Peak oil is the idea that the world has reached or is about to reach maximum production of oil either a few years ago or a few years from now. From there on we are supposedly going to experience significant declines in oil production, which would have devastating impacts on the world economy, which would need more and more oil in the future. This would be driven by the emerging economies of China and India, where hundreds of million of consumers will enter the middle class, and demand the lifestyle of your typical American Consumer. This will be bullish for companies like Coca-Cola (KO, Financial) as well as energy companies like Chevron (CVX, Financial).

I find some of the cheapest stocks in the market today to be oil companies. I own stock in the following three oil companies:

Chevron Corporation (CVX), through its subsidiaries, engages in petroleum, chemicals, mining, power generation, and energy operations worldwide. The company trades at 9.20 times earnings and yields 3.30%. This dividend champion has increased distributions for 26 years in a row and has achieved a ten year average annual dividend growth of 9.60%. Check my analysis of Chevron Corporation.

ConocoPhillips (COP, Financial) explores for, produces, transports, and markets crude oil, bitumen, natural gas, liquefied natural gas, and natural gas liquids on a worldwide basis. The company trades at 10.10 times earnings and yields 4.20%. This dividend achiever has increased distributions for 12 years in a row and has achieved a ten year average annual dividend growth of 15.10%.Check my analysis of ConocoPhillips.

Royal Dutch Shell plc (RDS.B, Financial) operates as an independent oil and gas company worldwide. The company trades at 8.20 times earnings and yields 5.30%. The company ended a 16 year streak of consecutive dividend increases in 2010 by keeping distributions flat, only to start increasing them again in 2012. Check my analysis of Royal Dutch Shell.

I also used to own Exxon Mobil (XOM, Financial), but I replaced it with ConocoPhillips. Exxon is the largest oil company in the world. It engages in the exploration and production of crude oil and natural gas, and manufacture of petroleum products. The company trades at 9.30 times earnings and yields 2.80%. Check my analysis of Exxon Mobil.

The thing to look for when evaluating energy companies is the reserve replenishment. Oil companies operate wells that will eventually run out of carbons, even if technologies are improved to a point where ALL the oil and gas in a well is pumped out. At some point, this well will stop producing income, and the company needs to move on. The reason why oil companies typically have low payout ratios is because they need to reinvest a portion of profits back into the business in order to find oil or buy assets they can develop.

I have looked at the data, and find that the idea behind peak oil is non-sense. The world is never going to run out of oil. That is, the world is never going to run out of oil during the lifetimes of anyone you meet today. The reason is that consumers will become more energy efficient, and companies will have an enormous incentive to explore and develop oil and gas fields in areas that are very difficult to drill in. The basic economic theory states that companies which see high energy prices will allocate funds at areas that are tough to explore and that make sense if oil stays at high levels for extended periods of time.

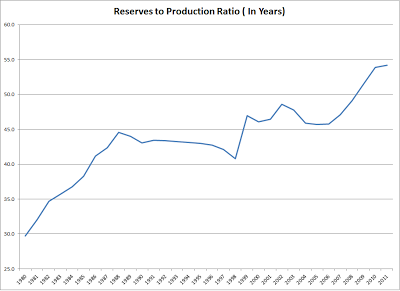

Over the past 30 years, the reserve to production ratio has remained above 40 - 50 years. This ratio shows the total amount of estimated oil reserves dividend by the total amount of annual production. If no new oil reserves were discovered ever again, and the world continues to consume oil at the same rate as today, the world would run out of oil in 50 years. It looks like oil reserves have been increasing enough to satisfy future oil demand. Therefore, it looks that for the past 30 years, the world has had anywhere between 50 -54 years’ worth of oil on its disposal. Right now, we have enough oil for the next 50+ years. I am betting ( see below how) that the world would have sufficient oil reserves for next 40 - 50 years in 2020, 2030 and 2040.

