Wal-Mart Stores Inc. (WMT, Financial) is one of the largest retailers in the world.

-Seven Year Revenue Growth Rate: 5.8%

-Seven Year EPS Growth Rate: 9.4%

-Seven Year Dividend Growth Rate: 14.9%

-Current Dividend Yield: 2.43%

-Balance Sheet: Reasonable Leverage, Stable

Currently, Walmart’s $77 share price appears to be fairly valued for an expectation of 10% long-term returns.

For fiscal year 2014, $12-13 billion is expected to be invested by the company. This includes up to $6 billion in the U.S. segment, up to $5 billion in the international segment, and up to $2 billion in the Sam’s Club segment and other areas.

Walmart U.S.

Walmart U.S. contributes over $274 billion in sales, and in this last year has surpassed 4,000 locations and 641 million square feet of retail space. More than 135 million customers are served weekly by Walmart in the U.S. The number of locations has increased by an average rate of a bit under 2% per year over the last four years, from 3,703 in the year 2009 to 4,005 as of the most recent quarter.

Walmart International

Walmart International contributes over $135 billion in sales with over 6,000 locations and 348 million square feet of retail space. International locations are generally significantly smaller than the superstore format in the United States. Weekly customer numbers surpass 105 million. The number of locations has increased by over 14% per year over the last four years, from 3,595 in 2009 to 6,148 as of the most recent quarter.

Sam’s Club

Sam’s Club contributes over $56 billion in sales with 620 locations and 83 million square feet of retail space. Annual growth in the number of location has been less than half of one percent per year, from 611 in 2009 to 620 currently.

Price to Free Cash Flow: 20

Price to Book: 3.3

Return on Equity: 23%

(Chart Source: DividendMonk.com)

Over the last seven years, the average annual revenue growth rate has been a respectable 5.8%.

(Chart Source: DividendMonk.com)

EPS grew by an average of 9.4% per year over the last seven years, and the dividend grew by 14.9% per year over the same period.

The dividend yield is now 2.43% and the dividend payout ratio from earnings is a bit over 30%.

Approximate historical dividend yield at beginning of each year:

The shareholder yield of Walmart tends to be over 5% in these recent years.

The interest coverage ratio is over 12x.

Overall, Walmart has historically used a decent amount of leverage to improve returns without much risk, and the current balance sheet continues to reflect this trend.

During periods where Walmart has had lackluster stock performance, it has been because the stock valuation got ahead of itself. Walmart stock was a poor performer in the previous decade because the company was irrationally overvalued at the turn of the millennium, but the stock began offering better returns in recent years as the increasing EPS finally caught up with the stock price and hit the point of being rather fairly valued.

As far as I see it, the competitive landscape for Walmart is reasonable for the foreseeable future. Being a mid-level retailer rather than a high-end or bargain retailer is likely to be quite a challenge in the U.S. with rising healthcare and tuition costs hurting the middle class, and Walmart’s position as a bargain retailer keeps it out of that dangerous middle territory.

The company has some defense from online retailers and niche retailers due to its product diversification. Groceries account for more than half of Walmart sales, and this is not a segment that can be replicated by a purer play online retailer; even if ordered online, grocery sales require a substantial physical distribution system. Many Walmart locations include a pharmacy as well. The company’s other areas such as electronics, home care needs, and clothes are a bit more up in the air as far as future prediction is concerned, but they tend to be competitively priced.

Walmart’s international business operations have not enjoyed the same consistency and success as the early expansion in the US. Growth is robust, and should continue to post good numbers, but the company hasn’t been able to generate the domestic efficiency on a worldwide basis. And on the domestic side, over the last few years, comparable same-store sales have gone down and up.

Online competitors threaten some of the product segments, at least to a certain extent. Amazon, for example, grew sales by whopping 25+% last year, and isn’t on any course to slow down. Quite often, if there are one or two things you need, it’s typically convenient to just buy them on Amazon and receive them a few days later at your home rather than to make a trip out to a store.

Continued growth for the company will have to come from successful international expansion and defensive positioning in the US, such as through strengthening of the online business and keeping physical locations as relevant as possible.

