Business overview

Cara Therapeutics Inc. (CARA, Financial) started its operations in 2004 and is a clinical-stage biotech company focused on the development of novel therapies. They are targeting the body’s peripheral kappa opioid receptors that are beneficial for pruritus indication. The current president and CEO, Derek Chalmers, Ph.D., is its co-founder and has been running the company since 2004. He also co-founded Arena Pharmaceuticals in 1997, which reflects his excellent expertise and professional experience over 20 years in the biotech industry. Arena Pharmaceuticals has a market cap of $2 billion today, and I firmly believe Chalmer can also turn Cara into a multi-billion dollar business.

Source: Investor Presentation, November 2018

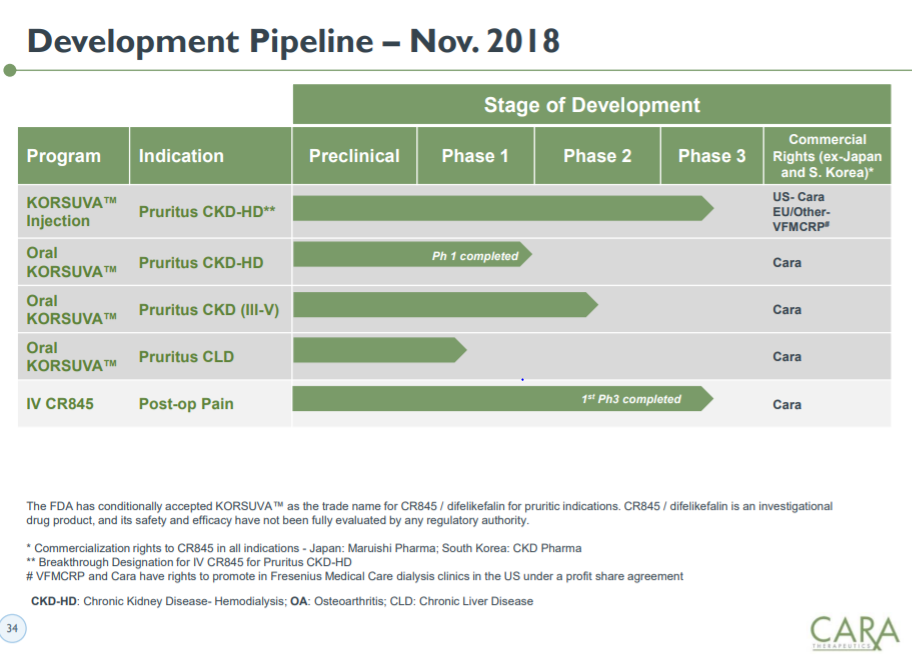

Cara has exclusive worldwide rights for to a pipeline of six therapeutics programs, with the key clinical program CR845 or under the brand name Korsuva. Cara recently successfully completed phase II for the treatment of patients with pruritus, while showing statistically significant reductions in itching, improvement in the quality of life measures and without strong adverse side effects. The company also expects its novel mechanism of action using kappa receptors to serve as an important treatment for pruritus across a various range of indications, including dermatological conditions. This clinical trial is also a backbone of my investment thesis, as Cara is well positioned to successfully go through all FDA phases and generate more than $1 billion peak revenue by 2027.

