Seahawk Drilling, Inc. (HAWK, Financial), which I’ve posted about before, has taken a pounding over the last few days, down over 11% just yesterday to close at $9.61. It seems crazy to me. HAWK is cheap as a going concern, but with its market capitalization at $113M, it’s now at a hefty discount to its liquidation value. Here’s how I figure it:

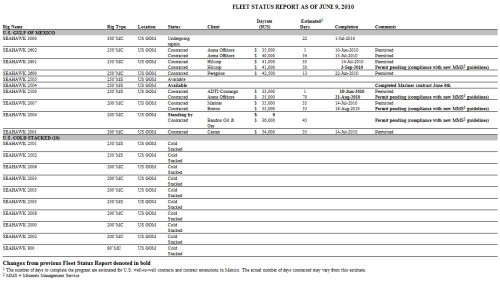

Here’s a list of HAWK’s rigs and their operating status from the June 9 Drilling Fleet Status Report:

There are two possible liquidation values for HAWK rigs. In the slightly more optimistic scenario, HAWK’s rigs are sold off as operating rigs to other drillers in the Gulf of Mexico. In the other more dour scenario, some of HAWK’s rigs are sold for scrap. HAWK is trading at a discount to both values.

Rig resale values

In March and April this year, ENSCO Plc (NYSE:ESV) sold three 300”² ILC rigs from the same vintage as HAWK’s rigs for ~$48M a piece (see press releases hereand here). These are clearly higher specification and therefore more valuable than HAWK’s rigs, but the sales do provide some insight into recent market conditions. Here’s a chart from HAWK’s presentation (.pdf) to the Macquarie Securities Small and Mid-Cap Conference on June 15 and 16 showing comparable sales since 2004:

When 300”² ILCs have sold in the past for ~$48M, rigs comparable to HAWK’s have sold for around $15M each. HAWK is presently trading as if its rigs are worth only $6M each. Retired rigs have sold recently for between $5M and more. Hercules Offshore, Inc.’s (NASDAQ:HERO) 31 December, 2009 10K is illustrative:

Scrap value

In this audio of the presentation to the Macquarie Securities Small and Mid-Cap Conference, Randy Stilley, the President and CEO of HAWK, says in relation to the slide below, that the value of the scrap steel and equipment on HAWK’s rigs is worth roughly $8M to $9M each:

Randy Stilley (at about 21 minutes into the presentation):

If the ten cold stacked rigs are worth $80M in scrap, and the ten other operating rigs are worth $150M ($15M each), HAWK has $230M in rig value. Add HAWK’s $88M in cash and receivables, and deduct HAWK’s $164M in total liabilities, and HAWK is worth $154M in the most dour liquidation scenario. With a market capitalization of $113m, HAWK is trading at a hefty discount to this value, and HAWK is too cheap. It’s burning cash, it’s got a chunky payable to Pride and some Mexican tax issues, but subliquidation value never materializes without hair.

Hat tip BB.

[Full Disclosure: I hold HAWK. This is neither a recommendation to buy or sell any securities. All information provided believed to be reliable and presented for information purposes only. Do your own research before investing in any security.]

Greenbackd

http://www.greenbackd.com

Here’s a list of HAWK’s rigs and their operating status from the June 9 Drilling Fleet Status Report:

There are two possible liquidation values for HAWK rigs. In the slightly more optimistic scenario, HAWK’s rigs are sold off as operating rigs to other drillers in the Gulf of Mexico. In the other more dour scenario, some of HAWK’s rigs are sold for scrap. HAWK is trading at a discount to both values.

Rig resale values

In March and April this year, ENSCO Plc (NYSE:ESV) sold three 300”² ILC rigs from the same vintage as HAWK’s rigs for ~$48M a piece (see press releases hereand here). These are clearly higher specification and therefore more valuable than HAWK’s rigs, but the sales do provide some insight into recent market conditions. Here’s a chart from HAWK’s presentation (.pdf) to the Macquarie Securities Small and Mid-Cap Conference on June 15 and 16 showing comparable sales since 2004:

When 300”² ILCs have sold in the past for ~$48M, rigs comparable to HAWK’s have sold for around $15M each. HAWK is presently trading as if its rigs are worth only $6M each. Retired rigs have sold recently for between $5M and more. Hercules Offshore, Inc.’s (NASDAQ:HERO) 31 December, 2009 10K is illustrative:

Additionally, the Company recently entered into an agreement to sell our retired jackups Hercules 191 and Hercules 255 for $5.0 million each.The rigs have a resale value well beyond the price implied by the company’s stock. Not convinced they can all be sold as operating rigs? How about as scrap?

…

In June 2009, the Company entered into an agreement to sell its Hercules 100 and Hercules 110 jackup drilling rigs for a total purchase price of $12.0 million. The Hercules 100 was classified as “retired” and was stacked in Sabine Pass, Texas, and the Hercules 110 was cold-stacked in Trinidad. The closing of the sale of the Hercules 100 and Hercules 110 occurred in August 2009 and the net proceeds of $11.8 million from the sale were used to repay a portion of the Company’s term loan facility. The Company realized approximately $26.9 million ($13.1 million, net of tax) of impairment charges related to the write-down of the Hercules 110 to fair value less costs to sell during the second quarter of 2009 (See Note 12). The financial information for the Hercules 100 has historically been reported as part of the Domestic Offshore Segment and the Hercules 110 financial information has been reported as part of the International Offshore Segment. In addition, the assets associated with the Hercules 100 and Hercules 110 are included in Assets Held for Sale on the Consolidated Balance Sheet at December 31, 2008.

During the second quarter of 2008, the Company sold Hercules 256 for gross proceeds of $8.5 million, which approximated the carrying value of this asset.

Scrap value

In this audio of the presentation to the Macquarie Securities Small and Mid-Cap Conference, Randy Stilley, the President and CEO of HAWK, says in relation to the slide below, that the value of the scrap steel and equipment on HAWK’s rigs is worth roughly $8M to $9M each:

Randy Stilley (at about 21 minutes into the presentation):

This is something that is just kind of amazing in a way. If you look at the underlying asset value of our rigs: five million dollars. The scrap value of a jackup is about eight or nine [million dollars], and that’s assuming that you get almost nothing for the steel and you just start taking stuff off of there; mud pumps, engines, top drives, cranes, draw works. If you start adding all that up, that alone is worth more than our current asset values based on our equity.Conclusion

Now you can also say, “Well, if they’re not working, they’re not worth much,” and we’re not likely to just start cutting them up for scrap, but I think that’s kind of an interesting reference point that you don’t want to forget about because we’re trading at a very low value today.

If the ten cold stacked rigs are worth $80M in scrap, and the ten other operating rigs are worth $150M ($15M each), HAWK has $230M in rig value. Add HAWK’s $88M in cash and receivables, and deduct HAWK’s $164M in total liabilities, and HAWK is worth $154M in the most dour liquidation scenario. With a market capitalization of $113m, HAWK is trading at a hefty discount to this value, and HAWK is too cheap. It’s burning cash, it’s got a chunky payable to Pride and some Mexican tax issues, but subliquidation value never materializes without hair.

Hat tip BB.

[Full Disclosure: I hold HAWK. This is neither a recommendation to buy or sell any securities. All information provided believed to be reliable and presented for information purposes only. Do your own research before investing in any security.]

Greenbackd

http://www.greenbackd.com