(Monty Guild is currently travelling in Asia and meeting with economists and analysts. Here’s a little of what he’s seeing and hearing so far).

In Hong Kong right now, commerce is booming. The overwhelming atmosphere here is of pride, opulence, and the desire of people and businesses to display their material wealth. At the airport, Chinese travelers abound, and not just businessmen—tourists as well. In confirmation of this experience, I was told by a source at Cathay Pacific, the large Hong Kong-based airline, that the number of Chinese traveling to the U.S., Europe, Latin America, and throughout Asia has dramatically increased the load factor on the carrier’s air fleet. China has not been through the banking wringer like Europe and the U.S., people have money. Profits will surge, and so will the profits of other Asian carriers as the huge Chinese tourist market awakens and explores the world.

Accompanying the boom in commerce is inflation in food prices, hotel prices, and other costs associated with doing business. This is not surprising because even though the Hong Kong dollar being pegged to the U.S. dollar, the Chinese Yuan has risen by over 22% versus the U.S. dollar in the last five years.

We have written before about the China’s increasing openness toward the internationalization and financial convertibility of the Yuan. Many steps have been taken in this direction thus far and many more will come in the months and years ahead. A strong Yuan will help China in its fight against inflation.

Another sector that is booming as a result of individual prosperity is Hong Kong real estate. Not only are many businesses here setting up operations further into China, many wealthy mainland Chinese are also buying in Hong Kong. The traffic is heavy in both directions.

This week I also travel to Singapore. The economic boom resonates throughout the region. In Singapore, as in Hong Kong, employment is also full and real estate similarly humming. Prices are rising for both office and residential space. As a result, many Singapore companies in the real estate, banking, and manufacturing sector look quite attractive. We plan to reinvest in Singapore as soon as the current correction in Asian markets draws to a close—probably within the next few months.

After Singapore, I will visit the beautiful and magnetic Thailand. There, too, I expect to see more growth and more inflation as my U.S. dollars just don’t carry the weight they once did.

The India Scene

In consideration of the other Asian giant, India, we continue to be keen on the country’s long-term prospects. The Indian market has fallen by about 15 percent in the last few weeks, making it much less expensive. Strong inflationary pressures have led the government to raise interest rates aggressively and as a result we are not currently recommending Indian stocks. Much of the inflation problem is self-created by India’s Fabian socialist history, which has encouraged a policy of subsidizing food and energy at below market prices to some Indian users. This program leads to hoarding and sales into world markets at higher prices than those available in India, and drains important food and energy from the country, creating shortages.

Yet, India also has many fast-growing and well-managed companies. The lively entrepreneurial spirit and intelligence of the Indian people will give rise to more great companies, and after inflation is controlled, Indian stocks will provide very good buying opportunities. When prices fall lower, we will definitely buy in the Indian markets.

For those of you interested in a detailed account of impactful events taking place in this immense 1.2 billion-person country and its growing role in the global economy, check out the multi-page report in the January 28, 2011 Financial Times here: http://www.ft.com/reports/india-globalisation-2010

Sensex – BSE Sensex 30 Index (February 15, 2010 to February 15, 2011)

Meanwhile, Down UnderThe Australian summer has witnessed record floods and cyclones, resulting in multiple deaths as well as property damage, soaring into the billions of dollars. In the wake of horrific weather and destruction, Australian resources stocks have moved higher. Investors should continue to look for opportunities in iron ore, energy, base metal, and precious metals stocks in Australia.

In Europe, German Support for the Euro

In late January, Germany’s Chancellor Angela Merkel started campaigning for the rescue of the Euro. The reason is simple: Germany’s economic leadership and power is now accepted by the rest of Europe, and consequently Germany is now more willing to consider helping others in the community.

With French acquiescence, Germany is open to cooperate under the condition that other European countries meet six specific conditions. As reported in a February 4 New York Times article, those conditions are as follows:

1. Abolition of wage indexation systems,

2. Agreement on mutual recognition of education qualifications,

3. Creation of a common base for assessing corporate tax,

4. Adjustment of the pension systems,

5. Establishment of a national crisis management regime for bank,

6. New legal measures to force countries to commit to tough fiscal policies through a ‘debt alert mechanism.”

The Germans, it appears, want to encourage European nations to mimic its economic discipline and emphasis on fiscal responsibility. Frankly, we believe that the strict Germanic approach is not a bad idea at all. The question is: will it fly in countries that have a more laid back culture? There is truth to the adage that it is hard to teach old dogs new tricks, although we don’t believe it can’t be done. In fact, currently the optimists on European integration outnumber the pessimists. We share in their hope, but recognize that success is not a sure thing. We’re watching to see how the ball bounces.