Source: Investor Presentation, November 2018

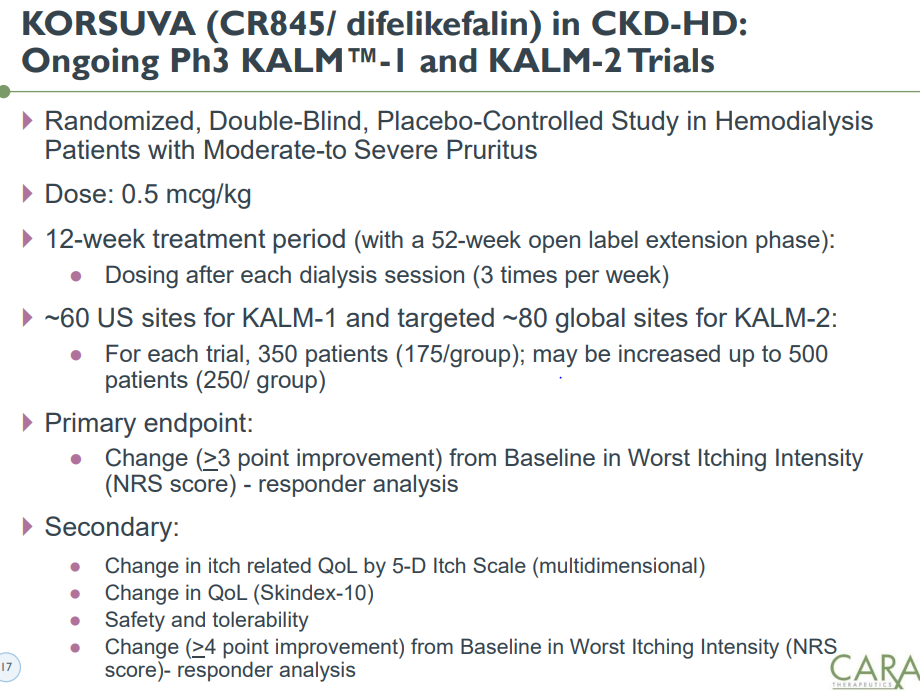

Cara has the ongoing U.S. and global phase 3 trial of Korsuva (KALM-1 and KALM-2 studies) injection for the treatment of CKD-aP in patients with hemodialysis indication. It has received a breakthrough designation in 2017 and is still enrolling patients in 60 U.S. sites, which it expects to complete by the first half of 2019. The company plans to enroll up to 250 patients in a particular study and if the FDA orders an expansion to 500 patients, that might lead to increased study-related costs.

As reflected in the table above, both studies have the primary efficacy endpoint of achieving at least a three-point improvement from baseline at week 12, with daily worst itching intensity score measured on a standard numeric scale or NRS. In a previous phase II study, higher dosing than 0.5 mg didn’t lead to more statistically significant improvement from placebo. However, it might become an issue if Cara has to use higher dosing like 1.0 mg or more for treatment. It would most likely lead to reduced effectiveness and increased adverse side effects.

There is also an ongoing open-label, long-term safety extension 52-week study, that evaluates Korsuva Injection and already has 175 patients enrolled. There are around 275,000 patients with pruritus in the U.S., with the total addressable market of more than $40 billion in 2018. A particular indication has no FDA-approved medications or standard of care. That provides a great opportunity for Cara to become the first company to meet a large medical need with potential peak revenues of $1 billion by 2025.

Source: Press Release, August 2018

There are other phase I and phase II oral Korsuva studies ongoing for moderate-to-severe pruritus. Positive clinical data results from both studies in early 2019 would lead to a significant stock price rise.

Phase study II is a 12-week trial testing the safety and efficacy of oral Korsuva with three dose levels of 0.25 mg, 0.5 mg and 1.0 mg given once daily compared to placebo. According to the figure above, oral Korsuva tablet has a similar efficacy and safety profile at 0.5 mg per kg as injection Korsuva. Therefore, if injection Korsuva gets FDA approved, it is likely oral Korsuva in pruritus-related indications will as well. Oral Korsuva has a larger population of 2.5 million with no FDA-approved therapies and is targeting CKD stage 3 to five patients with pruritus. There is no serious competition in the pruritus market and once the intellectual property expires in 2026 generics will enter the market.

Financials

Source: Investor Presentation, November 2018

The company reported results for the third quarter at the beginning of November 2018. It recognized $5 million of a license-fee revenue because of the recent collaboration agreement with Vifor Fresenius Medical Care Renal Pharma or VFMCRP. Both companies signed the deal to commercialize Korsuva injection to dialysis patients worldwide except in the U.S., Japan and South Korea. Cara received an up front payment of $50 million in cash and equity investment of $20 million at a price of $17.00 per share. It can also earn additional regulatory and commercial milestones payments of up to $470 million. This deal is highly important as Cara received important funding to continue with its U.S.-related clinical trials and can also use its extensive Frensius network, strong dialysis centers and its deep domain knowledge.

