A balanced portfolio of index funds is one of the smartest and easiest ways for most people to invest and build wealth. It takes a few hours per year to manage, which means you should get a good compounded rate of return on your money while you’re out living your life. I consider it the other smart long-term investment strategy besides value investing, and one that’s suitable for a wider range of people.

This article is going to provide a comprehensive overview on why and how to invest in index funds. It’s about how to invest in index funds purely, or how to combine them with individual stocks. We’re talking 4,500 words here, so you might want to bookmark this page. Alternatively, you can use the following links to jump directly to the sections that you want know about.

An Index Fund is a specific type of Mutual Fund, so it’s best to start there.

An Index Fund is a specific type of Mutual Fund, so it’s best to start there.

Shares of stock represent small portions of the ownership of a company. With a mutual fund, a fund manager collects the money from a bunch of investors together and buys shares of many companies with the common pool of money. So when you own a piece of a mutual fund, you own a piece of a big pool of stocks and/or other investments.

In an actively managed mutual fund, the fund manager is trying to meet a certain goal, such as wealth preservation or to try to beat the market.

In a passive mutual fund, called an index fund, the collective wealth of the investors is passively managed by the fund manager to match a certain index, such as the S&P 500. In other words, the index fund doesn’t try to beat the market; it is the market. Rather than trying to select individual stocks, the fund manager invests in all stocks that meet certain criteria.

There are several types of index funds. The most well-known ones follow the S&P 500, which is a set of 500 of the largest and most profitable corporations in the United States. But there are index funds that follow Bond indexes, funds that follow international markets, funds that follow the stocks of a specific country, funds that follow REITs, funds that follow specific sectors (such as Technology, or Healthcare), and all sorts of other funds.

The primary thing index funds have in common is that the fund manager isn’t trying to do anything other than match an index. He’s buying stock from most or all of the companies that meet the criteria of that particular index.

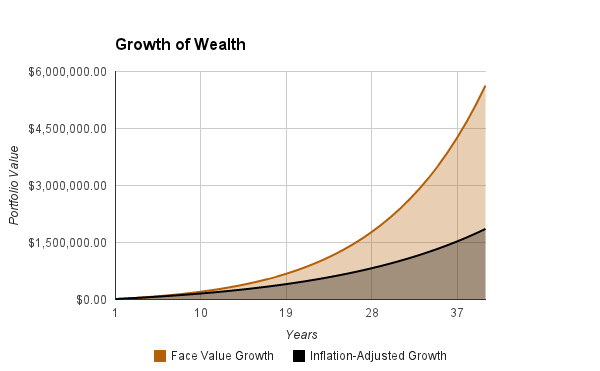

To provide a tangible example, if you put $1,000 per month away into an index fund that grows at an average rate of 9% per year with 3% average inflation, then you’ll have approximately $850,000 in 20 years, and this value adjusted for inflation would be $480,000. At the 40-year mark, these figures rise to $5.6 million in value, and $1.8 million in inflation-adjusted value. You could double or triple these intermediate and end-values by doubling or tripling your monthly investment.

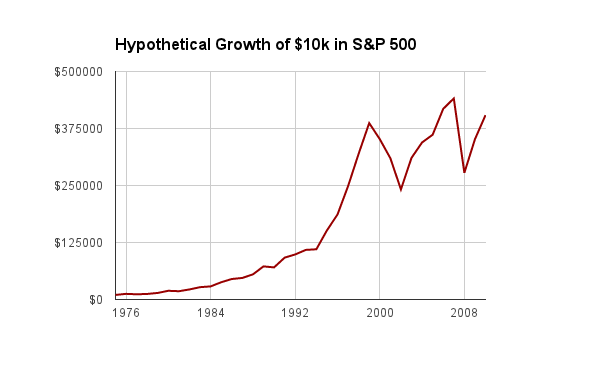

More realistically, the returns are going to be somewhat volatile. Here was the actual growth of a hypothetical $10,000 invested between 1975 and 2010:

Notice that the growth spiked at the turn of the century during the dot com bubble, and then moved flat and volatile over the next decade. This was because equities became overvalued during that period, and then had 10 years worth of reductions in stock valuations followed by the financial crisis.

Drawing a trend line over the long-term outcome takes some of the weirdness away. It ends up looking like the first chart, actually:

Low Fees

The biggest advantage of index funds is their low fees. Actively managed funds have much higher fees, and after fees, most of them provide lower returns than the market. By keeping fees low and merely trying to match the market rather than beat it, index funds statistically beat out actively managed mutual funds.

(The most successful investor in the world, Warren Buffett, recommends Index Funds to most investors for this reason.)

The Efficient Market Hypothesis suggests that all publicly-known information is already factored into stock prices, and that therefore nobody can deliberately beat the market. (It’s luck if they do, according to the hypothesis). To what degree you accept that hypothesis is up to you, but be aware of it.

No Investing Experience Needed

Index funds require no stock picking and little business knowledge, and therefore are useful for everyone that has money to save and invest.

Save Your Time

Out of all investing methods, index funds require the least of your valuable time. Depending on exactly what sort of index funds you pick, when it comes to basic portfolio maintenance, you’ll spend anywhere from a few minutes per year, to a few hours per year, to perhaps a couple of hours per month, tops. This is the closet to set-it-and-forget-it investing you can have.

You Forfeit Shareholder Voting Rights

Shareholders of stock get to voice their opinion on various company matters, ranging from approving or disapproving executive compensation, to voting on specific corporate matters such as whether a company should have a nondiscrimination policy that protects gay employees or whether a company should more easily disclose its political contributions or not. Those were some examples of questions that were brought to a shareholder vote for one of my holdings. Most shareholder votes are nonbinding, but their ultimate power is the ability to elect or not elect directors to the board of the company.

