Helen of Troy is a diversified producer of brand name products that generates tons of cash but trades at a low price. The company can be purchased at 10x TTM earnings and 8.5x projected earnings with a safe balance sheet and a business that can continue to earn in any economic climate. While top line growth is a product of acquisitions, the bottom line has steadily increased over the years.

Sales and earnings were $300m and $17m respectively in 2000. By 2010, they have grown to $650m and $71m. While sales just over doubled, profits quadrupled. Most of the progress happened from 2000-2004. From 2005-2010, sales have hovered between $581m and $652m and profits between $49m and $76m. The company’s fiscal year ends in February, so Fiscal 2009, when the company earned $49m excluding an impairment, includes most of the carnage of the recession. From 2005-2010, the company averaged $59m a year in net income. The company is a tremendous generator of FCF though, spending an annual average of $7m on capex in the past 3 years, while recording depreciation of $15m. The growth of the company has come from acquisitions, which leads to pessimism from Wall Street analysts. The company has not been a rip-roaring growth story, but the acquisitions have worked out a lot more times than not.

The crown jewel of this company is OXO, a strong brand the that produces a lot of kitchen related products and is expanding product offerings. The company has been releasing more than 100 new products a year under this brand and being growing sales and profits. They are expanding into childcare products such as strollers this year. The things that should be taken away from this division are that it shows how the company is good at developing brands and products (they bought OXO in 2004 and have done a tremendous job in growing it). The growth rate has been slowing lately to the high single digits, but the segment has the best margins.

Peter Lynch, among other investors, will tell you to buy what you know. I’m familiar with the OXO brand from a few kitchen tools like spatulas or peelers and think the brand definitely has a lot of power and can be expanded. While people may only buy one pizza cutter, a positive experience will resonate and carry over to their plastic containers or garden tools for instance.

The other division of the company is personal care products that range form hair dryers to foot baths and shampoo. The company has long term licenses to brands or outright owns brands that it puts on a variety of goods you can find in pharmacies or stores like Target and Walmart. For instance, they have a license for the Dr. Scholl’s brand name for foot baths. They are able to sell a relatively simple product, but piggyback on the visibility of the brand recognition to drive sales, acquire shelf space, and gain a degree of pricing power.

There are other brands the personal care division represents, but there is a similar dynamic to the housewares division. The company tries to continually release new products and updates under these brands. The brands have huge mindshare of customers, and HELE’s products benefit from the positive association. The brand name owners have to approve the products as well, so the company is going to consistently release products that remain relevant to the brand and fully leverage its strengths.

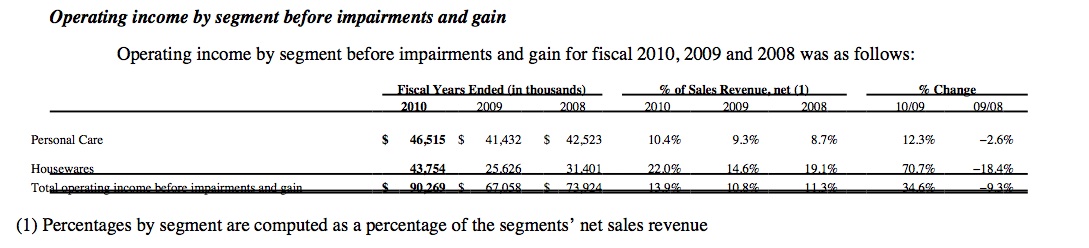

What the market seems to fail to recognize is that while maybe the personal care segment is boring, the houseware segment is pretty valuable:

The houseware segment has better margins and plenty of growth lies ahead. The growth has slowed and this has analysts worried that the stock is now dead money. Both segments generate plenty of cash though, which the company has been reinvesting in bolt on acquisitions. In 2010, the company acquired Pert Plus and Sure for $69m from Innovative Brands (the company should earn ~12m in 2010, $9m for the company due to the timing of the acquisition) and Kaz for $265m from the founding family and a private equity group. Kaz is of the same breed as Helen of Troy, using brands such as Vicks on humidifiers it sells. In 2009, the company acquired Infusium shampoos from Procter & Gamble for $60m. All these acquisitions are immediately accretive to earnings, expand the company’s offerings, and leverage the company’s relationship with customers.

The last part about leveraging the company’s relationship is key. It is a reinforcing mechanism, because the large companies (Walmart, Target, CVS, Walgreens) prefer to deal with fewer suppliers. In 2003, Walmart accounted for 30% of sales. Now it only accounts for 20% of sales. It’s largest 5 customers account for 45% of sales. Once the company gains a foothold on a store’s shelves, it can start pushing other products onto shelves as well, expanding its revenue base. As the company acquires more brands, it can fill in any gaps in their distribution or its own. As with Infusium, it can pay more attention to a $60m brand than P&G will, further wringing out sales that could only be realized if the brand was separated from P&G. The acquisitions are also done at good prices.

