Have you ever seen a company that actually earns more when you dilute the number of shares outstanding? Artio Global Investors (ART, Financial) presents an opportunity for the analytical mind, because it actually earns more when you dilute the number of shares. There are many market dynamics and gross misunderstandings that have caused unwarranted pressure on the stock. The company has a strong business model and trades in an unloved sector of an unloved sector: international asset management. I've discussed why asset managers can be such an attractive investment previously. The company trades at a low multiple of earnings and at a discount to peers.

Background

The company was spun of from Julius Baer in 2009. The company’s cornerstone investment product is an international equity fund started in 1995, with a sister fund started several years after due to the increasing size of the first fund. The company has since expanded its offerings to diversify its product line up and take advantage of their position as a respected international investor. The spinoff did not immediately result in a drop in the share price, although the structure of the spinoff is somewhat confusing. The company has not been helped by the lack of popularity in equity markets and the constantly shifting institutional allocation to various strategies.

Spinoff

The company was spun off with 3 classes of shares (A, B, and C), obscuring the earnings power of the entire company and created an overhang of excess liquidity. Class A shares are the basic publicly traded shares with no special features. Class B shares were the holdings of the two principals Mr. Pell and Mr. Younes, who are the CEO/CIO and Head of International Equity respectively, which entitled them to some profits, but have converted into Class A shares or are still in the process. They have been allowed to sell 20% of their holdings each quarter, and have sold a portion, bringing their combined ownership stake from ~30% to 19%. Class C shares are solely held by GAM Holdings, the Julius Baer parent company, and entitle it to a share of the profits. Within 2 years of the spin, all of these shares will be converted to Class A shares, of which 60 million will be outstanding. GAM Holdings has stated that the Artio shares are a financial stake as opposed to strategic stake. The shares will convert in Class A shares in October 2011 at the latest, giving the looming threat of additional excess liquidity. The principals own 1% each of the holding company that contains the Artio business. The 60 million shares outstanding represent 98% of the underlying company.

Inside Ownership

There’s a balance between the stock price and inside ownership situation. A lot of the liquidity in the stock is the result of the principals selling shares in the company. While insider buying is a universally bullish signal on a stock, a more nuanced view is necessary on insider selling. It is simultaneously discomforting and irrelevant. As long as the principals hold a meaningful stake in the company, there is a strong alignment of incentives. Now that the company is public, 2m shares in the form of RSU’s were issued to non-senior employees, which vest over the next 3 years. This further entrenches an alignment of interests in the entire operation and mitigates the potential dilution of aligned interests through the sales of the principals.

Without getting philosophical about what stake for the principals to hold would be considered “meaningful,” I would point out that there is a combined ~$200m of stock held by them still. They have gotten a fair amount of cash from selling some of their holdings, and it remains to be seen what they will do as they are allowed to sell more of their shares. This being the real world and considering that most managers are not Warren Buffett (who still has substantial wealth absent his stake in Berkshire), I’m not exactly shocked that they would look to diversify their wealth. While it is not the ideal situation, you are not paying a price for a stock that people expect to be everything but ideal. The principals also own 2% of the underlying company, which means they get 1% of the company’s profits passed through to them. This could potentially be destructive were they to do dilutive things with the other 98% of the shares to increase overall profits, but this 1% is outweighed by their public shares.

Valuation

This is the downside case based on the derivative earnings and EV/AUM valuations based on drops in AUM. The expenses are overstated by using 2010 expenses. There is greater variability in expenses if AUM/performance declines. Any upside through increases in AUM/positive performance is not accounted for. These various valuation situations reveal a margin of safety in spite of potential volatility in markets.

Downside and Risks

The company’s revenue is completely derivative of its assets under management. The main way to retain and attract more/grow AUM is performance. The long term performance metrics of its core strategies are industry leading, although recent performance has been disappointing. While it is difficult to allocate the blame, the recent outflow of assets is attributable to performance as well as changing institutional portfolio balancing. The International Equity funds (their flagship product) has underperformed the index in the past 1 and 3 year periods, which have slowed down the growth in the company. They haven’t done horrible by mutual fund standards and they’ve outperformed the index since inception. There is a risk the fund has “lost it” but it is the same people who have been running it since inception. If this is more than a temporary dip in performance, more assets could flow out.

