I bought CommScope Holding Co. (COMM, Financial) a few years ago, when interest rates were low and the stock looked cheap. It has gotten a lot cheaper since then, and the interest rate environment has changed drastically. Thus, in this discussion, I will take another look at the company and analyze its potential. These are my own notes, so potential investors should do their own due diligence to ensure it is suitable for them before taking the plunge as it is a high-risk play.

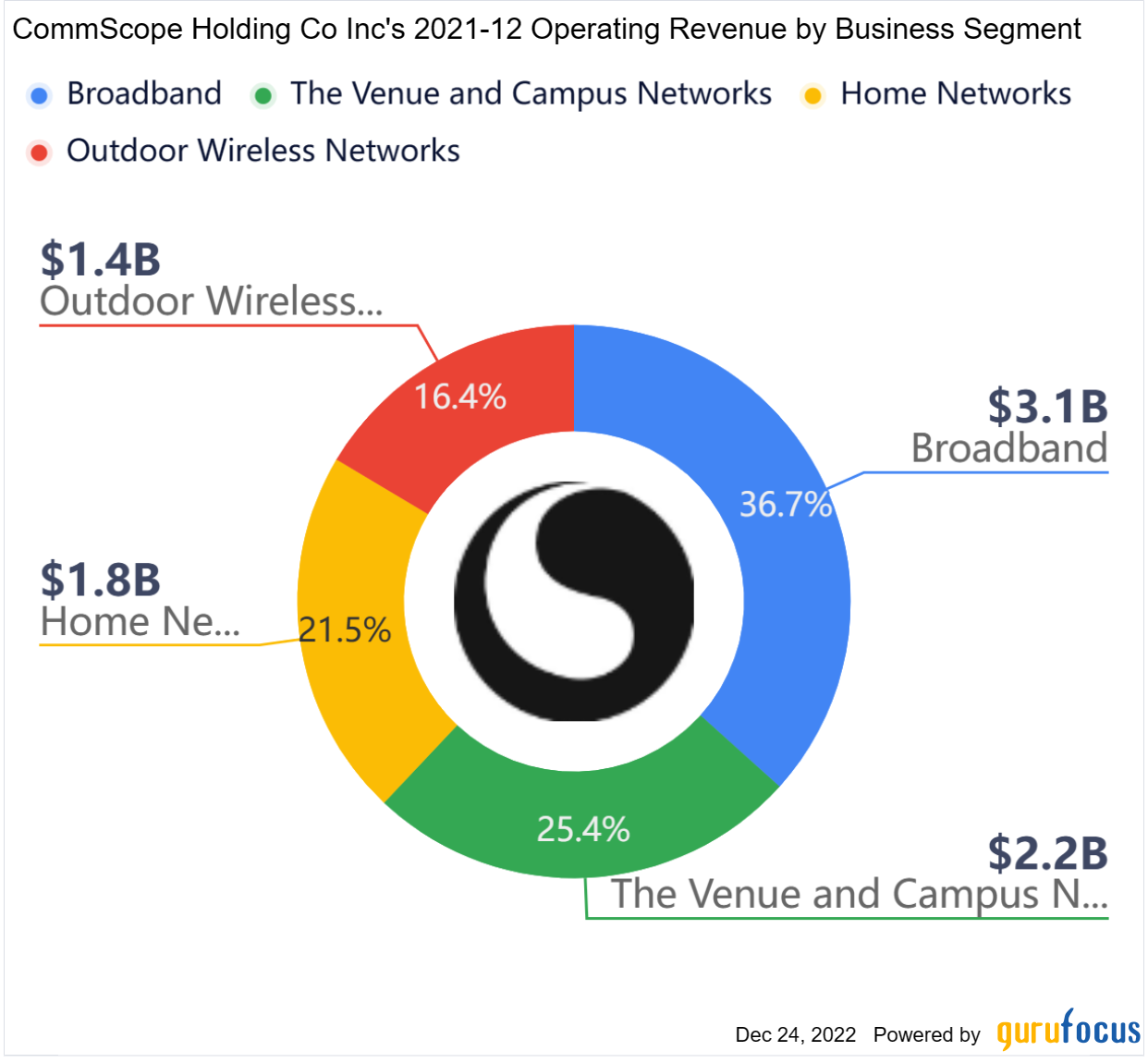

Headquartered in Hickory, North Carolina, the company develops, manufactures and supplies equipment and infrastructure for networking. The company operates through four segments: Broadband Networks (Broadband), Outdoor Wireless Networks (OWN), Venue and Campus Networks (VCN) and Home Networks (Home). The company is best known for its TV set-top boxes marketed under the Arris brand, but it is also a leading provider of antennas, cabling, connectors and connectivity equipment for enterprise and telecom service providers.