Reported R&D was at $22.3 million, up 142% year-over-year, and general and administrative expenses were $3.2 million, up 7% year-over-year. As the company advances its clinical trials, there will be increased R&D and G&A expenses, because of manufacturing expenses related to drug candidates, pre-clinical study efforts and use of third-party consultants and increased staff-related costs. It also reported a net loss of $19.4 million or 51 cents per share.

The company reported cash and cash equivalents of $206.1 million as of Sept.r 30, 2018, and it believes that its cash position will be enough to fund its operations and capex requirements into 2021. It has also completed a successful additional common share offering of $19.00 per share, which contributed to net proceeds of approximately $92.1 million. For the U.S phase III study for injection Korsuva, the company might need to raise additional cash if it conducts it on a standalone basis, or in the worst case scenario it might find a partner who will take over funding of the study.

Valuation

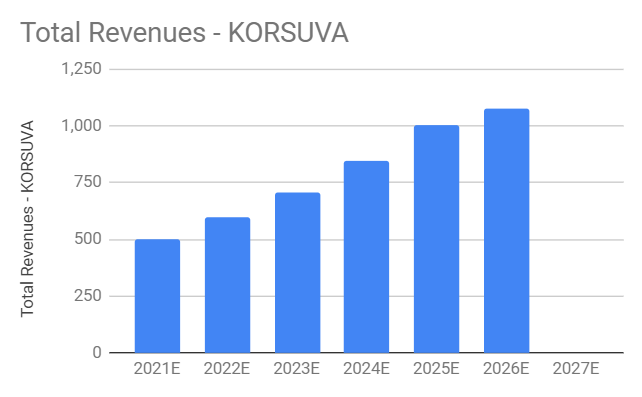

I have computed my own estimates for injection Korsuva. I expect the market launch of injection Korsuva in 2021 starting at global total revenues of $500 million. In my view, injection Korsuva has a global peak revenue potential between $1 billion and $1.1 billion. I expect injection Korsuva revenue to rise with CAGR of 19% between 2021 and 2025. The company has Korsuva IP protection until 2026 and for minor Korsuva patents even until 2027. Thus, I have assumed a conservative CAGR of 7% for injection Korsuva between 2025 and 2026, which derives a peak total revenue of $1.08 billion in 2026 as reflected on the chart below.

Source: Author’s own computation

Using the standard biotech discount rate of 15% for NPV calculation and 30% POS for successful market launch, I derive a current NPV value for injection Korsuva of $550 million. In 2018, many relevant biotech deals were done around EV-rev multiple of 3x. If I apply an EV-rev multiple of 3x to my estimated NPV revenue for injection Korsuva of $550 million, the company has enterprise value of $1.65 billion and without subtraction of net cash, it has a market cap of $1.86 billion. That makes a conservative upside potential of 265% compared to the current market cap of $509.8 million. Any positive progress in other clinical trials in Cara’s pipeline or a newly launched clinical trials in other lucrative dermatological indications such as atopic dermatitis or psoriasis makes upside potential even higher than projected 265%.

Risks

Key risks to a long thesis are a potential next phase clinical trial failure for oral and injection Korsuva and a lower-than-expected commercialization and market penetration in the case of the product launch on market. In terms of commercialization, Korsuva will compete against opioid products and might become subject to restrictive marketing and distribution regulations. Korsuva also acts as a kappa opioid receptor agonists, and this drug class has never yielded a successful commercial product for pain indications in the past. Thus Korsuva contains a huge risk that it will be successful for the first time. Even though the FDA granted Korsuva a breakthrough designation, that doesn’t mean the product will go faster through the regulatory review and approval process.

Read more here:

Contest: Sale Season on Plastivaloire

GuruFocus Value Idea Contest: December Update

Contest: The Sky Is the Limit With the Skyworks Growth Story