What This Means to YouInvesting in Europe is still profitable, but only wise in companies that can benefit even if the German and French plan comes to naught. Investors should focus on commodity producers and exporters that will benefit from an increase in European inflation. If the Euro comes under pressure again, you will profit by holding European exporters of industrial equipment that benefit from the currency decline.

The Grain Gain

Most prices of food grains and meats are on the rise. There are many factors involved: hoarding by producers and users, investing by speculators, weather, unwise government policies, and the insatiable demand for better diets by hundreds of millions of consumers.

It’s not just the food grains either; cotton prices recently breached highs not seen since the U.S. Civil War. The connection between agriculture prices and food prices is intimate. All are used for human consumption and animal feed. Wheat, corn, soybeans, and other grains can be substituted one for another when weather, changes in lifestyle, and government policies (subsidies and price controls) combine to create a huge supply demand imbalance. This is what we now see unfolding throughout the world. Such a food shortage is the son of many mothers; although it is popular these days to point the finger at the quantitative easing (QE) programs unleashed by the U.S. Federal Reserve, and at agencies controlling the purse strings in other nations, the problem is not so simple.

We believe that the crisis in food prices has a few more months to run in the developed world, and wise investors will want to participate. For several months, we have held food grains and stocks that benefit from a farm sector trying to grow more grain and produce more meat. Farm equipment makers, fertilizer producers, and other farm suppliers all fit into this category.

Our Recommendations—In Review

Bonds

Intermediate and long-term bonds are still presenting risk of falling, and we still recommend avoiding them entirely.

Gold

Still hold gold for long-term investment. Our recommendation of late still holds: we have been bullish since June 25, 2002, when gold was selling at about $325 per ounce. We see gold moving to $1,500 and then higher. Traders should sell spikes and buy dips.

Food and Farm-related Stocks

These continue as a favorite investment target of ours. We have been bullish on grains and farm-related shares since late 2008. Continue to hold and acquire these industries on dips. The possibility of food crises in Africa, Asia and Latin America is very real.

Oil

Oil-related investments hold promise. Our bullishness dates back to February 11, 2009, when oil was trading at $35.94 per barrel.

Currencies

For long-term investment, we do not like the U.S. dollar, Japanese yen, British pound, or the Euro. Since September 14th of last year we continue to favor the Singaporean, Thai, Canadian, Swiss, Brazilian, Chinese, and Australian currencies. Use pullbacks in these currencies as an opportunity to establish long-term positions. They will rise as the U.S. dollar and European currencies fall.

Global Stock Selections

For stock investments throughout the world we base our recommendations on careful studying of individual companies and industries, always keeping in mind that companies and sectors are at differing stages of growth. In developed countries, technology, precious metals, and commodity producers (food, oil, and base metals) will all benefit from an improving economy and a developing back-to-work trend in the U.S. and Europe.

Since September 9, 2010, we have thought U.S. stocks still have enough gas in the tank for further rallying. Money is flowing into them. Liquidity formation through QE is creating demand for many assets, including U.S. stocks. A correction of 5-7 percent could occur at any time, so we suggest using this correction as a buying opportunity.

This week we are adding Japan and Australia to our list of recommended stock markets (see our comments on Australia above). As for Japan, in the coming weeks we will discuss in more detail why we think the Japanese stock market has become more attractive. In short, Asia is booming, and Japanese companies are benefitting. Japan is not presently experiencing the same inflation headwinds that have scared investors in other Asian markets. Also, because the yen looks vulnerable to decline, we recommend that investors hedge their currency exposure by shorting the yen while they are long Japanese stocks.

AS51 – S&P/ASX 200 Index (February 15, 2010 to February 15, 2011)

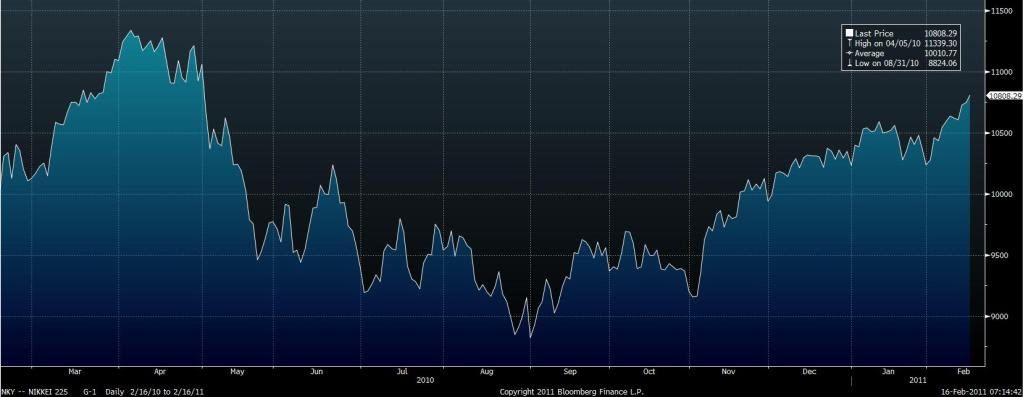

NKY – Nikkei 225 (February 15, 2010 to February 15, 2011)

