Ray Dalio (Trades, Portfolio) founded Bridgewater Associates in 1975. GuruFocus has the firm pegged at around 13% annual returns after fees. Bridgewater gathered over $100 billion in assets, so it’s definitely doing something right. Lately Dalio has appeared in the media a lot as he wants to reach out and promote his somewhat unusual principles around the world. He collected his life principles in the first of two books, called "Principles."

Most recently he appeared on Bloomberg TV and talked about the outlook for China and Europe. I have the impression Dalio tends to be very diplomatic when talking about China and quick to talk about the bright side of things. It seems that he tends to be more forthright talking to or about regulators and governments of the U.S. This is my take from observing quite a few Dalio interviews and appearances, but I could be wrong or biased myself. Perhaps he truly believes the long-term outlook for China outweighs the gravity of any short-term problems.

I can think of two reasons for Dalio’s diplomacy:

He is apparently involved with policymakers and likely would like to build Bridgewater’s business in Asia. He may not want to offend Chinese policymakers who could have a lot of power to make life for Bridgewater difficult.

The quick Cliff's notes:

- China has a vital economy with short-term problems.

- Europe has a bright short-term future but needs to deal with inequality, which can ignite populism.

- Inflation could be a concern in two years.

China

Dalio appears truly excited about China. He thinks the opening of its capital markets is terrific. China is the second largest market in the world. Dalio has been involved in the evolution of the Chinese capital markets, and he sees huge progress. Not everything is perfect, but the important thing is the direction the country is moving.

People put too much emphasis on short-term problems. There have always been reasons not to believe in China’s success. The main current criticism of China is that it is overleveraged. Jim Chanos (Trades, Portfolio) and Kyle Bass (Trades, Portfolio) have eloquently argued that point on quite a few occasions. According to Dalio the regulators acknowledge the problem and are more forthright about it as compared to U.S. regulators in the 2008 crisis.Â

He adds that financial crises come and go but you have to look at the capabilities and entrepreneurship. In this respect China is a terrific place. I’ve included Bridgewater’s holdings below. The fund has a large allocation to the iShares Emerging Markets ETF (EEM, Financial), meaning the fund is putting its money where its mouth is.

He briefly talks about the attractiveness of China to asset management and says the Chinese government will determine how welcome outside investors are. This is in line with Chinese behavior towards other industries. Dalio sees opportunity as the Chinese want to bring in the best global standards because they want to build great industries. This suggests best practice funds are well-positioned.

This matches my knowledge of the forays into China of Bridgewater and Blackstone (BX, Financial), the largest private equity and alternative investment shop in the world. These firms are building connections and seem to be tolerated. The track record for U.S. companies' success in China is mixed. Alphabet (GOOG, Financial)(GOOGL, Financial) and Apple (AAPL) experienced problems. It seems Chinese authorities are not very fond of businesses coming in to dominate their markets but if they work together with local firms (DreamWorks), or bring something else besides business, the country seems more welcoming.

Europe

Usually Europe gets described as a big mess, and there’s certainly truth to that. Dalio again takes a more upbeat perspective. He says, "There is today and what used to be."

Which I take to mean that it is at least improving. Draghi and ECB should be congratulated. Although there is always debate about the best policies, we have made it through the worst debt crisis and experienced beautiful debt deleveraging. Growth is improving.

He acknowledges there could be more structural reforms but emphasizes that there have been structural reforms as well. As a European, I am somewhat knowledgeable about the subject and while reforms fall far short of perfection, it is definitely true that there have been improvements. Improvements continue to be made. Under Macron, even France is making some tough structural changes.

Dalio believes inflation not getting up to 2% is not a big problem. What he views as the major problem is inequality. Europe (or the world) can’t have a big slideback because that will fire up inequality debate and fuel populism. That’s the real danger.

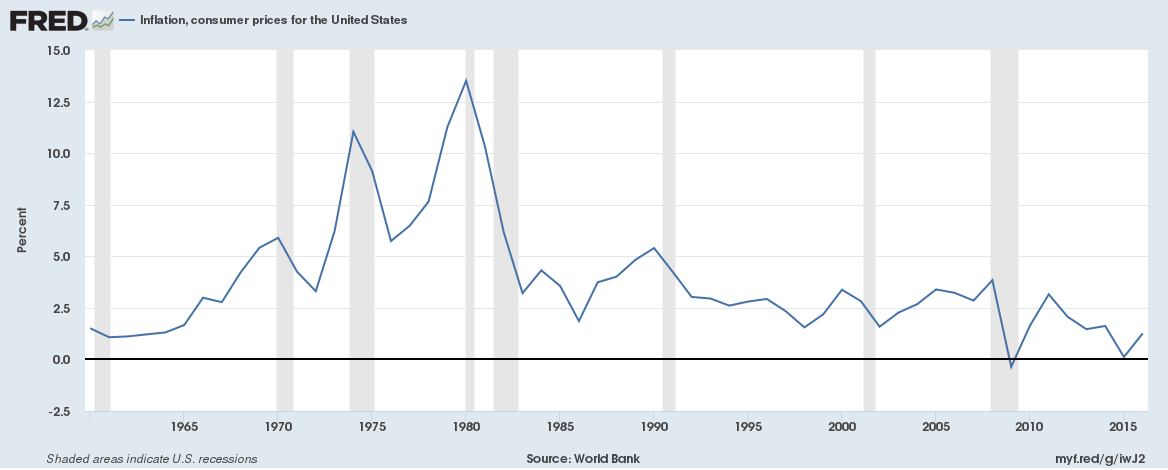

Inflation U.S.

Should we be concerned about inflation? Dalio thinks it is a funny topic. Should he be concerned it is too high or too low? Is too-low inflation a problem? It used to be. Dalio thinks we are in a pretty good spot.

As I see it, the problem isn’t low single digit inflation. My fear is that a lot of drivers are lining up to drive inflation higher, and when we’ve seen severe spikes in the past it turned out to be extremely hard to control inflation.

Dalio acknowledgef this to an extent as he is concerned that near the end of the cycle the central bank will have a challenge to get it right -- especially if there has also been a lot of fiscal stimulus put on.

He sees the U.S. as being in the later part of the cycle. The goldilocks period. Not too hot and not too cold. Growth but no inflation. If we move further where the brakes get put on by higher interest rates and the balance sheet will go off that could end the cycle.

In Europe the interest rate will lag, but quantitative easing has been started.

Dalio doesn’t think rates will get hiked much faster, as implied by the curves.

Bridgewater’s portfolio: