As odd as it is to see an article pertaining to quarterly earnings on our site, I just couldn’t resist. National Oilwell Varco (NOV) has officially put up some pretty impressive numbers. On Oct. 25, 2013, the company reported that for the third quarter ending on Sept. 30, 2013, it earned a net income of $636 million ($1.49 per share). If we compare this to last quarter, which earned a net income of $531 million, we can see that in just one quarter NOV experienced almost a 20% increase in revenue. Even if we take away the $10 million in pre-tax transaction charges and the $102 million in pre-tax gains that are results from the settlement of an outstanding legal claim, net income has still increased almost 8%. Part of this is due to operating profit increasing 3% (to 15% of sales) for the quarter.

From a long term investor’s standpoint, that’s not the most impressive statistic that I took from the recent release. Most impressive to me is NOV’s constantly increasing backlog. As of Sept. 30, 2013, the company’s Rig Technology segment reached a record backlog level of $15.15 billion. This is a super impressive increase of 9% since the end of the second quarter of 2013, and a 30% increase from the same time last year (September 30, 2012). The company had $3.31 billion worth of new orders for the quarter, which represents over 21% of their backlog. This is mathematical proof of the strong demand for oilfield equipment.

Here’s what Pete Miller, chairman and CEO of National Oilwell Varco, had to say about the company’s most recent achievements:

“Outstanding execution enabled the Company to achieve solid results again this quarter. All three segments posted higher sequential revenues and margins, and collectively reduced the Company’s working capital requirements, which ultimately led to a quarterly record of $1 billion in cash flow from operations. We also added significant new bookings to our capital equipment backlog for the Rig Technology segment during the third quarter, as the industry’s demand for our suite of technologies remains strong.

We are excited about our recently announced plans to spin-off the Company’s distribution business from the remainder of the Company, creating two stand-alone, publicly traded corporations. We believe that the contemplated spin-off is very consistent with NOV’s strategy and commitment to continue to grow the Company and create significant shareholder value. As separate companies, the distribution business and the remainder of NOV will each be better positioned and have the enhanced operational flexibility to focus on their specific products, services and customers.”

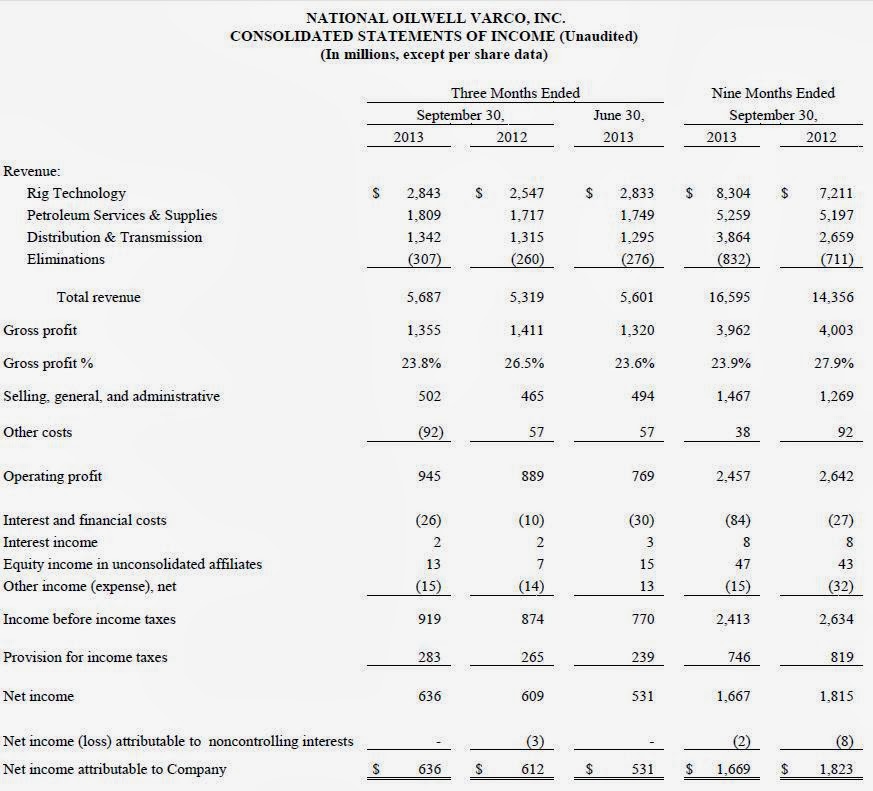

Here is the recent quarterly comparison of consolidated statements of income.

The share price for NOV has increased 13% since my previous, and very brief, article about the company was written on Aug. 27, 2013. I believe that with the increasing demand for NOV’s services, as well as the impressive management, the company is poised for more. What are your thoughts? What do these impressive results mean to you?

End Notes

Disclosure: Currently long NOV.

Disclaimer: The opinions and ideas in this article are for informational and educational purposes only. They are not a recommendation to buy or sell any stock at any given time. As always, it is imperative for each individual investor to do their own due diligence and perform their own research on any and all stocks before making an investment decision.

From a long term investor’s standpoint, that’s not the most impressive statistic that I took from the recent release. Most impressive to me is NOV’s constantly increasing backlog. As of Sept. 30, 2013, the company’s Rig Technology segment reached a record backlog level of $15.15 billion. This is a super impressive increase of 9% since the end of the second quarter of 2013, and a 30% increase from the same time last year (September 30, 2012). The company had $3.31 billion worth of new orders for the quarter, which represents over 21% of their backlog. This is mathematical proof of the strong demand for oilfield equipment.

Here’s what Pete Miller, chairman and CEO of National Oilwell Varco, had to say about the company’s most recent achievements:

“Outstanding execution enabled the Company to achieve solid results again this quarter. All three segments posted higher sequential revenues and margins, and collectively reduced the Company’s working capital requirements, which ultimately led to a quarterly record of $1 billion in cash flow from operations. We also added significant new bookings to our capital equipment backlog for the Rig Technology segment during the third quarter, as the industry’s demand for our suite of technologies remains strong.

We are excited about our recently announced plans to spin-off the Company’s distribution business from the remainder of the Company, creating two stand-alone, publicly traded corporations. We believe that the contemplated spin-off is very consistent with NOV’s strategy and commitment to continue to grow the Company and create significant shareholder value. As separate companies, the distribution business and the remainder of NOV will each be better positioned and have the enhanced operational flexibility to focus on their specific products, services and customers.”

Here is the recent quarterly comparison of consolidated statements of income.

The share price for NOV has increased 13% since my previous, and very brief, article about the company was written on Aug. 27, 2013. I believe that with the increasing demand for NOV’s services, as well as the impressive management, the company is poised for more. What are your thoughts? What do these impressive results mean to you?

End Notes

Disclosure: Currently long NOV.

Disclaimer: The opinions and ideas in this article are for informational and educational purposes only. They are not a recommendation to buy or sell any stock at any given time. As always, it is imperative for each individual investor to do their own due diligence and perform their own research on any and all stocks before making an investment decision.