We are bullish on China, South Korea, and Colombia. In Colombia’s case, half of our original position remains, and we still see it as an attractive investment.

In Hong Kong right now, commerce is booming. The overwhelming atmosphere here is of pride, opulence, and the desire of people and businesses to display their material wealth. At the airport, Chinese travelers abound, and not just businessmen—tourists as well. In confirmation of this experience, I was told by a source at Cathay Pacific, the large Hong Kong-based airline, that the number of Chinese traveling to the U.S., Europe, Latin America, and throughout Asia has dramatically increased the load factor on the carrier’s air fleet. China has not been through the banking wringer like Europe and the U.S., people have money. Profits will surge, and so will the profits of other Asian carriers as the huge Chinese tourist market awakens and explores the world.

Accompanying the boom in commerce is inflation in food prices, hotel prices, and other costs associated with doing business. This is not surprising because even though the Hong Kong dollar being pegged to the U.S. dollar, the Chinese Yuan has risen by over 22% versus the U.S. dollar in the last five years.

We have written before about the China’s increasing openness toward the internationalization and financial convertibility of the Yuan. Many steps have been taken in this direction thus far and many more will come in the months and years ahead. A strong Yuan will help China in its fight against inflation.

Another sector that is booming as a result of individual prosperity is Hong Kong real estate. Not only are many businesses here setting up operations further into China, many wealthy mainland Chinese are also buying in Hong Kong. The traffic is heavy in both directions.

This week I also travel to Singapore. The economic boom resonates throughout the region. In Singapore, as in Hong Kong, employment is also full and real estate similarly humming. Prices are rising for both office and residential space. As a result, many Singapore companies in the real estate, banking, and manufacturing sector look quite attractive. We plan to reinvest in Singapore as soon as the current correction in Asian markets draws to a close—probably within the next few months.

After Singapore, I will visit the beautiful and magnetic Thailand. There, too, I expect to see more growth and more inflation as my U.S. dollars just don’t carry the weight they once did.

The India Scene

In consideration of the other Asian giant, India, we continue to be keen on the country’s long-term prospects. The Indian market has fallen by about 15 percent in the last few weeks, making it much less expensive. Strong inflationary pressures have led the government to raise interest rates aggressively and as a result we are not currently recommending Indian stocks. Much of the inflation problem is self-created by India’s Fabian socialist history, which has encouraged a policy of subsidizing food and energy at below market prices to some Indian users. This program leads to hoarding and sales into world markets at higher prices than those available in India, and drains important food and energy from the country, creating shortages.

Yet, India also has many fast-growing and well-managed companies. The lively entrepreneurial spirit and intelligence of the Indian people will give rise to more great companies, and after inflation is controlled, Indian stocks will provide very good buying opportunities. When prices fall lower, we will definitely buy in the Indian markets.

For those of you interested in a detailed account of impactful events taking place in this immense 1.2 billion-person country and its growing role in the global economy, check out the multi-page report in the January 28, 2011 Financial Times here: http://www.ft.com/reports/india-globalisation-2010

Sensex – BSE Sensex 30 Index (February 15, 2010 to February 15, 2011)

Meanwhile, Down UnderThe Australian summer has witnessed record floods and cyclones, resulting in multiple deaths as well as property damage, soaring into the billions of dollars. In the wake of horrific weather and destruction, Australian resources stocks have moved higher. Investors should continue to look for opportunities in iron ore, energy, base metal, and precious metals stocks in Australia.

In Europe, German Support for the Euro

In late January, Germany’s Chancellor Angela Merkel started campaigning for the rescue of the Euro. The reason is simple: Germany’s economic leadership and power is now accepted by the rest of Europe, and consequently Germany is now more willing to consider helping others in the community.