If you invest only in index funds, then you give up your shareholder voting rights to the index fund manager, since they own the equities rather than you. Most fund managers don’t vote quite how you’d likely want to vote if you owned the shares because they represent the interests of millions of shareholders and therefore abstain from many types of votes.

No Investing Experience Needed

This was listed in the advantages section, but it’s a double-edged sword. Investing in index funds means you never have to look at a corporate report, never have to learn Discounted Cash Flow Analysis, never have to keep up on what corporations are doing.

Gaining some knowledge on how businesses work down to the shareholder level can give you knowledge of politics and economics, can help you dominate an interview, gives you some financial knowledge for your own trials of entrepreneurship, and generally leads to financial well-roundedness.

You Abstain from Outperformance

An index fund will beat most actively managed mutual funds due to the huge difference in fees. Most people, including professionals, who try to pick stocks fail to beat the market.

Some of them don’t. Instead, some of them massively outperform the market.

The problem is that it’s next to impossible to know ahead of time which fund manager will outperform the market, and it’s difficult to predict your own future stock-picking ability if you go that route.

An index fund will essentially match the market. If you’re a value investor that believes that you can beat the market by at least a percentage or two per year (which can add up to hundreds of thousands of dollars over the long run), then you might have a better shot with appropriately valued individual stocks.

MPT argues that the only free lunch is diversification. For any desired rate of return, you can reduce the risk by diversifying. For any level of risk, you can increase the rate of return by diversifying.

When it comes to index funds, this primarily means asset allocation between stocks and bonds, but can also include cash, REITs, MLPs, etc. And within the stock segment, it means diversification between equities in your own country and equities from other countries. For example, if you’re based in the U.S., and your portfolio consists of a U.S. stock index fund, an international stock index fund, and a U.S. bond fund, along with sufficient cash and some real estate, then you’d be considered rather diversified.

This diversification reduces your volatility at the expense of reducing your overall rate of return, at least over the long term. To passively rebalance your portfolio, you simply pick a target balance and stick to it.

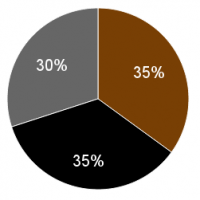

For example, if you decide that your percentage of bonds will equal your age, and that your equities will be split evenly between U.S. stock and foreign stocks, then a 30 year old person would have an index portfolio consisting of three funds: 35% in U.S. equities, 35% in foreign equities, and 30% in bonds. This plan makes your portfolio become less volatile as you age, so that you maximize your rate of return when you’re young, and yet you don’t experience a large decrease when you’re older.

In this scenario, you’d automatically buy stock when stocks are cheap, and sell stocks when stocks are high, which is ideal.

To simplify the scenario, let’s just say your portfolio consists of stocks and bonds, in a 70%/30% balance. If this year, stocks rise by a huge amount, then your portfolio might shift towards 80%/20% in favor of stocks. So, to maintain the balance, you’d use your investment money to buy more of the bond funds to balance that out. And in the event that that’s not enough, you’d sell some of your stock to buy bounds, and regain the 70%/30% target.

If next year, stocks fall by a large amount, then your portfolio might shift towards 60%/40% in favor of stocks. So, to maintain the balance, you’d use your investment money to buy more of the stock funds to balance that out. If that’s not enough, then you’d sell some of your bonds to buy stock, and regain the 70%/30% target.

This doesn’t entail market timing, because you’re not making any predictions about the future. You’re just maintaining the 70%/30% stock/bond allocation whenever it becomes unbalanced by a few percentage points. The same is true for a three-fund portfolio that consists of domestic equities, foreign equities, and bonds; you’d simply direct capital towards the funds that are below your target balance due to their recent underperformance, and/or draw funds away from the funds that are over-represented in the portfolio due to their recent outperformance.

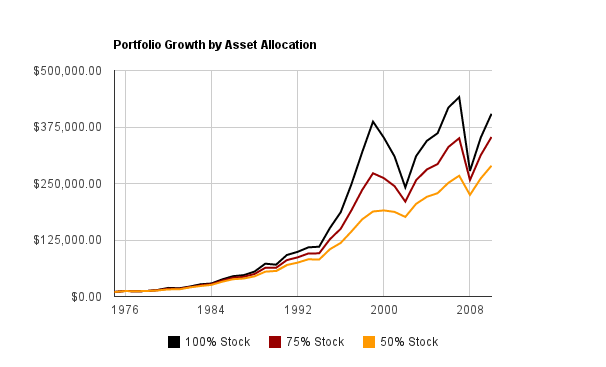

To give an idea of how different types of balances would do, the following chart shows the historical performance of stock/bond allocations between 1975 and 2010. For simplicity, the “stock” section is the S&P 500, when in reality, you’d likely want to split it between U.S. equities and foreign equities. Nonetheless, it presents a long real scenario of the kinds of returns you would have had with different balances of equities and bonds.

The following chart shows the growth of a $10,000 investment in 1975 in three different scenarios: 100% stock, 75%/25% stock/bond, and 50%/50% stock/bond:

As can be seen, the volatility and total returns increased as the equity exposure increased.

However, these differences are somewhat reduced in a more realistic scenario where new money is invested each year, which would be typical during a working career. In the next chart, each portfolio starts with $10,000 in 1975, but then new money is added each year. More money is added each year to represent a combination of inflation and increased earnings power, so $2k is put in during the first year, then $4k the next year, then $6k the next year, then $8k the year after that, and so on.

In this scenario, there are two main things to notice. First, adding more money over time resulted in a much larger portfolio value over time. Second, it made it so that even the difference between 100% stock and 50%/50% stock/bond was minimal over the long term. The latter was less volatile but provided almost the same rate of return.