Kaz has the Vicks and Honeywell brand names for products, along with a few others. The Honeywell name has great recognition and signifies quality, and so throwing it on a machine like a fan gives people more confidence than if it said “Frog’s Kiss Fans” on it. Kaz is very much in line with the company’s business and operations, and there are real cost cutting opportunities that can be achieved such as consolidating regional offices and distribution.

Kaz gives the company a greater foreign footprint, further diversifies the product lines, and was done at a price of 7x adjusted EBITDA (this is the figure the company gives) while the company trades at around 9x EBITDA. I think the acquisition will be successful and the company’s past history or acquisitions has been a net positive.

The acquisition of Kaz boosted the company from having a small net debt position, to around $260m net debt. The company has proven fairly stable and has under a 3x debt/TTM EBITDA ratio, which is manageable and not excessive. Kaz should boost cash flow as well, and the company has forecasted a $0.50 increase in EPS for 2011 to $3.50. This is mostly, if not all, attributable to the Kaz acquisition. Even trimming down managements forecast to $3/share puts the current value at less than 10x earnings.

The CEO has been running the company for years and owns 1.6m shares worth around $45m, so the company is in reliable and properly incentivized hands. The CEO recently sold 40,000 shares, but I don’t take this negatively. The CEO still owns a huge block of shares and the reasons for selling can be plentiful.

A very crude 10 year DCF having the company have no growth and generate $100m in FCF with an exit multiple of 6x FCF of $100m values the company at $1.1B NPV. The past record of success indicates that any FCF reinvested in the business will be done so wisely. The company is currently trading as if it will generate $75m in FCF annually and sell out for a 6x FCF of $75m in 10 years. Barring any huge economic shocks like those seen in 2008, the company is operating at a level that earns well over this hurdle.

The major risk is commodity prices. The company is exposed to copper and oil due to the electrical components, chemicals, and packaging. The company’s production is mostly in the Far East, which can prove problematic if transportation rates increase. The company has never had its profits wiped out by commodity prices in 2007 and 2008, so the risk is more in dampened earnings than a dangerous scenario where the company loses money.

The company is a straightforward value stock in my opinion. The company is throwing off cash that it has been successfully reinvesting in acquisitions. At 10x earnings, the market seems to expect the company to make no money on its recent acquisitions despite a long history of profitability (absent the 2009 goodwill impairment), integrating acquisitions, and sound management. Conventional metrics of earnings and a crude DCF model indicate that the market expects very little positives to occur, and seems to expect negative news. The company is involved in an easy to understand business that faces little obsolescence risk and should continue to generate strong cash flows to protect investors on the downside.

Disclosure: Long HELE. Do your own research before investing.

[url=mailto:[email protected]]

Talk to Andrew about HELE[/url]

Sales and earnings were $300m and $17m respectively in 2000. By 2010, they have grown to $650m and $71m. While sales just over doubled, profits quadrupled. Most of the progress happened from 2000-2004. From 2005-2010, sales have hovered between $581m and $652m and profits between $49m and $76m. The company’s fiscal year ends in February, so Fiscal 2009, when the company earned $49m excluding an impairment, includes most of the carnage of the recession. From 2005-2010, the company averaged $59m a year in net income. The company is a tremendous generator of FCF though, spending an annual average of $7m on capex in the past 3 years, while recording depreciation of $15m. The growth of the company has come from acquisitions, which leads to pessimism from Wall Street analysts. The company has not been a rip-roaring growth story, but the acquisitions have worked out a lot more times than not.

The crown jewel of this company is OXO, a strong brand the that produces a lot of kitchen related products and is expanding product offerings. The company has been releasing more than 100 new products a year under this brand and being growing sales and profits. They are expanding into childcare products such as strollers this year. The things that should be taken away from this division are that it shows how the company is good at developing brands and products (they bought OXO in 2004 and have done a tremendous job in growing it). The growth rate has been slowing lately to the high single digits, but the segment has the best margins.

Peter Lynch, among other investors, will tell you to buy what you know. I’m familiar with the OXO brand from a few kitchen tools like spatulas or peelers and think the brand definitely has a lot of power and can be expanded. While people may only buy one pizza cutter, a positive experience will resonate and carry over to their plastic containers or garden tools for instance.

The other division of the company is personal care products that range form hair dryers to foot baths and shampoo. The company has long term licenses to brands or outright owns brands that it puts on a variety of goods you can find in pharmacies or stores like Target and Walmart. For instance, they have a license for the Dr. Scholl’s brand name for foot baths. They are able to sell a relatively simple product, but piggyback on the visibility of the brand recognition to drive sales, acquire shelf space, and gain a degree of pricing power.

