John Hussman - Following the Fed to 50% Flops (June 3, 2013)

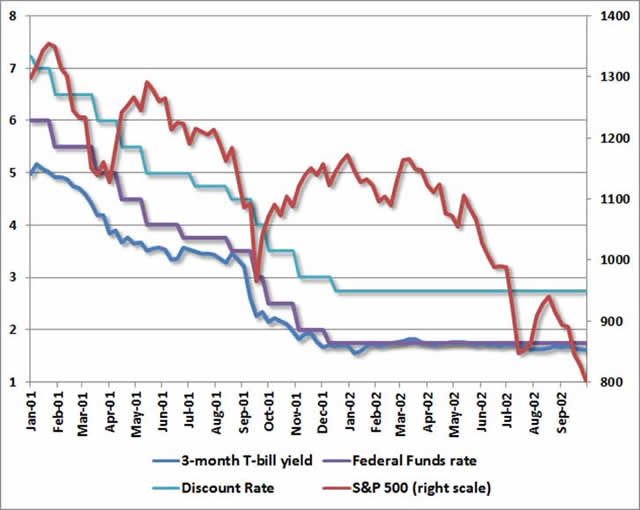

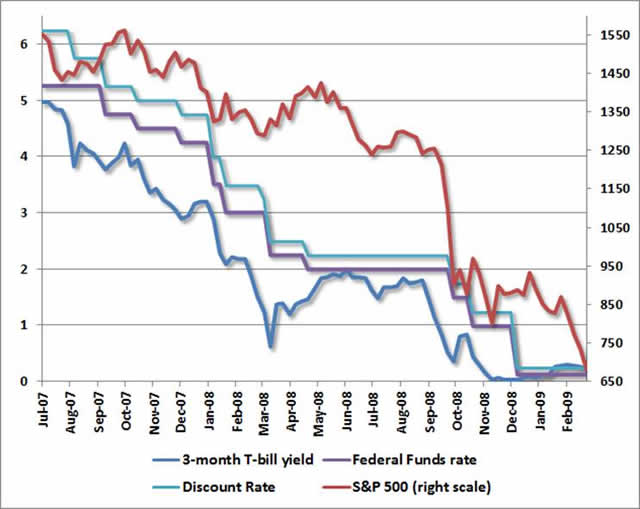

One of the most strongly held beliefs of investors here is the notion that it is inappropriate to “Fight the Fed” – reflecting the view that Federal Reserve easing is sufficient to keep stocks not only elevated, but rising. What’s baffling about this is that the last two 50% market declines – both the 2001-2002 plunge and the 2008-2009 plunge – occurred in environments of aggressive, persistent Federal Reserve easing.

It’s certainly true that favorable monetary conditions are helpful for stocks, on average. But that average hides a lot of sins.

There are many ways to define monetary conditions using policy rates, market yields, and variables such as the monetary base or other aggregates. But given the strong relationship between monetary base/GDP and interest rates, these measures overlap quite a bit, and the results are quite general regardless of the precise definition. For discussion purposes, we’ll define “favorable” monetary conditions here as: either the Federal Funds rate, the Discount Rate, or the 3-month Treasury bill yield lower than 6 months prior, or the last move in the Fed Funds or Discount Rate being an easing. Historically, this captures about 52% of historical periods. During these periods, the total return of the S&P 500 averaged 13.5% annually, versus just 8.8% annually when monetary conditions were not favorable.

This is a worthwhile distinction, but it doesn’t partition the data enough to separate out periods where the average return on the S&P 500 was below Treasury bills. So historically, using this indicator alone would have suggested holding stocks regardless of monetary conditions. One might expect to do better by taking a leveraged exposure during favorable monetary conditions, and a muted exposure during unfavorable conditions, but this strategy would have invited intolerable risks. Strikingly, the maximum drawdown of the S&P 500, confined to periods of favorablemonetary conditions since 1940, would have been a 55% loss. This compares with a 33% loss during unfavorablemonetary conditions. This is worth repeating – favorable monetary conditions were associated with far deeperdrawdowns.

If this all seems preposterous and counterintuitive, consider the last two market plunges. While investors seem to have forgotten this inconvenient history, the 2001-2002 market plunge went hand-in-hand with continuous and aggressive monetary easing.

Ditto for the 2008-2009 market plunge. Persistent monetary easing did nothing to prevent a 55% collapse in the S&P 500.