The research for these returns originally appears in a bit more detail in the Dividend Toolkit.

The takeaway here is to maintain a balanced portfolio. Your precise allocation depends on your goals, but mixing stocks and bonds, and rebalancing during market movements, reduces your volatility and keeps your overall rate of return decent. This type of rebalancing takes literally a couple of hours per year. Whenever you add more money to your portfolio (such as once per month perhaps), simply add it to the funds that are below your target allocation to balance them out. If the segments of your portfolio are perhaps 5% or more out of balance despite your additions of new money, then consider selling a portion of the over-represented fund to buy more of the under-represented fund to achieve balance.

Simple.

Likewise, during certain periods such as the market bottom in 2009, it was clear to many value investors that the market was very undervalued.

In these circumstances, wouldn’t it be optimal to change the balance accordingly? During the top of the dotcom bubble, wouldn’t it be rational to reduce stock exposure to well under the normal target? And during deep market bottoms, wouldn’t it be rational to increase stock exposure to well over the normal target?

It depends on what your goals are.

If you’d like to be a bit more active with your portfolio, then the Shiller P/E is a good tool to use. The Shiller PE, put forth by Robert Shiller, Yale Economist, is a calculation of the current market valuation. It divides the price of the market by the inflation-adjusted average of the last ten years of earnings to provide a smoothed-out representation of what the current valuation of the market is compared to what it historically has been.

The chart shows that, over a century-long period, the current market valuation is inversely proportional with the expected annualized returns over the next 20 years. In other words, the higher the current market valuation is (as calculated by the Shiller P/E ratio), the less likely it is you’ll get good returns over the next 20 years:

Image Source

The chart ends in 2005 (20 years after the last mark of 1985), but the accuracy has continued up until the present day. The decade from 2000-2010 was absolutely terrible for equities because the market was ridiculously overvalued in the late 1990”²s and early 2000”²s.

Given the rather well-evidenced (and inherently logical) premise that highly valued markets offer statistically lower returns, there is a semi-popular investing method that takes this into account.

With this method, an indexed portfolio is rebalanced actively. Rather than sticking to a static stock/bond allocation, such as 70%/30%, the ratio is adjusted based on the Shiller P/E of the market. The higher the Shiller P/E, the lower the stock allocation. And the lower the Shiller P/E, the higher the stock allocation.

The precise method of active rebalancing could be up to you, but here’s an example. Again, I used a simple two-part stock/bond portfolio to explain the point rather than the more realistic US/Foreign/Bond portfolio that would be better to go with.

-When the Shiller P/E of the market is 18, the portfolio shall be 80% stock and 20% bonds.

-For each point that the Shiller P/E rises, the stock percentage shall be decreased by 2%.

-For each point that the Shiller P/E falls, the stock percentage shall be increased by 2%.

So, if the Shiller P/E is 21, the portfolio shall be 76% stock and 24% bonds. If the Shiller P/E is 15, the portfolio shall be 86% stock and 14% bonds. And so on.

This is what the results would have been between 1975 and 2010, compared with the passive portfolios, where “Active” is this actively rebalanced portfolio:

The returns were slightly better, and the volatility was fairly modest. “Active” is probably even an overstatement, because this accounts for a rebalancing only once per year, so it’s about 10 minutes of work per year.

Whether this is a method to go with isn’t conclusive, though.

The overall returns are better, but they’re not that much better.

Given that a) most people won’t stick to the plan and b) the returns aren’t dramatically improved, there’s not a strong reason for everyone to follow that method. Passive rebalancing is perfectly fine. But if you enjoy investing and want to reduce or increase your equity exposure based on the market valuation, it can be a worthwhile approach that likely leads to improved returns and reduced volatility if it’s done with discipline. Personally I wouldn’t recommend it for most people that I encounter, but the information is around for those that want to pursue the method of taking market valuations into account for determining the balance of portfolio assets.

There are a few main ways to invest via Vanguard funds.

Indexed Mutual Funds

These indexes are structured as mutual funds. You can open open an account with them, and the minimum amount to invest depends on the specific fund but is typically several thousand dollars. Here are some of the options:

Total Stock Market Index Fund Investor Shares

This fund invests small, medium, and large publicly traded American companies, and has an expense ratio of only 0.18%.

High Dividend Yield Investor Shares

This fund invests in over 400 companies that pay medium and high dividend yields. The yield is over 3% and the expense ratio is 0.25%.

Total Bond Market Index Fund Admiral Shares

Here’s a good bond fund, diversified across over 5,000 bonds with a 0.10% expense ratio.

Total International Stock Index Fund Investor Shares

For international exposure, this is a good choice. The fund includes over 6,000 companies from around the world, but excludes U.S. companies so that you can pair this with a U.S. index without overlapping. The expense ratio is 0.22%.

If you hold simply a U.S. stock fund, and international stock fund, and a bond fund, your portfolio is pretty diversified. If you live in Canada or the UK or another country, you may want to modify that with greater emphasis on your home country, but the basics are the same.

Funds of Funds

An even simpler method is to invest in a fund of funds. Let Vanguard rebalance your own funds for you. In these structures, Vanguard groups together some of the funds from the previous category into a fund of funds that they keep at a specific balance.

LifeStrategy Growth Fund

This fund is split between the Total Stock Market fund (56%), the Total International Stock Market fund (24%), and the Total Bond Market fund (20%). The expense ratio is 0.17%, and the primary goal here is to grow the wealth with manageable volatility.

LifeStrategy Income Fund

This fund inverses the balance compared to the previous fund, consisting of bonds (80%), U.S. stocks (14%) and international stocks (6%). It’s meant for retirement to keep volatility and risk lower, and the expense ratio is 0.13%. There are two other options that rest between these two funds in terms of stock/bond ratios.