With a year of EPS growth without much stock price growth, Walmart once again appears to be fairly priced.

According the Dividend Discount Model, the current price of over $77 is justified for a 10% expected long-term annual rate of return if dividend growth exceeds 7.5% for the foreseeable future. This is lower than the historical EPS and dividend growth, so there is a comfortable margin for Walmart to hit these numbers.

The yield is a bit on the low side, but quantitatively the price appears to be fair. The question then shifts towards the qualitative: if you believe Walmart will continue to be a competitive retailer with a decent economic moat, then an investment in Walmart at the current time appears reasonable.

Full Disclosure: As of this writing, I have no position in WMT.

-Seven Year Revenue Growth Rate: 5.8%

-Seven Year EPS Growth Rate: 9.4%

-Seven Year Dividend Growth Rate: 14.9%

-Current Dividend Yield: 2.43%

-Balance Sheet: Reasonable Leverage, Stable

Currently, Walmart’s $77 share price appears to be fairly valued for an expectation of 10% long-term returns.

Overview

Founded in Arkansas in 1962 by Sam Walton, Walmart is now one of the largest companies in the world, with revenue of over $460 billion and with 2.2 million employees. They have stores under a variety of brands in 25+ countries around the world. In addition to being a massive retailer, it’s the largest seller of groceries in the United States. Walmart also owns Sam’s Club, which is a membership warehouse much like Costco that offers bulk products for a reduced cost to people that pay for a membership.For fiscal year 2014, $12-13 billion is expected to be invested by the company. This includes up to $6 billion in the U.S. segment, up to $5 billion in the international segment, and up to $2 billion in the Sam’s Club segment and other areas.

Walmart U.S.

Walmart U.S. contributes over $274 billion in sales, and in this last year has surpassed 4,000 locations and 641 million square feet of retail space. More than 135 million customers are served weekly by Walmart in the U.S. The number of locations has increased by an average rate of a bit under 2% per year over the last four years, from 3,703 in the year 2009 to 4,005 as of the most recent quarter.

Walmart International

Walmart International contributes over $135 billion in sales with over 6,000 locations and 348 million square feet of retail space. International locations are generally significantly smaller than the superstore format in the United States. Weekly customer numbers surpass 105 million. The number of locations has increased by over 14% per year over the last four years, from 3,595 in 2009 to 6,148 as of the most recent quarter.

Sam’s Club

Sam’s Club contributes over $56 billion in sales with 620 locations and 83 million square feet of retail space. Annual growth in the number of location has been less than half of one percent per year, from 611 in 2009 to 620 currently.

Ratios

Price to Earnings: 15Price to Free Cash Flow: 20

Price to Book: 3.3

Return on Equity: 23%

Revenue

(Chart Source: DividendMonk.com)

Over the last seven years, the average annual revenue growth rate has been a respectable 5.8%.

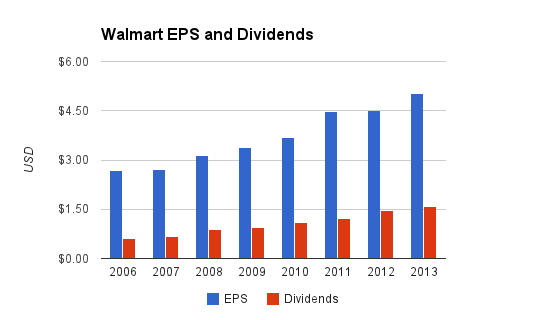

EPS and Dividends

(Chart Source: DividendMonk.com)

EPS grew by an average of 9.4% per year over the last seven years, and the dividend grew by 14.9% per year over the same period.

The dividend yield is now 2.43% and the dividend payout ratio from earnings is a bit over 30%.

Approximate historical dividend yield at beginning of each year:

| Year | Yield |

|---|---|

| Current | 2.43% |

| 2013 | 2.3% |

| 2012 | 2.5% |

| 2011 | 2.2% |

| 2010 | 2.0% |

| 2009 | 1.7% |

| 2008 | 1.9% |

| 2007 | 1.4% |

| 2006 | 1.3% |

How Does Walmart Spend its Cash?