From an asset allocation perspective, even simple trend-following methods have performed far better historically than following monetary policy. For example, since 1940, when the S&P 500 has been above its 200-day moving average, the total return of the index has averaged 14.2% annually, versus just 4.5% when the index has been below its 200-day average. That separation in returns is meaningful, because the return during periods of unfavorable trends did not exceed Treasury bill returns, so it would not have harmed long-term performance to be out of the market during those periods (at least, before transaction costs, taxes and slippage). The deepest loss of the S&P 500, confined to periods of “favorable” trends and reflecting occasional whipsaws, was -26%, versus -53% during unfavorable trends.

As I noted a few weeks ago (see Aligning Investment Exposure with the Expected Return/Risk Profile), all of the net historical benefit of favorable trend-following has occurred in periods where “overvalued, overbought, overbullish” characteristics have been absent. In the presence of this syndrome, the average total return of the S&P 500 collapses below Treasury bill yields, on average. The same is true, on average, when favorable monetary conditions are coupled with overvalued, overbought, overbullish features.

Hands-down, the worst-case scenario is a market that comes off of such overextended conditions and then breaks trend-support in the context of an economic downturn. That’s not something we observe at present, but it is something to keep in mind, as I doubt that we will avoid that sequence over the completion of the current market cycle.

Part of the reason that monetary policy was so ineffective during 2001-2002 and 2008-2009 is that these market collapses were preceded by overvalued, overbought, overbullish euphoria, and then gave way to economic downturns. Though monetary policy certainly fed the preceding bubbles, monetary policy did not prevent or halt those recessions, and those recessions were not broadly recognized until stocks had already lost about 30% of their value. At least in post-war data (Depression-era data is more challenging), the proper investment approach has generally been to accept market risk in the presence of favorable market action, particularly if monetary conditions are supportive, to start walking when overvalued, overbought, overbullish conditions emerge, and to run once momentum rolls over (as it has already). There’s a grey area when such overextended conditions are cleared, which can allow for recovery rallies if market action is still supportive. But regardless of monetary policy, investors should avoid risk in richly-valued environments once market action deteriorates, and buckle up hard on signs of economic weakness once an overvalued market loses trend support.

The following point should not be missed. I am not saying that monetary conditions are unimportant. Indeed, provided that trend-following conditions are favorable and overvalued, overbought, overbullish conditions are absent, favorable monetary conditions have contributed to stronger total returns for the S&P 500, and reduced periodic losses, in data since 1940. Favorable monetary conditions are most useful in confirming and supporting favorable evidence on other measures. My concern here, however, is that investors seem to believe that favorable monetary conditions are a vetoagainst all other possible risks, regardless of whether those risks are financial (e.g. overvalued, overbought, overbullish conditions) or economic. This is dangerously incorrect.

There is no question that Fed action can affect economic outcomes when it relaxes some economic constraint that is actually binding (for example, during bank runs, when Fed-provided liquidity is essential). But there is little evidence of any transmission mechanism whereby a greater supply of idle bank reserves promises to make a dent in the economy beyond occasional and short-lived can-kicks. There is also no question that interest rates matter, given that stocks must compete with bonds. But stocks are much longer duration securities than investors seem to appreciate, and the relationship between stock yields and interest rates is not even close to one-to-one, despite what Fed Model proponents might suggest.

Even so, investors have come to believe that there is a direct cause-and-effect link from monetary easing to rising security prices. The historical evidence is much less supportive. Interestingly, if we look at conditions that have been most generally hostile for stocks on average (S&P 500 below its 200-day moving average, or overvalued, overbought, overbullish conditions in place), more than half of these periods were accompanied by “favorable” monetary conditions. Stocks proceeded to underperform Treasury bills anyway, on average, with steep interim losses.

Conversely, monetary conditions have been unfavorable in nearly half of historical periods where trends were supportive and overvalued, overbought, overbullish features were absent. In those periods, the average total return of the S&P 500 was still quite strong, and returns were only slightly lower than when monetary conditions were favorable under otherwise similar conditions (15.6% vs. 18.9% at an annual rate), while periodic drawdowns increased only slightly.

