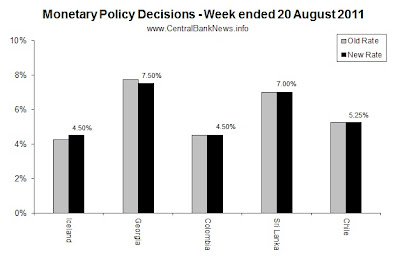

The past week in monetary policy saw just 5 central banks meeting to review monetary policy settings. Those that changed interest rates were: Iceland +25bps to 4.50% and Georgia -25bps to 7.50%. Meanwhile those that held interest rates unchanged were: Colombia 4.50%, Sri Lanka 7.00%, and Chile 5.25%. Elsewhere the Monetary Authority of Singapore released a statement affirming is monetary policy stance, following significant financial market movements. Similarly the Swiss National Bank announced even further measures to counter the strong Swiss franc. Also on the radar was the ECB releasing data showing in the week ending the 12th of August it had spent 22 billion euros on bond purchases as part of its SMP.

One of the most common themes in the monetary policy statements of the banks that met last week was concerns about slowing growth in the EU and US. Likewise most of the central banks also noted the heightened levels of risk aversion and volatility in financial markets over the past few weeks; largely a result of concerns on the sovereign debt situation in the US with the debt level debate and credit rating downgrade. As for the Eurozone, continued sovereign debt trouble and fears of contagion, with as yet seemingly only temporary solutions, also detracted from confidence levels. However, on their own economies the central banks were much more optimistic, reflecting the fact that most of the central banks in question were in emerging market economies.

Listed below are some of the key quotes from the monetary policy statements:

Looking to the central bank calendar, the key events in central banking in the week ahead include the central bank meetings listed below, but also on the agenda later in the week is the speech scheduled by Ben Bernanke, Chairman of the US Federal Reserve, at the Jackson Hole symposium in Wyoming, USA.

Source: www.CentralBankNews.info

Article source: http://www.centralbanknews.info/2011/08/monetary-policy-week-in-review-20.html

One of the most common themes in the monetary policy statements of the banks that met last week was concerns about slowing growth in the EU and US. Likewise most of the central banks also noted the heightened levels of risk aversion and volatility in financial markets over the past few weeks; largely a result of concerns on the sovereign debt situation in the US with the debt level debate and credit rating downgrade. As for the Eurozone, continued sovereign debt trouble and fears of contagion, with as yet seemingly only temporary solutions, also detracted from confidence levels. However, on their own economies the central banks were much more optimistic, reflecting the fact that most of the central banks in question were in emerging market economies.

Listed below are some of the key quotes from the monetary policy statements:

- Central Bank of Iceland (increased rate 25bps to 4.50%): "The interest rate increase is in accordance with recent MPC statements and reflects the fact that the inflation outlook for the coming two years has deteriorated still further since the Committee's last meeting," and noted "It is necessary to act now to contain inflation and reduce potential pressure on the krona".

- National Bank of Georgia (decreased rate -25bps to 7.50%): (translated) the high rate of inflation (8.5% in July) was mainly driven by food price rises (6.7%), and it expects inflation to reduce in the coming months; towards target by the end of the current year. The interest rate decrease was preventative in nature, in order to keep inflation around the target level in the medium term. The Bank also noted the economic growth risks in the US and eurozone economies; commenting that it may ease pressure on commodity prices, but also impact on global growth risks.

- Central Bank of Colombia (held rate at 4.50%): "The board considered it prudent to pause in interest rate increases, especially given the high uncertainty in international financial markets and their potential negative effect on the growth of the world economy in general, and Colombia in particular,". On its own economy, the Bank said (translated): "the Colombian economy maintained good growth, driven primarily by strong household consumption. Indicators of consumer confidence and the industry continue at high levels and the growth of credit to households and businesses continue to grow in an environment of real interest rates below their historical averages. The GDP growth forecasts published in the last Inflation Report remain unchanged".

- Central Bank of Sri Lanka (held rate at 7.00%): "with the continuous improvements in the supply of most food items, inflation is expected to moderate in the coming months," and further noted that "the central bank will continue to closely monitor the growth of monetary aggregates and will implement appropriate measures if demand-side pressures in the economy increase."

- Central Bank of Chile (held rate at 5.25%): "Domestically, output, demand and labor market figures are evolving strongly and are showing signs of moderation at the margin. However, in the case of product and demand,such moderation has been less than foreseen in the baseline scenario of June's MonetaryPolicy Report. CPI inflation has hovered around 3% y”o”y while measures of core inflationremain bounded. Inflation expectations show a significant decline and are close to the target."

Looking to the central bank calendar, the key events in central banking in the week ahead include the central bank meetings listed below, but also on the agenda later in the week is the speech scheduled by Ben Bernanke, Chairman of the US Federal Reserve, at the Jackson Hole symposium in Wyoming, USA.

- PLN - Poland (National Bank of Poland) - expected to hold at 4.50% on the 23rd of August

- HUF - Hungary (Magyar Nemzeti Bank) - expected to hold at 6.00% on the 23rd of August

- TRY - Turkey (Central Bank of Turkey) - expected to hold at 5.75% on the 23rd of August

- THB - Thailand (Bank of Thailand) - expected to hold at 3.25% on the 24th of August

- MXN - Mexico (Banco de Mexico) - expected to hold at 4.50% on the 26th of August

Source: www.CentralBankNews.info

Article source: http://www.centralbanknews.info/2011/08/monetary-policy-week-in-review-20.html