The J.M. Smucker Company continues its aggressive growth strategy, but food prices and competition in general provide a number of headwinds to face. The company’s products include jellys, jams, peanut butter, coffee, sandwich products, ice cream toppings, baking products, oil, juices,

-Seven Year Average Revenue Growth Rate: 15%

-Seven Year Average EPS Growth Rate: 8.9%

-Seven Year Average Dividend Growth Rate: 9.4%

-Current Dividend Yield: 2.45%

-Balance Sheet Strength: Moderately Strong

The company draws its revenue mostly from North America, but has international ambitions as well. The company focuses primarily on having the No. 1 brand in any given category.

Coffee

For coffee brands, Smuckers has gone on a buying spree. They acquired the large Folgers brand of coffee from Procter and Gamble, and they also sell Dunkin Donuts coffee for retail markets. They now sell Millstone, Cafe Bustelo and Pilon coffee, with the last two being popular among Hispanic demographics, statistically speaking.

K-Cups are becoming more popular, and Smuckers has offerings in this area, including from their Folgers Gourmet Selections brand. Smuckers does face strong coffee competition from several brands, with Starbucks and Green Mountain Coffee Roasters being the two most worth mentioning.

Coffee represents 42% of company sales, and also has the largest profit margins out of their business segments.

U.S. Consumer Foods

The company’s original flagship product is their line of Smuckers fruit spreads: jams, jellies, and preserves. They were smart to acquire the Jif peanut butter brand as well, and they also control or license other brands like Crisco, Pillsbury and Hungry Jack.

This segment accounts for 38% of total company sales.

International and “Natural” Foods

Some of the company’s largest brands compete internationally, and they also have brands dedicated to certain markets, like Canada. For “natural foods” in this category, they have Santa Cruz Organic and R.W. Krudsen Family. In fiscal year 2012, the company invested in Seamild, a leading provider of oats products throughout China.

This third segment accounts for the remaining 20% of the company’s sales.

Price to Free Cash Flow: 20.7

Price to Book: 1.8

Return on Equity: 8.8%

(Chart Source: DividendMonk.com)

Revenue grew by a huge 15% annual rate over this period. However, the number of shares more than doubled over this period.

Smuckers probably has stronger revenue growth than any company I cover besides master limited partnerships. Most large companies are working to keep shares static, or repurchase shares to accelerate EPS and dividend growth, but Smuckers is operating more like an MLP in that they have radically increased the number of shares in order to grow aggressively. The company has done so responsibly and profitably.

(Chart Source: DividendMonk.com)

EPS growth averaged 8.9% over this period, which is decent. The big increase in the chart is primarily due to the large Folgers acquisition, from when Smuckers bought the major Folgers coffee brand from Procter and Gamble.

The dividend grew approximately in line with EPS, at 9.4% per year on average. The dividend payout is currently moderate, at under 50%.

As far as share repurchases are concerned, Smuckers follows an interesting cycle. When they’re not making a major acquisition, they have repurchased shares rather aggressively. In fiscal year 2012, the company spent $214 million on dividends and $316 million on buybacks to reduce the share count. The shareholder yield this year was a respectable 5-6%.

But during acquisitions, Smuckers has aggressively used its stock as its currency to expand and grow. Sales, earnings, and dividends per share have all grown at a moderately good pace as the company has pursued an aggressive and profitable growth strategy.

Approximate historical dividend yield at beginning of each year:

The current yield is approximately in line with the historical yield over this period, although the payout ratio has modestly expanded from sub-40% to sub-50%.

Total debt/income is under 5, which is acceptable, and the interest coverage ratio is over 9. Overall, the balance sheet is fairly strong.

It’s remarkable that Smuckers has been able to grow so quickly by issuing shares, while also growing the value of each share at a considerable rate. The company, therefore, significantly beat the market over the last decade. The company does acquisitions better than almost any other company out there. The main emphasis by this company is to focus on establishing and maintaining #1 brands.

The company had a 5% volume decline in 2012, which is concerning, but was offset by acquisition growth.

Going forward with a two-stage dividend discount model can provide some insight. If the company grows the dividend by an annualized rate of 8% over the next ten years (which is mildly under their recent growth rate), and then 7% thereafter, and a discount rate of 10% is used, then we’re looking at a fair stock value of under $76. But if only a small change is assumed, and we assume 8% dividend growth occurs perpetually, then we’re looking at a fair value of over $105. On the other end, if we use 6% for the perpetual dividend growth rate after 10 years of 8% growth, then the fair value is under $70.