So again, the point is not that favorable monetary conditions are irrelevant. The point is that they are not omnipotent – and that the most severe market losses on record have been accompanied by aggressive easing. Without question, quantitative easing has been very effective in suppressing spikes in risk premiums in recent years. More recently, it has been effective in removing any perception that stocks have risk and creating the impression that easy money is enough to override every possible economic or financial concern. But that is where perception has moved beyond reality. There is no evidence in the historical record for such optimism. Indeed, even the recovery from the 2009 lows was more directly linked to the change by the Financial Accounting Standards Board to eliminate “mark-to-market” accounting (keeping banks from insolvency even if they were technically insolvent) and the shift to an outright guarantee of Fannie Mae and Freddie Mac debt by the U.S. Treasury. It is superstition to believe that monetary easing is a panacea. Investors who recognize (actually, simply remember) this now are likely to fare better than those who are forced to relearn it later.

Needless to say, all of this will be summarily ignored by speculators who have been rewarded by the strategy of following the Fed in a mature, overvalued, overbought, overbullish, unfinished half-cycle that recently hit new highs. Advice from Kenny Rogers – you never count your money when you’re sittin’ at the table.

Economic Notes

We’re observing some very wide dispersion in regional economic surveys in recent reports. On one hand, the Chicago Purchasing Managers Index surged to 58.7 last month, with the important new orders component jumping to 58.1 (a level of 50 on the PMI is neutral). This sort of strength, if sustained over several months and joined by strength in the Philadelphia Fed index, would help to ease our economic concerns here, as several months of strength on these two measures are among the more reliable leading indicators of economic shifts.

On the other hand, in nearby Milwaukee, the PMI collapsed from 48.4 to 40.7, while the Philadelphia Fed index itself dropped into negative territory, falling from +1.3 to -5.2, with the new orders component deteriorating from -1.0 to -7.9. That general weakness was much more in line with what we’re observing from other surveys, including the Chicago Fed National Activity Index, Empire Manufacturing, Dallas Fed, and Richmond Fed.

When we plot “outliers” (where the Chicago PMI deviates from the average of the other surveys), against subsequentchanges in the Chicago PMI, what results is a clearly downward-sloping scatter, meaning that positive outliers, as we presently observe, are typically corrected by subsequent disappointments in the Chicago PMI. Conversely, however, outliers in the Chicago PMI are typically not related to subsequent positive surprises in the other indices. Again, jointstrength in the Chicago PMI New Orders component and the Philly Fed index, sustained over a period of 3-4 months, does tend to lead broader improvements. This is not what we observe here.

In short, the coincident and leading economic evidence is deteriorating, not improving. Even the chart below incorporates a strong Chicago PMI figure that appears to be a temporary outlier. Employment data is a well-known lagging indicator, and is always somewhat “rear-view”, but it’s fair to say that given what is now the lowest labor participation rate in 30 years, the relatively restrained level of new claims for unemployment has been a bright spot.

It seems to be universally assumed that surprisingly strong data on the economic and jobs front would pose the greatest risk to the market, as it would accelerate the “taper” of quantitative easing. To the contrary, the largest risk here would be an acceleration of disappointing economic data, as it would further reinforce the case made by former Fed Chairman Paul Volcker that the benefits of quantitative easing are “limited and diminishing.” Disappointments on the economic front may be met with knee-jerk enthusiasm. But the quickest path to an extended bear market would be a deteriorating economy, coupled with recognition that quantitative easing has an even weaker benefit/cost tradeoff than is already plain.

Hussman Funds

One of the most strongly held beliefs of investors here is the notion that it is inappropriate to “Fight the Fed” – reflecting the view that Federal Reserve easing is sufficient to keep stocks not only elevated, but rising. What’s baffling about this is that the last two 50% market declines – both the 2001-2002 plunge and the 2008-2009 plunge – occurred in environments of aggressive, persistent Federal Reserve easing.

It’s certainly true that favorable monetary conditions are helpful for stocks, on average. But that average hides a lot of sins.

There are many ways to define monetary conditions using policy rates, market yields, and variables such as the monetary base or other aggregates. But given the strong relationship between monetary base/GDP and interest rates, these measures overlap quite a bit, and the results are quite general regardless of the precise definition. For discussion purposes, we’ll define “favorable” monetary conditions here as: either the Federal Funds rate, the Discount Rate, or the 3-month Treasury bill yield lower than 6 months prior, or the last move in the Fed Funds or Discount Rate being an easing. Historically, this captures about 52% of historical periods. During these periods, the total return of the S&P 500 averaged 13.5% annually, versus just 8.8% annually when monetary conditions were not favorable.