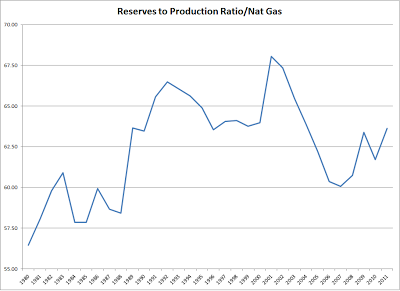

The same ratio for Natural Gas is over 60 years. The US is currently experiencing an energy renaissance particularly in such areas like Bakken Shale.

Companies are getting much better at forecasting where to drill for oil, and maximizing their chances of striking energy significantly. By using sophisticated seismic data, energy companies can obtain general reserve estimates for oil and gas wells. In addition, with improvements in technology, companies can now recover much more oil and gas out of the ground, compared to before. When the US experienced its first oil boom in the early 1900s, the primitive technology made it possible to only skim a portion of the oil in oil wells. As pressure in the oil and gas wells decreased, production fell in those wells, and they were then closed out. With improvements in technology however, it is now possible to increase the life of wells significantly, as it is much easier to get more out of each well.

One thing I do avoid is purchasing US oil and gas trusts. While they offer mouthwatering yields today, they are all destined to go to zero. This is because when these trusts were setup, their revenues are set to be generated from a fixed portfolio of assets. They cannot purchase new wells to earn revenue off of, and cannot drill for oil or gas. Even with improvements in technology, chances are that the wells you own will eventually dry up. As a result, the reason why these trusts offer such high yields is because they are essentially returning a huge portion of investor’s capital back. If investors reinvest a portion of these distributions in other oil and gas producing wells, they can extend their income stream. If investors instead spent all of their distributions, then they will not do well in a typical 30 year retirement scenario. BP Prudhoe Bay (BPT) is an example of an oil trust that will go to zero by 2025- 2030. This is the time when the oil royalties will no longer result in distributions, due to costs, declines in production, even if oil went to $200/barrel.

So what is the risk to my theory? If prices rise above a certain threshold, it might be economical for alternative energy sources such as solar and wind to be priced at par with oil and gas. However, oil would still be relevant 100 years from now even if it no longer were used for energy, because it is used in so many other aspects in everyday life such as chemicals, plastics etc.

Another risk is if the data I am using to base my assumptions is incorrect. The amount in proved reserves is simply an estimate. Actuals could turn out to be much different than estimates. In addition, just because there are proven oil reserves to last for 50 years however, there is no guarantee that all the oil will be available to be pumped out within 50 years, even if estimates were correct. On the positive side however, the reserves to production ratio does not account for undeveloped reserves. With the majority of the world's surface being under water, chances are that high enough oil and gas prices will one day incentivize exploration in the deep sea areas of the globe.Those areas could potentially provide for an almost unlimited amount of energy.

Full Disclosure: Long CVX, COP, RDS/B, KO

I find some of the cheapest stocks in the market today to be oil companies. I own stock in the following three oil companies:

Chevron Corporation (CVX), through its subsidiaries, engages in petroleum, chemicals, mining, power generation, and energy operations worldwide. The company trades at 9.20 times earnings and yields 3.30%. This dividend champion has increased distributions for 26 years in a row and has achieved a ten year average annual dividend growth of 9.60%. Check my analysis of Chevron Corporation.

ConocoPhillips (COP, Financial) explores for, produces, transports, and markets crude oil, bitumen, natural gas, liquefied natural gas, and natural gas liquids on a worldwide basis. The company trades at 10.10 times earnings and yields 4.20%. This dividend achiever has increased distributions for 12 years in a row and has achieved a ten year average annual dividend growth of 15.10%.Check my analysis of ConocoPhillips.

Royal Dutch Shell plc (RDS.B, Financial) operates as an independent oil and gas company worldwide. The company trades at 8.20 times earnings and yields 5.30%. The company ended a 16 year streak of consecutive dividend increases in 2010 by keeping distributions flat, only to start increasing them again in 2012. Check my analysis of Royal Dutch Shell.

I also used to own Exxon Mobil (XOM, Financial), but I replaced it with ConocoPhillips. Exxon is the largest oil company in the world. It engages in the exploration and production of crude oil and natural gas, and manufacture of petroleum products. The company trades at 9.30 times earnings and yields 2.80%. Check my analysis of Exxon Mobil.