Based on this range, the current price of $86 appears reasonable. Working backward from a dividend discount model perspective, a value of $86 implies 10 years of 8% dividend growth followed by 7.5% dividend growth perpetually (among other similar combinations).

Overall, it appears that Smuckers is reasonably priced, but like many defensive names at the current time, there doesn’t seem to be any margin of safety. I’m a holder of the stock but not a buyer at this price.

Full Disclosure: As of this writing, I am long SJM.

-Seven Year Average Revenue Growth Rate: 15%

-Seven Year Average EPS Growth Rate: 8.9%

-Seven Year Average Dividend Growth Rate: 9.4%

-Current Dividend Yield: 2.45%

-Balance Sheet Strength: Moderately Strong

Overview

The J.M. Smucker Company (SJM, Financial) was founded in 1897, is headquartered in Ohio, and is still run by the Smuckers family.The company draws its revenue mostly from North America, but has international ambitions as well. The company focuses primarily on having the No. 1 brand in any given category.

Coffee

For coffee brands, Smuckers has gone on a buying spree. They acquired the large Folgers brand of coffee from Procter and Gamble, and they also sell Dunkin Donuts coffee for retail markets. They now sell Millstone, Cafe Bustelo and Pilon coffee, with the last two being popular among Hispanic demographics, statistically speaking.

K-Cups are becoming more popular, and Smuckers has offerings in this area, including from their Folgers Gourmet Selections brand. Smuckers does face strong coffee competition from several brands, with Starbucks and Green Mountain Coffee Roasters being the two most worth mentioning.

Coffee represents 42% of company sales, and also has the largest profit margins out of their business segments.

U.S. Consumer Foods

The company’s original flagship product is their line of Smuckers fruit spreads: jams, jellies, and preserves. They were smart to acquire the Jif peanut butter brand as well, and they also control or license other brands like Crisco, Pillsbury and Hungry Jack.

This segment accounts for 38% of total company sales.

International and “Natural” Foods

Some of the company’s largest brands compete internationally, and they also have brands dedicated to certain markets, like Canada. For “natural foods” in this category, they have Santa Cruz Organic and R.W. Krudsen Family. In fiscal year 2012, the company invested in Seamild, a leading provider of oats products throughout China.

This third segment accounts for the remaining 20% of the company’s sales.

Ratios

Price to Earnings: 21.1Price to Free Cash Flow: 20.7

Price to Book: 1.8

Return on Equity: 8.8%

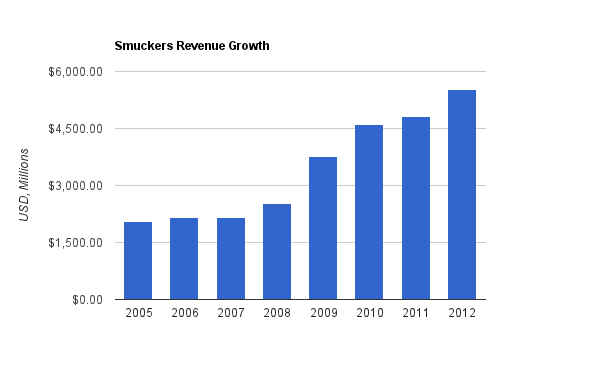

Revenue

(Chart Source: DividendMonk.com)

Revenue grew by a huge 15% annual rate over this period. However, the number of shares more than doubled over this period.

Smuckers probably has stronger revenue growth than any company I cover besides master limited partnerships. Most large companies are working to keep shares static, or repurchase shares to accelerate EPS and dividend growth, but Smuckers is operating more like an MLP in that they have radically increased the number of shares in order to grow aggressively. The company has done so responsibly and profitably.