This is a worthwhile distinction, but it doesn’t partition the data enough to separate out periods where the average return on the S&P 500 was below Treasury bills. So historically, using this indicator alone would have suggested holding stocks regardless of monetary conditions. One might expect to do better by taking a leveraged exposure during favorable monetary conditions, and a muted exposure during unfavorable conditions, but this strategy would have invited intolerable risks. Strikingly, the maximum drawdown of the S&P 500, confined to periods of favorablemonetary conditions since 1940, would have been a 55% loss. This compares with a 33% loss during unfavorablemonetary conditions. This is worth repeating – favorable monetary conditions were associated with far deeperdrawdowns.

If this all seems preposterous and counterintuitive, consider the last two market plunges. While investors seem to have forgotten this inconvenient history, the 2001-2002 market plunge went hand-in-hand with continuous and aggressive monetary easing.

Ditto for the 2008-2009 market plunge. Persistent monetary easing did nothing to prevent a 55% collapse in the S&P 500.

From an asset allocation perspective, even simple trend-following methods have performed far better historically than following monetary policy. For example, since 1940, when the S&P 500 has been above its 200-day moving average, the total return of the index has averaged 14.2% annually, versus just 4.5% when the index has been below its 200-day average. That separation in returns is meaningful, because the return during periods of unfavorable trends did not exceed Treasury bill returns, so it would not have harmed long-term performance to be out of the market during those periods (at least, before transaction costs, taxes and slippage). The deepest loss of the S&P 500, confined to periods of “favorable” trends and reflecting occasional whipsaws, was -26%, versus -53% during unfavorable trends.

As I noted a few weeks ago (see Aligning Investment Exposure with the Expected Return/Risk Profile), all of the net historical benefit of favorable trend-following has occurred in periods where “overvalued, overbought, overbullish” characteristics have been absent. In the presence of this syndrome, the average total return of the S&P 500 collapses below Treasury bill yields, on average. The same is true, on average, when favorable monetary conditions are coupled with overvalued, overbought, overbullish features.

Hands-down, the worst-case scenario is a market that comes off of such overextended conditions and then breaks trend-support in the context of an economic downturn. That’s not something we observe at present, but it is something to keep in mind, as I doubt that we will avoid that sequence over the completion of the current market cycle.

Part of the reason that monetary policy was so ineffective during 2001-2002 and 2008-2009 is that these market collapses were preceded by overvalued, overbought, overbullish euphoria, and then gave way to economic downturns. Though monetary policy certainly fed the preceding bubbles, monetary policy did not prevent or halt those recessions, and those recessions were not broadly recognized until stocks had already lost about 30% of their value. At least in post-war data (Depression-era data is more challenging), the proper investment approach has generally been to accept market risk in the presence of favorable market action, particularly if monetary conditions are supportive, to start walking when overvalued, overbought, overbullish conditions emerge, and to run once momentum rolls over (as it has already). There’s a grey area when such overextended conditions are cleared, which can allow for recovery rallies if market action is still supportive. But regardless of monetary policy, investors should avoid risk in richly-valued environments once market action deteriorates, and buckle up hard on signs of economic weakness once an overvalued market loses trend support.

The following point should not be missed. I am not saying that monetary conditions are unimportant. Indeed, provided that trend-following conditions are favorable and overvalued, overbought, overbullish conditions are absent, favorable monetary conditions have contributed to stronger total returns for the S&P 500, and reduced periodic losses, in data since 1940. Favorable monetary conditions are most useful in confirming and supporting favorable evidence on other measures. My concern here, however, is that investors seem to believe that favorable monetary conditions are a vetoagainst all other possible risks, regardless of whether those risks are financial (e.g. overvalued, overbought, overbullish conditions) or economic. This is dangerously incorrect.

There is no question that Fed action can affect economic outcomes when it relaxes some economic constraint that is actually binding (for example, during bank runs, when Fed-provided liquidity is essential). But there is little evidence of any transmission mechanism whereby a greater supply of idle bank reserves promises to make a dent in the economy beyond occasional and short-lived can-kicks. There is also no question that interest rates matter, given that stocks must compete with bonds. But stocks are much longer duration securities than investors seem to appreciate, and the relationship between stock yields and interest rates is not even close to one-to-one, despite what Fed Model proponents might suggest.