The thing to look for when evaluating energy companies is the reserve replenishment. Oil companies operate wells that will eventually run out of carbons, even if technologies are improved to a point where ALL the oil and gas in a well is pumped out. At some point, this well will stop producing income, and the company needs to move on. The reason why oil companies typically have low payout ratios is because they need to reinvest a portion of profits back into the business in order to find oil or buy assets they can develop.

I have looked at the data, and find that the idea behind peak oil is non-sense. The world is never going to run out of oil. That is, the world is never going to run out of oil during the lifetimes of anyone you meet today. The reason is that consumers will become more energy efficient, and companies will have an enormous incentive to explore and develop oil and gas fields in areas that are very difficult to drill in. The basic economic theory states that companies which see high energy prices will allocate funds at areas that are tough to explore and that make sense if oil stays at high levels for extended periods of time.

Over the past 30 years, the reserve to production ratio has remained above 40 - 50 years. This ratio shows the total amount of estimated oil reserves dividend by the total amount of annual production. If no new oil reserves were discovered ever again, and the world continues to consume oil at the same rate as today, the world would run out of oil in 50 years. It looks like oil reserves have been increasing enough to satisfy future oil demand. Therefore, it looks that for the past 30 years, the world has had anywhere between 50 -54 years’ worth of oil on its disposal. Right now, we have enough oil for the next 50+ years. I am betting ( see below how) that the world would have sufficient oil reserves for next 40 - 50 years in 2020, 2030 and 2040.

The same ratio for Natural Gas is over 60 years. The US is currently experiencing an energy renaissance particularly in such areas like Bakken Shale.

Companies are getting much better at forecasting where to drill for oil, and maximizing their chances of striking energy significantly. By using sophisticated seismic data, energy companies can obtain general reserve estimates for oil and gas wells. In addition, with improvements in technology, companies can now recover much more oil and gas out of the ground, compared to before. When the US experienced its first oil boom in the early 1900s, the primitive technology made it possible to only skim a portion of the oil in oil wells. As pressure in the oil and gas wells decreased, production fell in those wells, and they were then closed out. With improvements in technology however, it is now possible to increase the life of wells significantly, as it is much easier to get more out of each well.

One thing I do avoid is purchasing US oil and gas trusts. While they offer mouthwatering yields today, they are all destined to go to zero. This is because when these trusts were setup, their revenues are set to be generated from a fixed portfolio of assets. They cannot purchase new wells to earn revenue off of, and cannot drill for oil or gas. Even with improvements in technology, chances are that the wells you own will eventually dry up. As a result, the reason why these trusts offer such high yields is because they are essentially returning a huge portion of investor’s capital back. If investors reinvest a portion of these distributions in other oil and gas producing wells, they can extend their income stream. If investors instead spent all of their distributions, then they will not do well in a typical 30 year retirement scenario. BP Prudhoe Bay (BPT) is an example of an oil trust that will go to zero by 2025- 2030. This is the time when the oil royalties will no longer result in distributions, due to costs, declines in production, even if oil went to $200/barrel.

So what is the risk to my theory? If prices rise above a certain threshold, it might be economical for alternative energy sources such as solar and wind to be priced at par with oil and gas. However, oil would still be relevant 100 years from now even if it no longer were used for energy, because it is used in so many other aspects in everyday life such as chemicals, plastics etc.

Another risk is if the data I am using to base my assumptions is incorrect. The amount in proved reserves is simply an estimate. Actuals could turn out to be much different than estimates. In addition, just because there are proven oil reserves to last for 50 years however, there is no guarantee that all the oil will be available to be pumped out within 50 years, even if estimates were correct. On the positive side however, the reserves to production ratio does not account for undeveloped reserves. With the majority of the world's surface being under water, chances are that high enough oil and gas prices will one day incentivize exploration in the deep sea areas of the globe.Those areas could potentially provide for an almost unlimited amount of energy.

Full Disclosure: Long CVX, COP, RDS/B, KO