An original pioneer in the cable TV infrastructure business, CommScope as it is known today was put together through a series of acquisitions. The initial business was founded in 1975 within Superior Continent Cable Co.

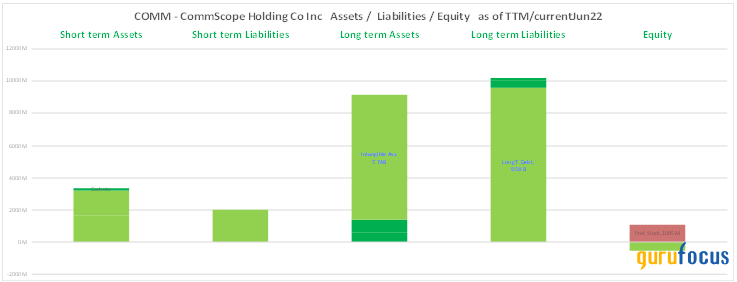

The company is structured like a publicly traded leveraged buyout fund, meaning a small amount of equity supports a large amount of debt. The debt-to-equity ratio is a shocking 17.64. Further, CommScope has a market cap of around $1.5 billion and a total enterprise value of the just over $12 billion.

Debt

Following the maturity schedule from the company's recent 10-Q, the debt appears to be fairly spread out. As a result, the company should be able to refinance the debt when it comes due, albeit at a higher rate. The earliest tranche of debt is due in June 2025. CommScope's debt leverage is very high at 7.8 as of Sept. 30, but management says it remains on track to reduce net leverage within the range of 6.8 times to 7.2 times by year end.

| $ Millions | September 30,2022 |

| 7.125% senior notes due July 2028 | 700.0 |

| 5.00% senior notes due March 2027 | 750.0 |

| 8.25% senior notes due March 2027 | 1,000.0 |

| 6.00% senior notes due June 2025 | 1,300.0 |

| 4.75% senior secured notes due September 2029 | 1,250.0 |

| 6.00% senior secured notes due March 2026 | 1,500.0 |

| Senior secured term loan due April 2026 | 3,104.0 |

| Senior secured revolving credit facility | 105.0 |

| Total principal amount of debt | 9,709.0 |

| Less: Original issue discount, net of amortization | (17.0) |

| Less: Debt issuance costs, net of amortization | (83.2) |

| Less: Current portion | (32.0) |

| Total long-term debt | 9,576.8 |

Debt peaked in 2019 following the acquisition of Arris, but the company is now getting it down. The following chart shows the total debt per share. Debt is down from over $53 per share in 2019 to around $47 per share now, a reduction of over 12% in three years. Thus, progress is being made.

However, the recent spike in interest rates triggered by Federal Reserve tightening has increased the risk to the company substantially. This, in turn, has hammered the stock price, which is now approaching the pandemic lows of March 2020.

