In his 2006 paper, “The Little Note That Beats the Markets” James Montier backtested the Magic Formula and found that it supported the claim in the “Little Book That Beats The Market” that the Magic Formula does in fact beat the market:

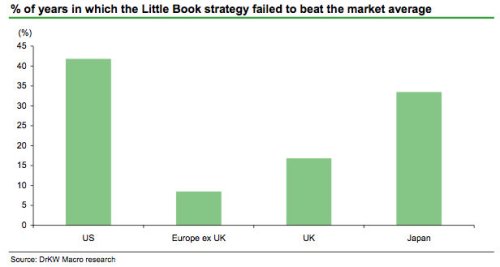

Europe and the UK show surprisingly few years of historic market underperformance. Montier says investors should “bear in mind the lessons from the US and Japan, where underperformance has been seen on a considerably more frequent basis:”

The results certainly support the notions put forward in the Little Book. In all the regions, the Little Book strategy substantially outperformed the market, and with lower risk! The range of outperformance went from just over 3.5% in the US to an astounding 10% in Japan.Regardless, Montier felt that investors would struggle to implement the strategy for behavioral reasons:

…

The results of our backtest suggest that Greenblatt’s strategy isn’t unique to the US. We tested the Little Book strategy on US, European, UK and Japanese markets between 1993 and 2005. The results are impressive. The Little Book strategy beat the market (an equally weighted stock index) by 3.6%, 8.8%, 7.3% and 10.8% in the various regions respectively. And in all cases with lower volatility than the market! The outperformance was even better against the cap weighted indices.

Greenblatt suggests two reasons why investors will struggle to follow the Little Book strategy. Both ring true with us from our meeting with investors over the years. The first is “investing by using a magic formula may take away some of the fun”. Following a quant model or even a set of rules takes a lot of the excitement out of stock investing. What would you do all day if you didn’t have to meet companies or sit down with the sell side?The chart below shows the proportion of years within Montier’s sample where the Magic Formula failed to beat the market in each of the respective regions.

As Keynes noted “The game of professional investment is intolerably boring and over- exacting to anyone who is entirely exempt from the gambling instinct; whilst he who has it must pay to this propensity the appropriate toll”.

Secondly, the Little Book strategy, and all value strategies for that matter, requires patience. And patience is in very short supply amongst investors in today’s markets. I’ve even come across fund managers whose performance is monitored on a daily basis – congratulations are to be extended to their management for their complete mastery of measuring noise! Everyone seems to want the holy grail of profits without any pain. Dream on. It doesn’t exist.

Value strategies work over the long run, but not necessarily in the short term. There can be prolonged periods of underperformance. It is these periods of underperformance that ensure that not everyone becomes a value investor (coupled with a hubristic belief in their own abilities to pick stocks).

As Greenblatt notes “Imagine diligently watching those stocks each day as they do worse than the market averages over the course of many months or even years… The magic formula portfolio fared poorly relative to the market average in 5 out of every 12 months tested. For full-year periods… failed to beat the market averages once every four years”.

Europe and the UK show surprisingly few years of historic market underperformance. Montier says investors should “bear in mind the lessons from the US and Japan, where underperformance has been seen on a considerably more frequent basis:”

It is this periodic underperformance that really helps ensure the survival of such strategies. As long as investors continue to be overconfident in their abilities to consistently pick winners, and myopic enough that even a year of underperformance is enough to send them running, then strategies such as the Little Book are likely to continue to do well over the long run. Thankfully for those of us with faith in such models, the traits just described seem to be immutable characteristics of most people. As Warren Buffet said “Investing is simple but not easy”.Montier has long promoted the theme that the reason value investors underperform value models is due to behavioral errors and cognitive biases. For example, in his excellent 2006 research report Painting By Numbers: An Ode To Quant Montier attributes most of the underperformance to overconfidence:

We all think that we know better than simple models. The key to the quant model’s performance is that it has a known error rate while our error rates are unknown.Greenblatt has conducted a study on exactly this point. More tomorrow.

The most common response to these findings is to argue that surely a fund manager should be able to use quant as an input, with the flexibility to override the model when required. However, as mentioned above, the evidence suggests that quant models tend to act as a ceiling rather than a floor for our behaviour. Additionally there is plenty of evidence to suggest that we tend to overweight our own opinions and experiences against statistical evidence.