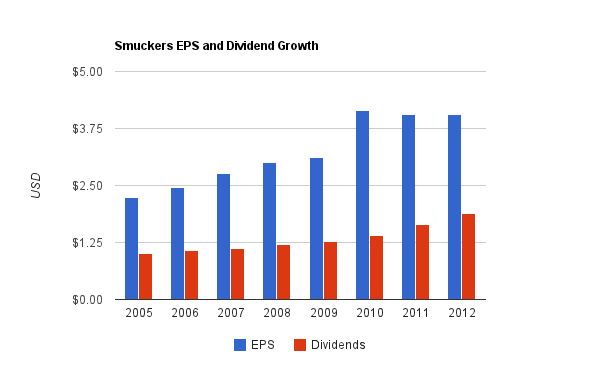

Earnings and Dividends

(Chart Source: DividendMonk.com)

EPS growth averaged 8.9% over this period, which is decent. The big increase in the chart is primarily due to the large Folgers acquisition, from when Smuckers bought the major Folgers coffee brand from Procter and Gamble.

The dividend grew approximately in line with EPS, at 9.4% per year on average. The dividend payout is currently moderate, at under 50%.

As far as share repurchases are concerned, Smuckers follows an interesting cycle. When they’re not making a major acquisition, they have repurchased shares rather aggressively. In fiscal year 2012, the company spent $214 million on dividends and $316 million on buybacks to reduce the share count. The shareholder yield this year was a respectable 5-6%.

But during acquisitions, Smuckers has aggressively used its stock as its currency to expand and grow. Sales, earnings, and dividends per share have all grown at a moderately good pace as the company has pursued an aggressive and profitable growth strategy.

Approximate historical dividend yield at beginning of each year:

| Year | Yield |

|---|---|

| Current | 2.45% |

| 2012 | 2.5% |

| 2011 | 2.5% |

| 2010 | 2.3% |

| 2009 | 2.9% |

| 2008 | 2.3% |

| 2007 | 2.3% |

| 2006 | 2.4% |

| 2005 | 2.1% |

| 2004 | 2.0% |

Balance Sheet

Total debt/equity for Smuckers is only around 40%, and the goodwill (much of which came from the Folgers purchase) only makes up around 60% of total equity, which is reasonable considering the company’s pursuit of acquisitions.Total debt/income is under 5, which is acceptable, and the interest coverage ratio is over 9. Overall, the balance sheet is fairly strong.

Investment Thesis

The primary growth strategy of Smuckers has been to focus on acquisitions, which they have done smartly. The most recent big acquisition was the hot beverage business part of Sara Lee for $420.6 million, with the prior large acquisition being Rowland Coffee Roasters in 2011 for $362.8 million.It’s remarkable that Smuckers has been able to grow so quickly by issuing shares, while also growing the value of each share at a considerable rate. The company, therefore, significantly beat the market over the last decade. The company does acquisitions better than almost any other company out there. The main emphasis by this company is to focus on establishing and maintaining #1 brands.

Risks

Like any company, SJM has risks. Being a food company, they are a defensive stock, but they always face risk in two main forms: commodity costs and cheaper private label competition. In addition, in contrast to many large American companies, Smuckers has most of its sales and operations in North America, meaning it is geographically concentrated.The company had a 5% volume decline in 2012, which is concerning, but was offset by acquisition growth.

Conclusion and Valuation

Due to the moderately low yield and substantial dividend growth rate, the Dividend Discount Model (DDM) can only provide a wide range of reasonable values here rather than an extremely targeted fair value. Standard discounted cash flow is hampered a bit by the tendency of Smuckers to use its shares as currency for acquisitions, so sticking to a per-share valuation method is preferable in my view.Going forward with a two-stage dividend discount model can provide some insight. If the company grows the dividend by an annualized rate of 8% over the next ten years (which is mildly under their recent growth rate), and then 7% thereafter, and a discount rate of 10% is used, then we’re looking at a fair stock value of under $76. But if only a small change is assumed, and we assume 8% dividend growth occurs perpetually, then we’re looking at a fair value of over $105. On the other end, if we use 6% for the perpetual dividend growth rate after 10 years of 8% growth, then the fair value is under $70.

Based on this range, the current price of $86 appears reasonable. Working backward from a dividend discount model perspective, a value of $86 implies 10 years of 8% dividend growth followed by 7.5% dividend growth perpetually (among other similar combinations).

Overall, it appears that Smuckers is reasonably priced, but like many defensive names at the current time, there doesn’t seem to be any margin of safety. I’m a holder of the stock but not a buyer at this price.

Full Disclosure: As of this writing, I am long SJM.