What Is a Value Trap?

A value trap is a stock that looks like a good buy because it’s inexpensive, but turns out to be a bad investment due to underlying business reasons.1

At first, value traps can seem attractive because they trade at low valuation multiples (i.e. low P/E ratio, low P/B ratio, etc.). To an inexperienced investor, these metrics make a stock look like a bargain. The problem is that sometimes the stock is cheap for a good reason that’s not going away anytime soon (if at all).

Basically, a value trap is a company that looks undervalued on paper but continues to destroy shareholder value over time.

- A value trap is a stock that looks cheap based on valuation ratios but continues to perform poorly because the underlying business is declining.

- Value traps are usually associated with declining earnings, weak(ening) competitive positions, or excessive debt.

- The most dangerous risk with value traps is permanent loss of capital.

- This is why successful value investing focuses on business quality first, then valuation, not the other way around.

Why Value Traps Are So Dangerous

The biggest risk with value traps isn’t volatility, it’s the potdential for the permanent loss of capital.

It can be tempting to assume that a low valuation automatically means upside potential. However, if a company’s overall business quality is deteriorating, its “cheap” valuation may be totally justified. In these cases, it’s not uncommon for the business to keep getting weaker over time, causing the stock to stagnate or continue falling for years.2

Common Characteristics of a Value Trap

Value traps usually share a few underlying problems, even though they can look extremely different on the surface.

One common sign is declining fundamentals. Revenues may be shrinking, margins may be compressing, or the company may be losing competitive advantage (aka have a decreasing moat). Another frequent issue is high leverage. Debt can magnify small operational problems into serious financial stress, even if earnings look stable at the moment.3

Value traps also tend to be more common in structurally difficult industries (e.g. businesses facing long-term disruption, regulation, or declining demand). In these cases, low valuation multiples tend to signal a bleak future, not a market mistake.3

Case Study

BlackBerry vs. Microsoft (2012-2013)

A great example of how valuation alone doesn’t tell the full story is the difference between BlackBerry and Microsoft in the early 2010s.

Both companies were struggling to adjust to a rapidly changing and newly mobile-first world. And although BlackBerry’s valuation at the time looked more attractive, their long term performance (and their shareholders) told very different stories.

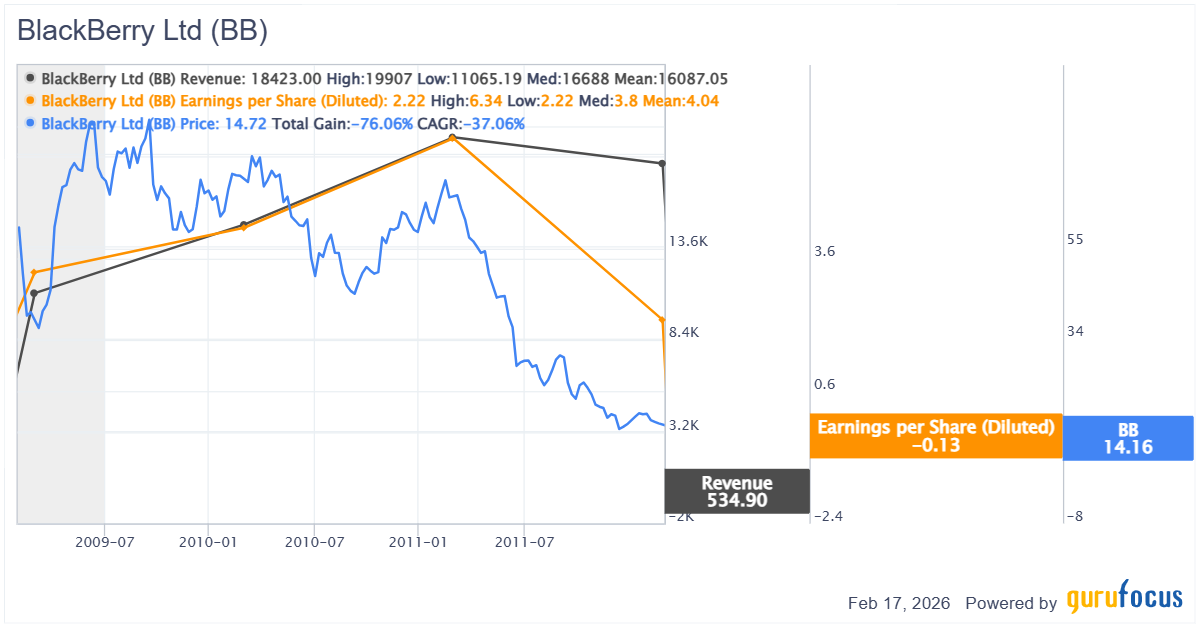

In 2012, BlackBerry traded at roughly 0.4x sales and 0.7x book value. By traditional metrics, it screamed cheap value stock.4, 5 Microsoft, on the other hand, traded at roughly 3x sales (a significant premium compared to BlackBerry).6

To many investors that focused only on valuation, BlackBerry looked like a bargain. BlackBerry's low valuation, however, wasn't opportunity.