There are other brands the personal care division represents, but there is a similar dynamic to the housewares division. The company tries to continually release new products and updates under these brands. The brands have huge mindshare of customers, and HELE’s products benefit from the positive association. The brand name owners have to approve the products as well, so the company is going to consistently release products that remain relevant to the brand and fully leverage its strengths.

What the market seems to fail to recognize is that while maybe the personal care segment is boring, the houseware segment is pretty valuable:

The houseware segment has better margins and plenty of growth lies ahead. The growth has slowed and this has analysts worried that the stock is now dead money. Both segments generate plenty of cash though, which the company has been reinvesting in bolt on acquisitions. In 2010, the company acquired Pert Plus and Sure for $69m from Innovative Brands (the company should earn ~12m in 2010, $9m for the company due to the timing of the acquisition) and Kaz for $265m from the founding family and a private equity group. Kaz is of the same breed as Helen of Troy, using brands such as Vicks on humidifiers it sells. In 2009, the company acquired Infusium shampoos from Procter & Gamble for $60m. All these acquisitions are immediately accretive to earnings, expand the company’s offerings, and leverage the company’s relationship with customers.

The last part about leveraging the company’s relationship is key. It is a reinforcing mechanism, because the large companies (Walmart, Target, CVS, Walgreens) prefer to deal with fewer suppliers. In 2003, Walmart accounted for 30% of sales. Now it only accounts for 20% of sales. It’s largest 5 customers account for 45% of sales. Once the company gains a foothold on a store’s shelves, it can start pushing other products onto shelves as well, expanding its revenue base. As the company acquires more brands, it can fill in any gaps in their distribution or its own. As with Infusium, it can pay more attention to a $60m brand than P&G will, further wringing out sales that could only be realized if the brand was separated from P&G. The acquisitions are also done at good prices.

Kaz has the Vicks and Honeywell brand names for products, along with a few others. The Honeywell name has great recognition and signifies quality, and so throwing it on a machine like a fan gives people more confidence than if it said “Frog’s Kiss Fans” on it. Kaz is very much in line with the company’s business and operations, and there are real cost cutting opportunities that can be achieved such as consolidating regional offices and distribution.

Kaz gives the company a greater foreign footprint, further diversifies the product lines, and was done at a price of 7x adjusted EBITDA (this is the figure the company gives) while the company trades at around 9x EBITDA. I think the acquisition will be successful and the company’s past history or acquisitions has been a net positive.

The acquisition of Kaz boosted the company from having a small net debt position, to around $260m net debt. The company has proven fairly stable and has under a 3x debt/TTM EBITDA ratio, which is manageable and not excessive. Kaz should boost cash flow as well, and the company has forecasted a $0.50 increase in EPS for 2011 to $3.50. This is mostly, if not all, attributable to the Kaz acquisition. Even trimming down managements forecast to $3/share puts the current value at less than 10x earnings.

The CEO has been running the company for years and owns 1.6m shares worth around $45m, so the company is in reliable and properly incentivized hands. The CEO recently sold 40,000 shares, but I don’t take this negatively. The CEO still owns a huge block of shares and the reasons for selling can be plentiful.

A very crude 10 year DCF having the company have no growth and generate $100m in FCF with an exit multiple of 6x FCF of $100m values the company at $1.1B NPV. The past record of success indicates that any FCF reinvested in the business will be done so wisely. The company is currently trading as if it will generate $75m in FCF annually and sell out for a 6x FCF of $75m in 10 years. Barring any huge economic shocks like those seen in 2008, the company is operating at a level that earns well over this hurdle.

The major risk is commodity prices. The company is exposed to copper and oil due to the electrical components, chemicals, and packaging. The company’s production is mostly in the Far East, which can prove problematic if transportation rates increase. The company has never had its profits wiped out by commodity prices in 2007 and 2008, so the risk is more in dampened earnings than a dangerous scenario where the company loses money.

The company is a straightforward value stock in my opinion. The company is throwing off cash that it has been successfully reinvesting in acquisitions. At 10x earnings, the market seems to expect the company to make no money on its recent acquisitions despite a long history of profitability (absent the 2009 goodwill impairment), integrating acquisitions, and sound management. Conventional metrics of earnings and a crude DCF model indicate that the market expects very little positives to occur, and seems to expect negative news. The company is involved in an easy to understand business that faces little obsolescence risk and should continue to generate strong cash flows to protect investors on the downside.

Disclosure: Long HELE. Do your own research before investing.

[url=mailto:[email protected]]

Talk to Andrew about HELE[/url]