Potential Upside

There is some upside potential in new fund launches. Their US equity funds are still small and have had a hard time since they launched in 2006. They have a High Yield Fund as well as a High Grade Fixed income fund with $4bn in AUM each. They’ve just launched a Local Emerging Markets Debt Fund (LEMD) , which is a logical extension of the international bent of the company as well as complimentary to their already established fixed income team. While no additional valued is assumed from the US equity or LEMD funds, the LEMD fund has strong potential to attract several billion more in AUM.

Additional Catalysts

The company has a buyback approved, which should be easy to complete with the low stock price and tons of FCF the company throws off. Increasing the dividend is another possibility. While I realize this does not quite constitute startling insight, the payout ratio is 10%.

As stated, the company throws off tons of cash flow. They have casually acknowledged the possibility of an acquisition. Done at a reasonable multiple – and most of the sector is not expensive – it might have the unexpected effect of boosting the stock price. It would give the company much needed diversity as it is considered mostly a one trick pony at this point with its International Equity fund family.

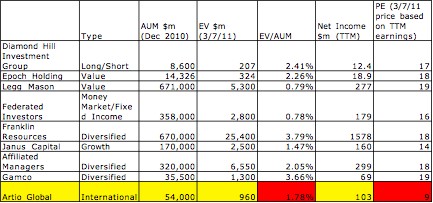

Comparisons

If you can point out errors in the comps, you can win a cookie. I used SEC filings, but I did not make many adjustments. I excluded Calamos Asset Management and AllianceBernstein because there were substantial adjustments to make due to their structure, and I wasn't sure if I was going to do it properly. Legg Mason is working through some of its own problems with the fall of Bill Miller and issues with money markets. Federated Investors core business has a lot less stickiness in it (money markets) and the fees earned are a lot lower. While the P/E multiple can be subject to manipulations, it is worth noting that money managers typically trade at above market valuations. I don't have a favored integer for the PE multiple, but 9 is definitely too low for Artio considering the many advantages of the the asset manager business model. An asset manager that trades OTC and is a real minnow that I wrote up a while ago, Hennessy Advisors, now sports a higher valuation with its recent run up.

Conclusion - The margin of safety on the downside is great enough that I'm not worried too much about where the upside will come from. From a pure valuation standpoint, Artio Global is cheap. There are no blemishes, outside of its concentrated fund offerings, that lead me to believe the company should trade at such a substantial discount to peers.

Disclosure: Long ART

Background

The company was spun of from Julius Baer in 2009. The company’s cornerstone investment product is an international equity fund started in 1995, with a sister fund started several years after due to the increasing size of the first fund. The company has since expanded its offerings to diversify its product line up and take advantage of their position as a respected international investor. The spinoff did not immediately result in a drop in the share price, although the structure of the spinoff is somewhat confusing. The company has not been helped by the lack of popularity in equity markets and the constantly shifting institutional allocation to various strategies.

Spinoff

The company was spun off with 3 classes of shares (A, B, and C), obscuring the earnings power of the entire company and created an overhang of excess liquidity. Class A shares are the basic publicly traded shares with no special features. Class B shares were the holdings of the two principals Mr. Pell and Mr. Younes, who are the CEO/CIO and Head of International Equity respectively, which entitled them to some profits, but have converted into Class A shares or are still in the process. They have been allowed to sell 20% of their holdings each quarter, and have sold a portion, bringing their combined ownership stake from ~30% to 19%. Class C shares are solely held by GAM Holdings, the Julius Baer parent company, and entitle it to a share of the profits. Within 2 years of the spin, all of these shares will be converted to Class A shares, of which 60 million will be outstanding. GAM Holdings has stated that the Artio shares are a financial stake as opposed to strategic stake. The shares will convert in Class A shares in October 2011 at the latest, giving the looming threat of additional excess liquidity. The principals own 1% each of the holding company that contains the Artio business. The 60 million shares outstanding represent 98% of the underlying company.