With French acquiescence, Germany is open to cooperate under the condition that other European countries meet six specific conditions. As reported in a February 4 New York Times article, those conditions are as follows:

1. Abolition of wage indexation systems,

2. Agreement on mutual recognition of education qualifications,

3. Creation of a common base for assessing corporate tax,

4. Adjustment of the pension systems,

5. Establishment of a national crisis management regime for bank,

6. New legal measures to force countries to commit to tough fiscal policies through a ‘debt alert mechanism.”

The Germans, it appears, want to encourage European nations to mimic its economic discipline and emphasis on fiscal responsibility. Frankly, we believe that the strict Germanic approach is not a bad idea at all. The question is: will it fly in countries that have a more laid back culture? There is truth to the adage that it is hard to teach old dogs new tricks, although we don’t believe it can’t be done. In fact, currently the optimists on European integration outnumber the pessimists. We share in their hope, but recognize that success is not a sure thing. We’re watching to see how the ball bounces.

What This Means to YouInvesting in Europe is still profitable, but only wise in companies that can benefit even if the German and French plan comes to naught. Investors should focus on commodity producers and exporters that will benefit from an increase in European inflation. If the Euro comes under pressure again, you will profit by holding European exporters of industrial equipment that benefit from the currency decline.

The Grain Gain

Most prices of food grains and meats are on the rise. There are many factors involved: hoarding by producers and users, investing by speculators, weather, unwise government policies, and the insatiable demand for better diets by hundreds of millions of consumers.

It’s not just the food grains either; cotton prices recently breached highs not seen since the U.S. Civil War. The connection between agriculture prices and food prices is intimate. All are used for human consumption and animal feed. Wheat, corn, soybeans, and other grains can be substituted one for another when weather, changes in lifestyle, and government policies (subsidies and price controls) combine to create a huge supply demand imbalance. This is what we now see unfolding throughout the world. Such a food shortage is the son of many mothers; although it is popular these days to point the finger at the quantitative easing (QE) programs unleashed by the U.S. Federal Reserve, and at agencies controlling the purse strings in other nations, the problem is not so simple.

We believe that the crisis in food prices has a few more months to run in the developed world, and wise investors will want to participate. For several months, we have held food grains and stocks that benefit from a farm sector trying to grow more grain and produce more meat. Farm equipment makers, fertilizer producers, and other farm suppliers all fit into this category.

Our Recommendations—In Review

Bonds

Intermediate and long-term bonds are still presenting risk of falling, and we still recommend avoiding them entirely.

Gold

Still hold gold for long-term investment. Our recommendation of late still holds: we have been bullish since June 25, 2002, when gold was selling at about $325 per ounce. We see gold moving to $1,500 and then higher. Traders should sell spikes and buy dips.

Food and Farm-related Stocks

These continue as a favorite investment target of ours. We have been bullish on grains and farm-related shares since late 2008. Continue to hold and acquire these industries on dips. The possibility of food crises in Africa, Asia and Latin America is very real.

Oil

Oil-related investments hold promise. Our bullishness dates back to February 11, 2009, when oil was trading at $35.94 per barrel.

Currencies

For long-term investment, we do not like the U.S. dollar, Japanese yen, British pound, or the Euro. Since September 14th of last year we continue to favor the Singaporean, Thai, Canadian, Swiss, Brazilian, Chinese, and Australian currencies. Use pullbacks in these currencies as an opportunity to establish long-term positions. They will rise as the U.S. dollar and European currencies fall.

Global Stock Selections

For stock investments throughout the world we base our recommendations on careful studying of individual companies and industries, always keeping in mind that companies and sectors are at differing stages of growth. In developed countries, technology, precious metals, and commodity producers (food, oil, and base metals) will all benefit from an improving economy and a developing back-to-work trend in the U.S. and Europe.

Since September 9, 2010, we have thought U.S. stocks still have enough gas in the tank for further rallying. Money is flowing into them. Liquidity formation through QE is creating demand for many assets, including U.S. stocks. A correction of 5-7 percent could occur at any time, so we suggest using this correction as a buying opportunity.

This week we are adding Japan and Australia to our list of recommended stock markets (see our comments on Australia above). As for Japan, in the coming weeks we will discuss in more detail why we think the Japanese stock market has become more attractive. In short, Asia is booming, and Japanese companies are benefitting. Japan is not presently experiencing the same inflation headwinds that have scared investors in other Asian markets. Also, because the yen looks vulnerable to decline, we recommend that investors hedge their currency exposure by shorting the yen while they are long Japanese stocks.

AS51 – S&P/ASX 200 Index (February 15, 2010 to February 15, 2011)

NKY – Nikkei 225 (February 15, 2010 to February 15, 2011)

We are bullish on China, South Korea, and Colombia. In Colombia’s case, half of our original position remains, and we still see it as an attractive investment.