Target Retirement 2040 Fund

This fund is a bit different than the others, because the fund will shift towards bonds over time. As of this writing, it currently consists of 63% U.S. stock, 27% international stock, and 10% bonds. Over time, the bond ratio will grow larger and larger, to reduce volatility as you near retirement. Vanguard offers these funds in five-year increments, so you pick the fund that corresponds to your expected retirement year.

With these funds of funds, you’re sufficiently diversified if you invest in them. Apart from holding property and cash, your job as an investor here is just to shovel as much money into these funds as possible and let Vanguard do the rest. It takes no management from you at all except to check your balances once in a while and keep up with paperwork and taxes (a few hours per year at most), so you can focus your efforts on increasing your income, living life, etc.

Indexed ETFs

These funds are similar to the first group of mutual funds, but they’re wrapped in a structure that is traded on a stock exchange. This is why they are called Exchange Traded Funds (ETFs). You don’t need a Vanguard account for these; you can buy them through any brokerage account just like you would buy any stock.

Total Stock Market ETF (VTI)

Vanguard’s ETF invests in over 3,000 U.S. companies and has an expense ratio of 0.06%.

Total Bond Market ETF (BND)

Vanguard’s Bond Market ETF with an expense ratio of 0.10%.

Total International Stock ETF (VXUS)

Vanguard’s International Stock ETF with a 0.18% expense ratio.

These are the same as their equivalent mutual funds. They’re more flexible, because you can buy and sell them through any broker. There is not currently a fund-of-funds ETF option through Vanguard.

So, to be clear, I think that for 90% of the population, going with a passive and purely indexed approach is the most optimal investing method.

If you’re like me, and for one reason or another you want to own individual stocks as well (because you want to retain your shareholder voting rights rather than wasting them, or you think you can beat the market with a smart investing approach, or you want higher and more consistent dividend income, or another reason), then there are some seamless ways to combine indexes and individual stocks.

The easiest option is to split investments between different accounts. For example, if you have a 401(k), then you can fill that with a few index funds. Then if you have an IRA or a taxable account on the side, you could look into building a portfolio of stocks that pay good dividends, or growth stocks you know well, etc. If the bulk of your wealth is diversified and indexed, then trying your hand at stock picking can keep your risks low.

If you combine things together, then you just have to keep track of your overall diversification. For example, if you have a regular brokerage account filled with indexed ETFs and some individual stocks, then make sure you keep track of what you’re overall diversification is.

For example, let’s say you have $50,000 in a bond ETF, $50,000 in an international stock ETF, and $100,000 in a U.S. stock ETF, and you also own $50,000 worth of individual U.S. stocks split between 10 holdings. In this scenario, the indexed portion of your portfolio is split between 50% U.S. stocks, 25% international stocks, and 25% bonds. The overall split including the individual stocks is 60% U.S. stocks, 20% international stocks, and 20% bonds.

Whatever target balance you’re aiming for, you have to make sure to include your individual stock holdings.

Another way to use index funds is to use some of the more targeted ones to give your portfolio exposure to certain markets. For example, if you own a portfolio mainly consisting of dividend stocks, you may be a bit light in certain industries, like technology. Or you may feel that your overall exposure is a bit too focused on large caps, or not globally diversified to your liking. If that’s the case, then you can hold a technology index fund like the Vanguard Information Technology ETF (VGT), or an index that focuses on small caps, or an international index fund. Or, let’s say you don’t feel comfortable picking stocks in a certain industry, like health care for example. That’s where an index that focuses on the health care industry can give you exposure to that industry and complement the rest of your portfolio.

So if you’d like some further reading on index funds, there are a few books that are good choices.

Millionaire Teacher

This is the #1 personal finance and investing book I’d recommend to people. It’s a good update on the established concepts. The author, Andrew Hallam, is an English teacher that became a millionaire in his 30”²s through frugality and index investing. Andrew is personable, so this book is concise, flowing, and quick to read, yet well-researched and thorough.

The Little Book of Common Sense Investing

Written By John Bogle, founder and retired CEO of Vanguard, this book is another concise and good read about index funds.

A Random Walk Down Wall Street

Burton Malkiel looks through various investment strategies and shows that they will underperform a passive investing approach. There have been several editions, and this is one of the original books about indexing, since it even predates index funds.

It’s the investing approach that takes the least amount of time, and although there are some drawbacks, there are plenty of advantages. In the simplest sense, it involves managing a portfolio that looks something like this:

In a more complicated scenario, it means keeping track of a few accounts which may include pure indexes, or indexes combined with individual stocks. If you own individual stocks, then index ETFs can still be quite useful to own assets in certain industries or to balance out your portfolio.

This article is going to provide a comprehensive overview on why and how to invest in index funds. It’s about how to invest in index funds purely, or how to combine them with individual stocks. We’re talking 4,500 words here, so you might want to bookmark this page. Alternatively, you can use the following links to jump directly to the sections that you want know about.

What is an Index Fund?

An Index Fund is a specific type of Mutual Fund, so it’s best to start there.Shares of stock represent small portions of the ownership of a company. With a mutual fund, a fund manager collects the money from a bunch of investors together and buys shares of many companies with the common pool of money. So when you own a piece of a mutual fund, you own a piece of a big pool of stocks and/or other investments.

In an actively managed mutual fund, the fund manager is trying to meet a certain goal, such as wealth preservation or to try to beat the market.

In a passive mutual fund, called an index fund, the collective wealth of the investors is passively managed by the fund manager to match a certain index, such as the S&P 500. In other words, the index fund doesn’t try to beat the market; it is the market. Rather than trying to select individual stocks, the fund manager invests in all stocks that meet certain criteria.