Inside Ownership

There’s a balance between the stock price and inside ownership situation. A lot of the liquidity in the stock is the result of the principals selling shares in the company. While insider buying is a universally bullish signal on a stock, a more nuanced view is necessary on insider selling. It is simultaneously discomforting and irrelevant. As long as the principals hold a meaningful stake in the company, there is a strong alignment of incentives. Now that the company is public, 2m shares in the form of RSU’s were issued to non-senior employees, which vest over the next 3 years. This further entrenches an alignment of interests in the entire operation and mitigates the potential dilution of aligned interests through the sales of the principals.

Without getting philosophical about what stake for the principals to hold would be considered “meaningful,” I would point out that there is a combined ~$200m of stock held by them still. They have gotten a fair amount of cash from selling some of their holdings, and it remains to be seen what they will do as they are allowed to sell more of their shares. This being the real world and considering that most managers are not Warren Buffett (who still has substantial wealth absent his stake in Berkshire), I’m not exactly shocked that they would look to diversify their wealth. While it is not the ideal situation, you are not paying a price for a stock that people expect to be everything but ideal. The principals also own 2% of the underlying company, which means they get 1% of the company’s profits passed through to them. This could potentially be destructive were they to do dilutive things with the other 98% of the shares to increase overall profits, but this 1% is outweighed by their public shares.

Valuation

This is the downside case based on the derivative earnings and EV/AUM valuations based on drops in AUM. The expenses are overstated by using 2010 expenses. There is greater variability in expenses if AUM/performance declines. Any upside through increases in AUM/positive performance is not accounted for. These various valuation situations reveal a margin of safety in spite of potential volatility in markets.

Downside and Risks

The company’s revenue is completely derivative of its assets under management. The main way to retain and attract more/grow AUM is performance. The long term performance metrics of its core strategies are industry leading, although recent performance has been disappointing. While it is difficult to allocate the blame, the recent outflow of assets is attributable to performance as well as changing institutional portfolio balancing. The International Equity funds (their flagship product) has underperformed the index in the past 1 and 3 year periods, which have slowed down the growth in the company. They haven’t done horrible by mutual fund standards and they’ve outperformed the index since inception. There is a risk the fund has “lost it” but it is the same people who have been running it since inception. If this is more than a temporary dip in performance, more assets could flow out.

Potential Upside

There is some upside potential in new fund launches. Their US equity funds are still small and have had a hard time since they launched in 2006. They have a High Yield Fund as well as a High Grade Fixed income fund with $4bn in AUM each. They’ve just launched a Local Emerging Markets Debt Fund (LEMD) , which is a logical extension of the international bent of the company as well as complimentary to their already established fixed income team. While no additional valued is assumed from the US equity or LEMD funds, the LEMD fund has strong potential to attract several billion more in AUM.

Additional Catalysts

The company has a buyback approved, which should be easy to complete with the low stock price and tons of FCF the company throws off. Increasing the dividend is another possibility. While I realize this does not quite constitute startling insight, the payout ratio is 10%.

As stated, the company throws off tons of cash flow. They have casually acknowledged the possibility of an acquisition. Done at a reasonable multiple – and most of the sector is not expensive – it might have the unexpected effect of boosting the stock price. It would give the company much needed diversity as it is considered mostly a one trick pony at this point with its International Equity fund family.

Comparisons

If you can point out errors in the comps, you can win a cookie. I used SEC filings, but I did not make many adjustments. I excluded Calamos Asset Management and AllianceBernstein because there were substantial adjustments to make due to their structure, and I wasn't sure if I was going to do it properly. Legg Mason is working through some of its own problems with the fall of Bill Miller and issues with money markets. Federated Investors core business has a lot less stickiness in it (money markets) and the fees earned are a lot lower. While the P/E multiple can be subject to manipulations, it is worth noting that money managers typically trade at above market valuations. I don't have a favored integer for the PE multiple, but 9 is definitely too low for Artio considering the many advantages of the the asset manager business model. An asset manager that trades OTC and is a real minnow that I wrote up a while ago, Hennessy Advisors, now sports a higher valuation with its recent run up.

Conclusion - The margin of safety on the downside is great enough that I'm not worried too much about where the upside will come from. From a pure valuation standpoint, Artio Global is cheap. There are no blemishes, outside of its concentrated fund offerings, that lead me to believe the company should trade at such a substantial discount to peers.

Disclosure: Long ART