mellanox is quite expensive, especially in light of EBITDA of less than $2 and revenues of about $17 per share. However, revenue growth of about 13% per year for the past five years is fairly attractive. If that sort of growth rate is sustainable and Starboard is able to expand margins again, resulting in additional free cash flow going forward, the company is indeed a very attractive investment. It should do very well over the next few years if Starboard gets its way.

Disclosure: No position.