Walmart generated over $34 billion in free cash flow cumulatively in the fiscal years 2011, 2012, and 2013. Over this same period, a bit under $15 billion was spent on dividends, and over $28 billion was spent on share buybacks. About $4 billion was spent on acquisitions.The shareholder yield of Walmart tends to be over 5% in these recent years.

Balance Sheet

The total debt/equity ratio is a bit under 70%, and the total debt/income ratio is approximately 3x. Goodwill makes up over $20 billion out of the $76 billion existing shareholder equity.The interest coverage ratio is over 12x.

Overall, Walmart has historically used a decent amount of leverage to improve returns without much risk, and the current balance sheet continues to reflect this trend.

Investment Thesis

Walmart has essentially been a machine of consistent shareholder returns since its founding. Through a predictable use of capital for expansions, share buybacks, and growing dividends, Walmart has achieved atypically consistent EPS growth and overall shareholder returns. The larger portion of the expected returns are internal: from using capital to buy back shares and pay dividends, and the smaller portion is from actual growth: inflation, new stores, and comparable increases in existing stores.During periods where Walmart has had lackluster stock performance, it has been because the stock valuation got ahead of itself. Walmart stock was a poor performer in the previous decade because the company was irrationally overvalued at the turn of the millennium, but the stock began offering better returns in recent years as the increasing EPS finally caught up with the stock price and hit the point of being rather fairly valued.

As far as I see it, the competitive landscape for Walmart is reasonable for the foreseeable future. Being a mid-level retailer rather than a high-end or bargain retailer is likely to be quite a challenge in the U.S. with rising healthcare and tuition costs hurting the middle class, and Walmart’s position as a bargain retailer keeps it out of that dangerous middle territory.

The company has some defense from online retailers and niche retailers due to its product diversification. Groceries account for more than half of Walmart sales, and this is not a segment that can be replicated by a purer play online retailer; even if ordered online, grocery sales require a substantial physical distribution system. Many Walmart locations include a pharmacy as well. The company’s other areas such as electronics, home care needs, and clothes are a bit more up in the air as far as future prediction is concerned, but they tend to be competitively priced.

Risks

Walmart, like any other company, has risks. When all is said and done, Walmart is really just a middle-man, buying products of others and selling them to customers. They are vulnerable to changes in consumer demand.Walmart’s international business operations have not enjoyed the same consistency and success as the early expansion in the US. Growth is robust, and should continue to post good numbers, but the company hasn’t been able to generate the domestic efficiency on a worldwide basis. And on the domestic side, over the last few years, comparable same-store sales have gone down and up.

Online competitors threaten some of the product segments, at least to a certain extent. Amazon, for example, grew sales by whopping 25+% last year, and isn’t on any course to slow down. Quite often, if there are one or two things you need, it’s typically convenient to just buy them on Amazon and receive them a few days later at your home rather than to make a trip out to a store.

Continued growth for the company will have to come from successful international expansion and defensive positioning in the US, such as through strengthening of the online business and keeping physical locations as relevant as possible.

Conclusion and Valuation

Walmart’s value seems to have caught up with its share price. When I published a report on Walmart last year, the stock price was at around $73, and I stated that the stock appears to have gotten ahead of itself, wasn’t at very good price, and that it would be better to look for dips into the mid-$60”²s. Since then, the stock did dip down into the mid-to-high $60”²s, and has now climbed to a bit over $77. Since that report, the S&P 500 has climbed over 20% whereas Walmart stock has only increased by a bit over 5%.With a year of EPS growth without much stock price growth, Walmart once again appears to be fairly priced.

According the Dividend Discount Model, the current price of over $77 is justified for a 10% expected long-term annual rate of return if dividend growth exceeds 7.5% for the foreseeable future. This is lower than the historical EPS and dividend growth, so there is a comfortable margin for Walmart to hit these numbers.

The yield is a bit on the low side, but quantitatively the price appears to be fair. The question then shifts towards the qualitative: if you believe Walmart will continue to be a competitive retailer with a decent economic moat, then an investment in Walmart at the current time appears reasonable.

Full Disclosure: As of this writing, I have no position in WMT.