There are several types of index funds. The most well-known ones follow the S&P 500, which is a set of 500 of the largest and most profitable corporations in the United States. But there are index funds that follow Bond indexes, funds that follow international markets, funds that follow the stocks of a specific country, funds that follow REITs, funds that follow specific sectors (such as Technology, or Healthcare), and all sorts of other funds.

The primary thing index funds have in common is that the fund manager isn’t trying to do anything other than match an index. He’s buying stock from most or all of the companies that meet the criteria of that particular index.

The Advantages of Index Funds

Depending how far back we go in history to use as the reference, the average long-term rate of return of the S&P 500 is around 9% per year. After inflation, it’s approximately a 6% real rate of return of purchasing power.To provide a tangible example, if you put $1,000 per month away into an index fund that grows at an average rate of 9% per year with 3% average inflation, then you’ll have approximately $850,000 in 20 years, and this value adjusted for inflation would be $480,000. At the 40-year mark, these figures rise to $5.6 million in value, and $1.8 million in inflation-adjusted value. You could double or triple these intermediate and end-values by doubling or tripling your monthly investment.

More realistically, the returns are going to be somewhat volatile. Here was the actual growth of a hypothetical $10,000 invested between 1975 and 2010:

Notice that the growth spiked at the turn of the century during the dot com bubble, and then moved flat and volatile over the next decade. This was because equities became overvalued during that period, and then had 10 years worth of reductions in stock valuations followed by the financial crisis.

Drawing a trend line over the long-term outcome takes some of the weirdness away. It ends up looking like the first chart, actually:

Low Fees

The biggest advantage of index funds is their low fees. Actively managed funds have much higher fees, and after fees, most of them provide lower returns than the market. By keeping fees low and merely trying to match the market rather than beat it, index funds statistically beat out actively managed mutual funds.

(The most successful investor in the world, Warren Buffett, recommends Index Funds to most investors for this reason.)

The Efficient Market Hypothesis suggests that all publicly-known information is already factored into stock prices, and that therefore nobody can deliberately beat the market. (It’s luck if they do, according to the hypothesis). To what degree you accept that hypothesis is up to you, but be aware of it.

No Investing Experience Needed

Index funds require no stock picking and little business knowledge, and therefore are useful for everyone that has money to save and invest.

Save Your Time

Out of all investing methods, index funds require the least of your valuable time. Depending on exactly what sort of index funds you pick, when it comes to basic portfolio maintenance, you’ll spend anywhere from a few minutes per year, to a few hours per year, to perhaps a couple of hours per month, tops. This is the closet to set-it-and-forget-it investing you can have.

The Disadvantages of Index Funds

Although there are many advantages of index funds, there are a few drawbacks as well.You Forfeit Shareholder Voting Rights

Shareholders of stock get to voice their opinion on various company matters, ranging from approving or disapproving executive compensation, to voting on specific corporate matters such as whether a company should have a nondiscrimination policy that protects gay employees or whether a company should more easily disclose its political contributions or not. Those were some examples of questions that were brought to a shareholder vote for one of my holdings. Most shareholder votes are nonbinding, but their ultimate power is the ability to elect or not elect directors to the board of the company.

If you invest only in index funds, then you give up your shareholder voting rights to the index fund manager, since they own the equities rather than you. Most fund managers don’t vote quite how you’d likely want to vote if you owned the shares because they represent the interests of millions of shareholders and therefore abstain from many types of votes.

No Investing Experience Needed

This was listed in the advantages section, but it’s a double-edged sword. Investing in index funds means you never have to look at a corporate report, never have to learn Discounted Cash Flow Analysis, never have to keep up on what corporations are doing.

Gaining some knowledge on how businesses work down to the shareholder level can give you knowledge of politics and economics, can help you dominate an interview, gives you some financial knowledge for your own trials of entrepreneurship, and generally leads to financial well-roundedness.

You Abstain from Outperformance

An index fund will beat most actively managed mutual funds due to the huge difference in fees. Most people, including professionals, who try to pick stocks fail to beat the market.

Some of them don’t. Instead, some of them massively outperform the market.

The problem is that it’s next to impossible to know ahead of time which fund manager will outperform the market, and it’s difficult to predict your own future stock-picking ability if you go that route.

An index fund will essentially match the market. If you’re a value investor that believes that you can beat the market by at least a percentage or two per year (which can add up to hundreds of thousands of dollars over the long run), then you might have a better shot with appropriately valued individual stocks.

The Easy Way to Rebalance an Indexed Portfolio

The second chart in this article showcased how volatile even a broad market index can be. The proposed solution to this is Modern Portfolio Theory (MPT).MPT argues that the only free lunch is diversification. For any desired rate of return, you can reduce the risk by diversifying. For any level of risk, you can increase the rate of return by diversifying.

When it comes to index funds, this primarily means asset allocation between stocks and bonds, but can also include cash, REITs, MLPs, etc. And within the stock segment, it means diversification between equities in your own country and equities from other countries. For example, if you’re based in the U.S., and your portfolio consists of a U.S. stock index fund, an international stock index fund, and a U.S. bond fund, along with sufficient cash and some real estate, then you’d be considered rather diversified.

This diversification reduces your volatility at the expense of reducing your overall rate of return, at least over the long term. To passively rebalance your portfolio, you simply pick a target balance and stick to it.

For example, if you decide that your percentage of bonds will equal your age, and that your equities will be split evenly between U.S. stock and foreign stocks, then a 30 year old person would have an index portfolio consisting of three funds: 35% in U.S. equities, 35% in foreign equities, and 30% in bonds. This plan makes your portfolio become less volatile as you age, so that you maximize your rate of return when you’re young, and yet you don’t experience a large decrease when you’re older.

