James Montier of GMO put out another bearish notes. These are must reads, especially if you are bullish or positioned bullish. I noticed my last article on a GMO note which talked about the possibility of a 50% melt-up was much more popular compared to the bearish commentary I share. We all want the market to go up and keep riding the easy money waves. That’s why it is so important to seek out that other sound. The grumbling of the bear. You can read the full note here, but I’ve quoted some of Montier’s gems below accompanied by my perspective:

Montier leads of by showing the elevated multiples awarded to the S&P 500. Most of you will be aware of the high valuations we are observing. The only reasonable defense I heard is that posited by Buffett; stocks are about fairly valued at these interest rates. The problem is I don’t believe interest rates are on a random walk from their current level. Once the Fed reverses directions and starts raising rates it continues on that path. Usually, getting interest rates to much higher levels compared to the current. The one reason I can see the Fed deviate from that path is if we are hit with a surprise recession (there are no signs of one). However, if a recession hits, the market will be in trouble as well. The way I look at it, there isn’t really a path the Fed can take that tends to bolster equities or bonds for that matter.

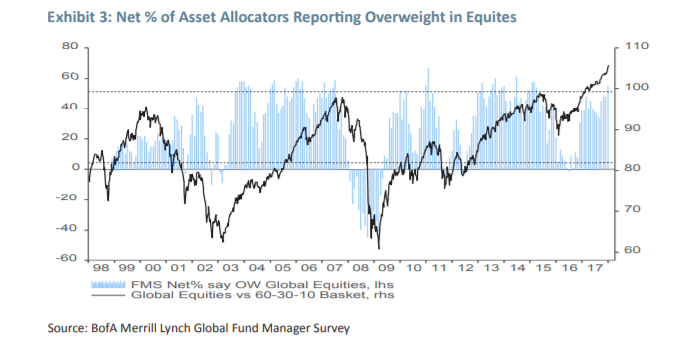

Montier proceeds to show a couple of very interesting graphs about professional fund managers outlook and positioning:

The pair of graphs show that most professionals believe the market is overvalued. Logically, they are massive long equities and sarcasm.

Montier than seeks the explanation for the discrepancy by assigning a type to the kind of (bubble) market we are experiencing; the rational bubble.

"The third type of bubble is known in the academic literature as a near rational bubble. I am not a great fan of this nomenclature as it suggests a veneer of respectability that I find undeserved. To me these are really better described as greater fool markets. They are cynical bubbles in that those buying the asset in question don’t really believe they are buying at fair price (or intrinsic value), but rather are buying because they want to sell to someone else at an even higher price before the bubble bursts.

Chuck Prince, the former CEO of Citibank, aptly demonstrated the typical cynical bubble mentality when in July of 2007 he uttered those fateful words,

'As long as the music is playing, you’ve got to get up and dance. We are still dancing.'

I would suggest that this is exactly the sort of market we are observing at the current juncture. Fund managers for the most part all agree that the US market is expensive but still they choose to own equities – a cynical career-risk-driven position if ever there was one. I have been amazed by the number of meetings I’ve had recently where investors have said they simply “have to own US equities.”

It is accompanied with another graph showing a majority of managers believe the market will peak this year:

This is why I’m reading these notes by superstar investors. I didn’t realize many professionals are experiencing career risk by not being invested. Although it’s not a super trustworthy data point, it is very interesting.

ETFs and indexes are all the rage. Indexes are not thinking at all and just propping up stocks as they continue to gather inflows. Professionals are forced into equities if they want to hold a job. And it’s a cushy job. That leaves the amateur investors to do the price investigation and maintain discipline. I’m not surprised we arrived at high valuations.

The answer Montier doesn’t have is when the market will break. Neither do I. However, pivoting away from the U.S. and selling stocks you (deep down) know are overvalued, makes a lot of sense to me.

In addition it could pay to seek out more defensive and/or idiosyncratic exposures. Montier ends his note with a great Keynes quote and it is so good I’ll include it here:

"It is the nature of organized investment markets, under the influence of purchasers largely ignorant of what they are buying and speculators who are more concerned with forecasting the next shift of market sentiment than with a reasonable estimate of future yield of capital - assets, that, when disillusion falls upon an over-optimistic and over-bought market, it should fall with sudden and catastrophic force."

Disclosures: No positions in any stocks mentioned.