Even so, investors have come to believe that there is a direct cause-and-effect link from monetary easing to rising security prices. The historical evidence is much less supportive. Interestingly, if we look at conditions that have been most generally hostile for stocks on average (S&P 500 below its 200-day moving average, or overvalued, overbought, overbullish conditions in place), more than half of these periods were accompanied by “favorable” monetary conditions. Stocks proceeded to underperform Treasury bills anyway, on average, with steep interim losses.

Conversely, monetary conditions have been unfavorable in nearly half of historical periods where trends were supportive and overvalued, overbought, overbullish features were absent. In those periods, the average total return of the S&P 500 was still quite strong, and returns were only slightly lower than when monetary conditions were favorable under otherwise similar conditions (15.6% vs. 18.9% at an annual rate), while periodic drawdowns increased only slightly.

So again, the point is not that favorable monetary conditions are irrelevant. The point is that they are not omnipotent – and that the most severe market losses on record have been accompanied by aggressive easing. Without question, quantitative easing has been very effective in suppressing spikes in risk premiums in recent years. More recently, it has been effective in removing any perception that stocks have risk and creating the impression that easy money is enough to override every possible economic or financial concern. But that is where perception has moved beyond reality. There is no evidence in the historical record for such optimism. Indeed, even the recovery from the 2009 lows was more directly linked to the change by the Financial Accounting Standards Board to eliminate “mark-to-market” accounting (keeping banks from insolvency even if they were technically insolvent) and the shift to an outright guarantee of Fannie Mae and Freddie Mac debt by the U.S. Treasury. It is superstition to believe that monetary easing is a panacea. Investors who recognize (actually, simply remember) this now are likely to fare better than those who are forced to relearn it later.

Needless to say, all of this will be summarily ignored by speculators who have been rewarded by the strategy of following the Fed in a mature, overvalued, overbought, overbullish, unfinished half-cycle that recently hit new highs. Advice from Kenny Rogers – you never count your money when you’re sittin’ at the table.

Economic Notes

We’re observing some very wide dispersion in regional economic surveys in recent reports. On one hand, the Chicago Purchasing Managers Index surged to 58.7 last month, with the important new orders component jumping to 58.1 (a level of 50 on the PMI is neutral). This sort of strength, if sustained over several months and joined by strength in the Philadelphia Fed index, would help to ease our economic concerns here, as several months of strength on these two measures are among the more reliable leading indicators of economic shifts.

On the other hand, in nearby Milwaukee, the PMI collapsed from 48.4 to 40.7, while the Philadelphia Fed index itself dropped into negative territory, falling from +1.3 to -5.2, with the new orders component deteriorating from -1.0 to -7.9. That general weakness was much more in line with what we’re observing from other surveys, including the Chicago Fed National Activity Index, Empire Manufacturing, Dallas Fed, and Richmond Fed.

When we plot “outliers” (where the Chicago PMI deviates from the average of the other surveys), against subsequentchanges in the Chicago PMI, what results is a clearly downward-sloping scatter, meaning that positive outliers, as we presently observe, are typically corrected by subsequent disappointments in the Chicago PMI. Conversely, however, outliers in the Chicago PMI are typically not related to subsequent positive surprises in the other indices. Again, jointstrength in the Chicago PMI New Orders component and the Philly Fed index, sustained over a period of 3-4 months, does tend to lead broader improvements. This is not what we observe here.

In short, the coincident and leading economic evidence is deteriorating, not improving. Even the chart below incorporates a strong Chicago PMI figure that appears to be a temporary outlier. Employment data is a well-known lagging indicator, and is always somewhat “rear-view”, but it’s fair to say that given what is now the lowest labor participation rate in 30 years, the relatively restrained level of new claims for unemployment has been a bright spot.

It seems to be universally assumed that surprisingly strong data on the economic and jobs front would pose the greatest risk to the market, as it would accelerate the “taper” of quantitative easing. To the contrary, the largest risk here would be an acceleration of disappointing economic data, as it would further reinforce the case made by former Fed Chairman Paul Volcker that the benefits of quantitative easing are “limited and diminishing.” Disappointments on the economic front may be met with knee-jerk enthusiasm. But the quickest path to an extended bear market would be a deteriorating economy, coupled with recognition that quantitative easing has an even weaker benefit/cost tradeoff than is already plain.

Hussman Funds