In this scenario, you’d automatically buy stock when stocks are cheap, and sell stocks when stocks are high, which is ideal.

To simplify the scenario, let’s just say your portfolio consists of stocks and bonds, in a 70%/30% balance. If this year, stocks rise by a huge amount, then your portfolio might shift towards 80%/20% in favor of stocks. So, to maintain the balance, you’d use your investment money to buy more of the bond funds to balance that out. And in the event that that’s not enough, you’d sell some of your stock to buy bounds, and regain the 70%/30% target.

If next year, stocks fall by a large amount, then your portfolio might shift towards 60%/40% in favor of stocks. So, to maintain the balance, you’d use your investment money to buy more of the stock funds to balance that out. If that’s not enough, then you’d sell some of your bonds to buy stock, and regain the 70%/30% target.

This doesn’t entail market timing, because you’re not making any predictions about the future. You’re just maintaining the 70%/30% stock/bond allocation whenever it becomes unbalanced by a few percentage points. The same is true for a three-fund portfolio that consists of domestic equities, foreign equities, and bonds; you’d simply direct capital towards the funds that are below your target balance due to their recent underperformance, and/or draw funds away from the funds that are over-represented in the portfolio due to their recent outperformance.

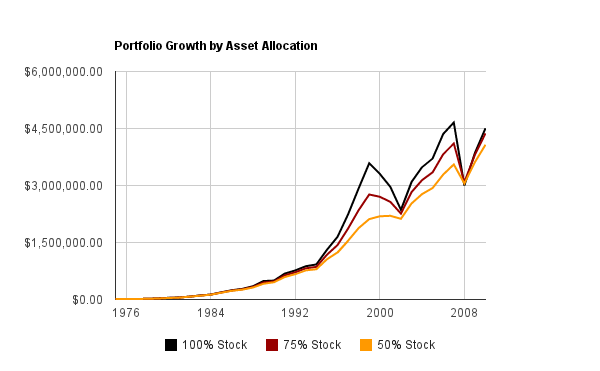

To give an idea of how different types of balances would do, the following chart shows the historical performance of stock/bond allocations between 1975 and 2010. For simplicity, the “stock” section is the S&P 500, when in reality, you’d likely want to split it between U.S. equities and foreign equities. Nonetheless, it presents a long real scenario of the kinds of returns you would have had with different balances of equities and bonds.

The following chart shows the growth of a $10,000 investment in 1975 in three different scenarios: 100% stock, 75%/25% stock/bond, and 50%/50% stock/bond:

As can be seen, the volatility and total returns increased as the equity exposure increased.

However, these differences are somewhat reduced in a more realistic scenario where new money is invested each year, which would be typical during a working career. In the next chart, each portfolio starts with $10,000 in 1975, but then new money is added each year. More money is added each year to represent a combination of inflation and increased earnings power, so $2k is put in during the first year, then $4k the next year, then $6k the next year, then $8k the year after that, and so on.

In this scenario, there are two main things to notice. First, adding more money over time resulted in a much larger portfolio value over time. Second, it made it so that even the difference between 100% stock and 50%/50% stock/bond was minimal over the long term. The latter was less volatile but provided almost the same rate of return.

The research for these returns originally appears in a bit more detail in the Dividend Toolkit.

The takeaway here is to maintain a balanced portfolio. Your precise allocation depends on your goals, but mixing stocks and bonds, and rebalancing during market movements, reduces your volatility and keeps your overall rate of return decent. This type of rebalancing takes literally a couple of hours per year. Whenever you add more money to your portfolio (such as once per month perhaps), simply add it to the funds that are below your target allocation to balance them out. If the segments of your portfolio are perhaps 5% or more out of balance despite your additions of new money, then consider selling a portion of the over-represented fund to buy more of the under-represented fund to achieve balance.

Simple.

The Optimal Way to Rebalance an Indexed Portfolio

It can be tempting to try to optimize these rebalancing efforts. For example, during the dotcom boom, it was clear to rational investors or economists such as Warren Buffett and Peter Shiller that the market was overvalued. It could be objectively proven with reasonable stock valuation methods including the Dividend Discount Model and other methods.Likewise, during certain periods such as the market bottom in 2009, it was clear to many value investors that the market was very undervalued.

In these circumstances, wouldn’t it be optimal to change the balance accordingly? During the top of the dotcom bubble, wouldn’t it be rational to reduce stock exposure to well under the normal target? And during deep market bottoms, wouldn’t it be rational to increase stock exposure to well over the normal target?

It depends on what your goals are.

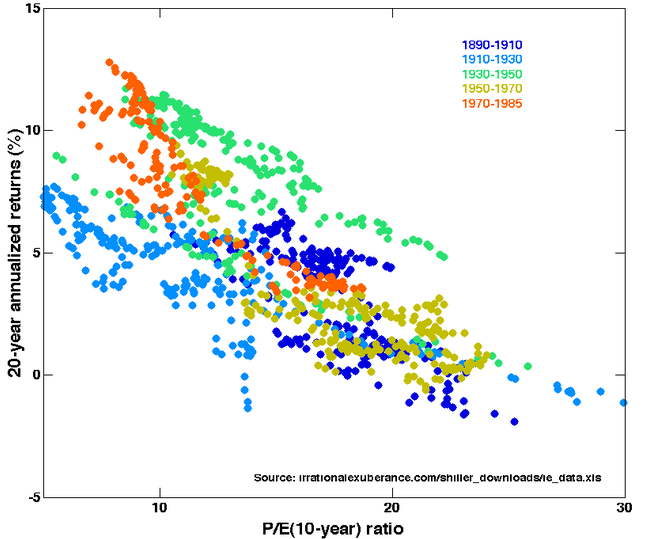

If you’d like to be a bit more active with your portfolio, then the Shiller P/E is a good tool to use. The Shiller PE, put forth by Robert Shiller, Yale Economist, is a calculation of the current market valuation. It divides the price of the market by the inflation-adjusted average of the last ten years of earnings to provide a smoothed-out representation of what the current valuation of the market is compared to what it historically has been.