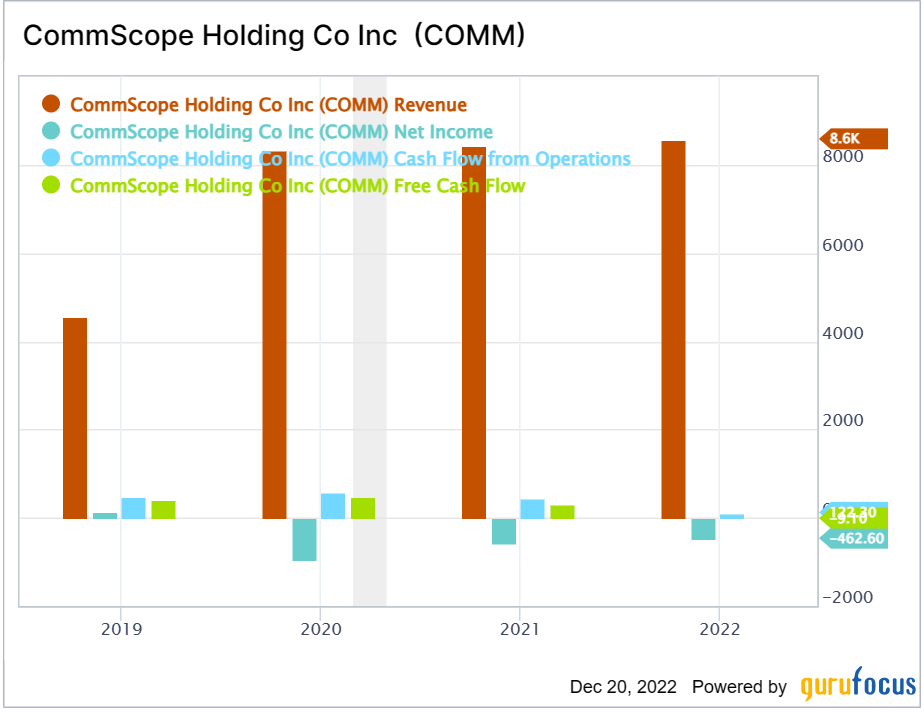

On the plus side, business is robust with revenue growing by over 20% since 2018 (which includes the Arris acqusition). In November, the company reported strong top-line growth for the third quarter, with core net sales of $1.99 billion growing 18% from the prior year, adjusted Ebitda of $353 million and a backlog of $3.6 billion, representing approximately six months of sales. (The above results excluded the Home Network segment, which CommScope intends to separate or sell when market valuations recover.)

The cash flow tends to swing widely from year to year as the company has large working capital needs, but CommScope is core free cash flow positive after adjusting for changes in working capital.

Valuation

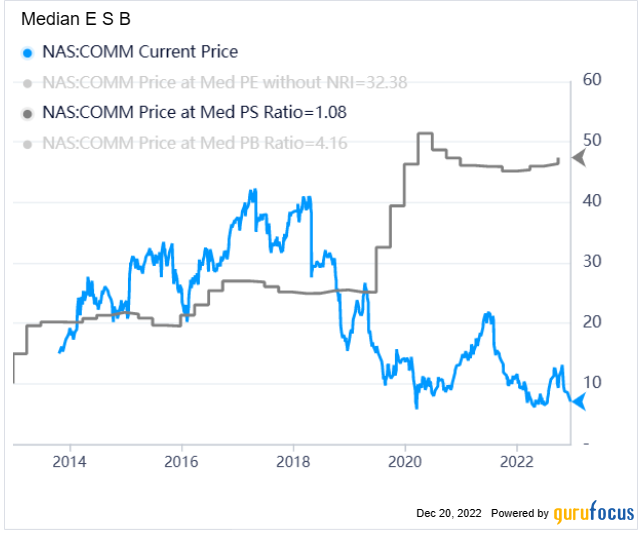

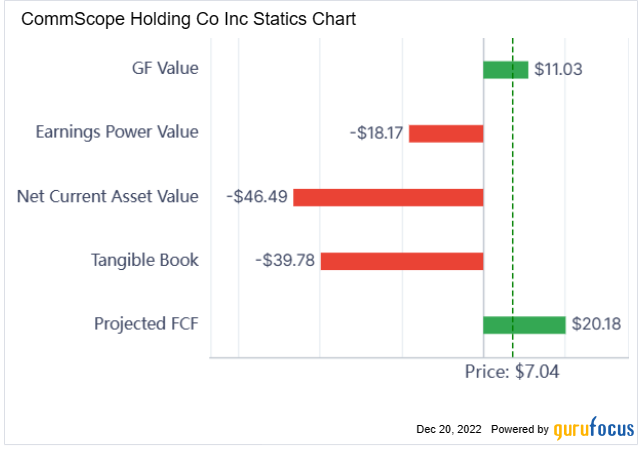

CommScope does not have GAAP earnings, so it is not possible to calculate the price-earnings ratio. However, the extreme undervaluation can be seen in the median price-sales ratio. The price-sales ratio's justified valuation is close to $50 vs. the current stock price of $7. While this looks optimistic, a share price of $30, if things go reasonably well, in a few years is very possible.

Another hint of undervaluation is provided by GuruFocus' proprietary projected FCF Value with an indicated value of about $20.

GuruFocus has devised a metric called the Projected FCF value to deal with situations where free cash flow or earnings are erratic. Essentially, the metric takes 80% of the book value and adds it to the present value of free cash flow averaged over six years.

Either way, CommScope looks highly undervalued and could possibly go up multiple times. The elephant in the room is, of course, debt, which could overwhelm the company if the recession turns out to be severe or prolonged, which I do not expect.

Another positive for investors is the robust insider buying (and lack of insider selling) of the stock. This shows insiders have confidence in the company and are putting their money where their mouth is.

Conclusion

CommScope is a high-risk, high-return play that could be a binary bet. Either new investors will end up making multiples of their investment in a few years provided the economy cooperates, or the company will be insolvent if the recession is worse than expected due to the large debt load. In the latter case, equity holders could be wiped out.

Overall, my conclusion is the upside is higher than the downside, as my macroeconomic view is the coming recession will be relatively short and shallow. As a result, I have added to my position.