Markets are perceiving the recent testimony from newly-seated Federal Reserve Chairman Jerome Powell as more dovish in tone when compared to the comments made earlier in his tenure. But markets remain convinced that four rate hikes in 2018 are still a distinct possibility going forward. On balance, this more “dovish” tone from the Fed has only had a bearish impact on market sentiment and would add to the stock volatility levels we have seen in the last few months.

Essentially, Powell’s tone at the Fed’s most recent monetary policy meeting was softer with respect to potential inflation risks. Powell essentially explained that he sees no evidence the economy is growing at an excessive rate, adding that “Nothing suggests wage inflation is at the point of acceleration.”

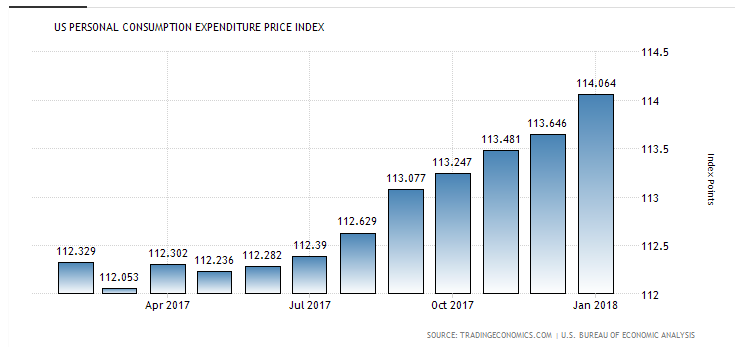

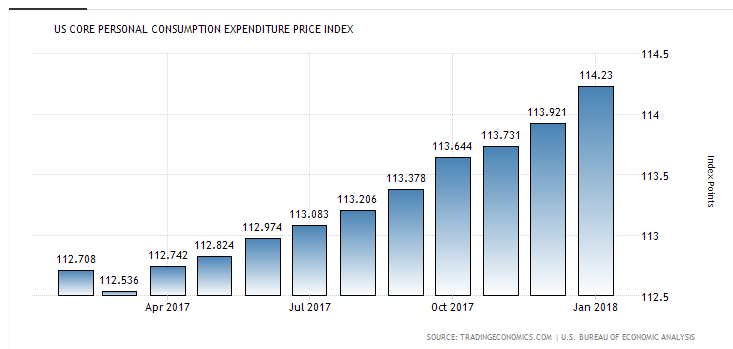

On the data front, the personal consumption expenditures reading is a highlight. The report is typically referred to as the Fed’s “preferred” inflation gauge and, since it seems that we are currently at a critical juncture in terms of defining the most likely interest rate path for the U.S. in 2018, the release probably got more attention than it actually deserves.

The core personal consumption expenditures is a reading that removes food and energy from the index, and the most recent number from January rose 0.3%. This is significant because it equals the largest increase since the post-2008 economic recovery first started. To find a time when the core readings in the index rose faster, we would need to go back to the bull market of 2007. That said, the yearly rise in the core index remains flat (up 1.5%) in a trend that now goes back four months.

Ultimately, inflation has shown gradual increases over the last several years, but we are still not within the Fed’s 2% banded target. This is largely why I am viewing the Fed’s recent comments as little more than rhetoric that is unlikely to be matched by four actual rate hikes this calendar year.

In some of today’s news outlets, President Trump's tweet regarding Amazon (AMZN, Financial) actually overshadowed Powell’s testimony entirely. This may not be surprising, given the fact Powell was asked the same question over and over again (U.S. debt insolvency).

Powell was more direct and short term in nature in his responses. I don’t think any of the politicians featured on today’s TV news breaks actually got the soundbites they wanted. Powell was there to steer the ship in the other direction (away from yesterday’s hawkishness). When we look at the market reaction in both stocks and treasuries, I would say Powell met his goal (and wagged the dog in the process). In other words, market volatility did stabilize without any additional changes in policy actually taking place.

Interest rates

We should see U.S. interest rates at 2.75%, so a flat yield curve before the end of the year is a very real expectation.

Powell is not interested in stock markets moving much higher and is looking to limit shocks like those already seen in the Dow earlier this year. This is an emphasis on rhetoric to rein in expectations and keep the market stable after the recent periods of surprise volatility.

Disclosure: Author has no positions in any assets mentioned.