The chart shows that, over a century-long period, the current market valuation is inversely proportional with the expected annualized returns over the next 20 years. In other words, the higher the current market valuation is (as calculated by the Shiller P/E ratio), the less likely it is you’ll get good returns over the next 20 years:

Image Source

The chart ends in 2005 (20 years after the last mark of 1985), but the accuracy has continued up until the present day. The decade from 2000-2010 was absolutely terrible for equities because the market was ridiculously overvalued in the late 1990”²s and early 2000”²s.

Given the rather well-evidenced (and inherently logical) premise that highly valued markets offer statistically lower returns, there is a semi-popular investing method that takes this into account.

With this method, an indexed portfolio is rebalanced actively. Rather than sticking to a static stock/bond allocation, such as 70%/30%, the ratio is adjusted based on the Shiller P/E of the market. The higher the Shiller P/E, the lower the stock allocation. And the lower the Shiller P/E, the higher the stock allocation.

The precise method of active rebalancing could be up to you, but here’s an example. Again, I used a simple two-part stock/bond portfolio to explain the point rather than the more realistic US/Foreign/Bond portfolio that would be better to go with.

-When the Shiller P/E of the market is 18, the portfolio shall be 80% stock and 20% bonds.

-For each point that the Shiller P/E rises, the stock percentage shall be decreased by 2%.

-For each point that the Shiller P/E falls, the stock percentage shall be increased by 2%.

So, if the Shiller P/E is 21, the portfolio shall be 76% stock and 24% bonds. If the Shiller P/E is 15, the portfolio shall be 86% stock and 14% bonds. And so on.

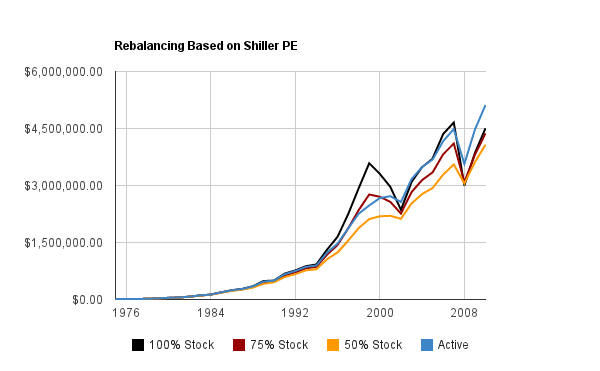

This is what the results would have been between 1975 and 2010, compared with the passive portfolios, where “Active” is this actively rebalanced portfolio:

The returns were slightly better, and the volatility was fairly modest. “Active” is probably even an overstatement, because this accounts for a rebalancing only once per year, so it’s about 10 minutes of work per year.

Whether this is a method to go with isn’t conclusive, though.

The overall returns are better, but they’re not that much better.

Given that a) most people won’t stick to the plan and b) the returns aren’t dramatically improved, there’s not a strong reason for everyone to follow that method. Passive rebalancing is perfectly fine. But if you enjoy investing and want to reduce or increase your equity exposure based on the market valuation, it can be a worthwhile approach that likely leads to improved returns and reduced volatility if it’s done with discipline. Personally I wouldn’t recommend it for most people that I encounter, but the information is around for those that want to pursue the method of taking market valuations into account for determining the balance of portfolio assets.

Specific Index Funds to Consider Investing In

The business that really started the index fund is Vanguard. And because they were the first mover and with such a strong focus on index funds, they’re the largest player today. Due to their size, they can generally keep expense ratios below any other competitor, and because of their focus, they don’t try to upsell you to actively managed funds. Plus, Vanguard is itself owned by its own funds (in other words, the investors), which really locks down the expenses. (For the record, I’m not in any way associated with Vanguard financially.)There are a few main ways to invest via Vanguard funds.

Indexed Mutual Funds

These indexes are structured as mutual funds. You can open open an account with them, and the minimum amount to invest depends on the specific fund but is typically several thousand dollars. Here are some of the options:

Total Stock Market Index Fund Investor Shares

This fund invests small, medium, and large publicly traded American companies, and has an expense ratio of only 0.18%.

High Dividend Yield Investor Shares

This fund invests in over 400 companies that pay medium and high dividend yields. The yield is over 3% and the expense ratio is 0.25%.

Total Bond Market Index Fund Admiral Shares

Here’s a good bond fund, diversified across over 5,000 bonds with a 0.10% expense ratio.

Total International Stock Index Fund Investor Shares

For international exposure, this is a good choice. The fund includes over 6,000 companies from around the world, but excludes U.S. companies so that you can pair this with a U.S. index without overlapping. The expense ratio is 0.22%.

If you hold simply a U.S. stock fund, and international stock fund, and a bond fund, your portfolio is pretty diversified. If you live in Canada or the UK or another country, you may want to modify that with greater emphasis on your home country, but the basics are the same.

Funds of Funds

An even simpler method is to invest in a fund of funds. Let Vanguard rebalance your own funds for you. In these structures, Vanguard groups together some of the funds from the previous category into a fund of funds that they keep at a specific balance.

LifeStrategy Growth Fund

This fund is split between the Total Stock Market fund (56%), the Total International Stock Market fund (24%), and the Total Bond Market fund (20%). The expense ratio is 0.17%, and the primary goal here is to grow the wealth with manageable volatility.