By this point the company's competitive moat was rapidly evaporating as consumers and enterprises abandoned its platform for iPhones and Android devices.

Despite the company’s attempts to pivot its entire business to software and security services, the stock fell from the $15-18 range to $6-8 for years, delivering (what are still so far) permanent losses to its investors.

Microsoft's story diverged entirely. When Satya Nadella became CEO in February 2014, he pivoted decisively to cloud computing (Azure), subscription services (Office 365), and cross-platform development.7 The "expensive" stock at $35 in 2013 would surge past $400 by 2024, becoming one of the decade's best-performing investments.6

This goes to show that cheapness in and of itself does not make a good investment; growth and durability are required for long term investors.

How Invest Like a Guru Thinks About Value Traps

The book Invest Like a Guru, written by our founder and CEO Dr. Charlie Tian, outlines the typical phases of a value trap’s collapse. They tend to happen in four distinct stages:

- Stage 1 - Gross and operating margin compression

- Stage 2 - Slowing revenue growth and stagnating earnings

- Stage 3 - Earnings decline

- Stage 4 - Both revenue and earnings decline

Although this tends to be the most common shape of a value trap’s progression, any one of these stages is a red flag in and of itself.

Another factor to keep in mind is the speed of the decline. Although there’s no exact formula for this, the rule of thumb as that faster moving industries like technology will face faster declines than slower moving industries like utilities.8

- Earnings per Share (Diluted) - Net income divided by the fully diluted share count, the most widely used measure of a company's per-share profitability.

- Enterprise Value - The total value of a company including market cap, debt, and minority interest minus cash, representing the theoretical acquisition price.

- GF Score - A GuruFocus composite score from 0–100 ranking stocks across valuation, profitability, growth, momentum, and financial strength.

- Market Cap - The total market value of a company's outstanding shares, calculated by multiplying the current share price by total shares outstanding.

- Piotroski F-Score - A nine-point scoring system that evaluates a company's financial health across profitability, leverage, and operating efficiency.

- Free Cash Flow per Share - Operating cash flow minus capital expenditures divided by shares outstanding, showing discretionary cash generated per share.

- Book Value per Share - A company's total shareholders' equity divided by shares outstanding, representing the per-share net asset value on the books.

- Revenue per Share - Total revenue divided by shares outstanding, a top-line productivity metric showing how much sales each share represents.

Conclusion

Value traps are a powerful reminder that price and value are not the same thing. A stock trading at a low P/E or P/B ratio isn't necessarily a bargain… it might just be the market's accurate assessment of a deteriorating business.

GuruFocus makes this easy with our "Potential Value Trap" warnings. Our models identify underlying red flags (such as margin compression, financial instability, etc.) to effortlessly notify you of potential value traps.

The most important thing to remember is that the difference between a value trap and a true value investment comes down to business quality. Companies like BlackBerry had weak fundamentals disguised by attractive multiples, while companies like Microsoft had an incredibly strong underlying business that was temporarily mispriced by the market.

Successful value investing requires the discipline to distinguish between these two scenarios: Is the business facing temporary headwinds it can overcome, or permanent decline it can’t?

- https://www.wallstreetprep.com/knowledge/value-trap/

- https://www.nasdaq.com/articles/cheaper-isnt-always-better-how-avoid-stock-value-trap

- https://www.fdcapital.co.uk/how-cfos-recognise-value-traps-early/

- https://business.time.com/2013/12/20/blackberry-from-worlds-hottest-tech-company-to-what/

- https://www.gurufocus.com/stock/BB/summary?search=bb

- https://www.gurufocus.com/stock/MSFT/summary?search=msft

- https://news.microsoft.com/source/2014/10/20/clouddaypr/

- Invest Like a Guru

Explore More Financial Insights

Dive deeper into company fundamentals, trends, and ideas with GuruFocus's comprehensive Stock Screeners and Financial Data tools.

About Us | Site Map | Terms of Use | Privacy Policy | Contact Us

© 2025 GuruFocus.com. All Rights Reserved.