LifeStrategy Income Fund

This fund inverses the balance compared to the previous fund, consisting of bonds (80%), U.S. stocks (14%) and international stocks (6%). It’s meant for retirement to keep volatility and risk lower, and the expense ratio is 0.13%. There are two other options that rest between these two funds in terms of stock/bond ratios.

Target Retirement 2040 Fund

This fund is a bit different than the others, because the fund will shift towards bonds over time. As of this writing, it currently consists of 63% U.S. stock, 27% international stock, and 10% bonds. Over time, the bond ratio will grow larger and larger, to reduce volatility as you near retirement. Vanguard offers these funds in five-year increments, so you pick the fund that corresponds to your expected retirement year.

With these funds of funds, you’re sufficiently diversified if you invest in them. Apart from holding property and cash, your job as an investor here is just to shovel as much money into these funds as possible and let Vanguard do the rest. It takes no management from you at all except to check your balances once in a while and keep up with paperwork and taxes (a few hours per year at most), so you can focus your efforts on increasing your income, living life, etc.

Indexed ETFs

These funds are similar to the first group of mutual funds, but they’re wrapped in a structure that is traded on a stock exchange. This is why they are called Exchange Traded Funds (ETFs). You don’t need a Vanguard account for these; you can buy them through any brokerage account just like you would buy any stock.

Total Stock Market ETF (VTI)

Vanguard’s ETF invests in over 3,000 U.S. companies and has an expense ratio of 0.06%.

Total Bond Market ETF (BND)

Vanguard’s Bond Market ETF with an expense ratio of 0.10%.

Total International Stock ETF (VXUS)

Vanguard’s International Stock ETF with a 0.18% expense ratio.

These are the same as their equivalent mutual funds. They’re more flexible, because you can buy and sell them through any broker. There is not currently a fund-of-funds ETF option through Vanguard.

How to Combine Index Funds and Individual Stocks

Despite the fact that I run this site that focuses on individual stock selection, I think it’s pretty clear that out of the general population, most people do not have a strong interest in investing, do not find it “fun”, are not willing to put a lot of time into it, and their chances of beating the market over time are not high based on a fairly high degree of market efficiency. Most of my writing is aimed towards the subset of investors that are interested in value investing, which includes myself.So, to be clear, I think that for 90% of the population, going with a passive and purely indexed approach is the most optimal investing method.

If you’re like me, and for one reason or another you want to own individual stocks as well (because you want to retain your shareholder voting rights rather than wasting them, or you think you can beat the market with a smart investing approach, or you want higher and more consistent dividend income, or another reason), then there are some seamless ways to combine indexes and individual stocks.

The easiest option is to split investments between different accounts. For example, if you have a 401(k), then you can fill that with a few index funds. Then if you have an IRA or a taxable account on the side, you could look into building a portfolio of stocks that pay good dividends, or growth stocks you know well, etc. If the bulk of your wealth is diversified and indexed, then trying your hand at stock picking can keep your risks low.

If you combine things together, then you just have to keep track of your overall diversification. For example, if you have a regular brokerage account filled with indexed ETFs and some individual stocks, then make sure you keep track of what you’re overall diversification is.

For example, let’s say you have $50,000 in a bond ETF, $50,000 in an international stock ETF, and $100,000 in a U.S. stock ETF, and you also own $50,000 worth of individual U.S. stocks split between 10 holdings. In this scenario, the indexed portion of your portfolio is split between 50% U.S. stocks, 25% international stocks, and 25% bonds. The overall split including the individual stocks is 60% U.S. stocks, 20% international stocks, and 20% bonds.

Whatever target balance you’re aiming for, you have to make sure to include your individual stock holdings.

Another way to use index funds is to use some of the more targeted ones to give your portfolio exposure to certain markets. For example, if you own a portfolio mainly consisting of dividend stocks, you may be a bit light in certain industries, like technology. Or you may feel that your overall exposure is a bit too focused on large caps, or not globally diversified to your liking. If that’s the case, then you can hold a technology index fund like the Vanguard Information Technology ETF (VGT), or an index that focuses on small caps, or an international index fund. Or, let’s say you don’t feel comfortable picking stocks in a certain industry, like health care for example. That’s where an index that focuses on the health care industry can give you exposure to that industry and complement the rest of your portfolio.

The Best Books on Index Funds

While this article provides as much detail as possible, the length of a blog post becomes ridiculous after a certain point. I may add to and improve this page over time. If you’ve gotten this far, you’ve probably clicked to other sites and back to this article several times, or you scanned rather than read, which is natural.So if you’d like some further reading on index funds, there are a few books that are good choices.

Millionaire Teacher

This is the #1 personal finance and investing book I’d recommend to people. It’s a good update on the established concepts. The author, Andrew Hallam, is an English teacher that became a millionaire in his 30”²s through frugality and index investing. Andrew is personable, so this book is concise, flowing, and quick to read, yet well-researched and thorough.

The Little Book of Common Sense Investing

Written By John Bogle, founder and retired CEO of Vanguard, this book is another concise and good read about index funds.

A Random Walk Down Wall Street

Burton Malkiel looks through various investment strategies and shows that they will underperform a passive investing approach. There have been several editions, and this is one of the original books about indexing, since it even predates index funds.

Conclusion: Why 90%+ of People Should Invest in Index Funds

Overall, index investing is one of the most viable wealth-building strategies, especially when combined with cash and real estate.It’s the investing approach that takes the least amount of time, and although there are some drawbacks, there are plenty of advantages. In the simplest sense, it involves managing a portfolio that looks something like this:

In a more complicated scenario, it means keeping track of a few accounts which may include pure indexes, or indexes combined with individual stocks. If you own individual stocks, then index ETFs can still be quite useful to own assets in certain industries or to balance out your portfolio.