Stock News

Categories

- All

- Editor's Picks

- Stock Market News

- Q&A with Gurus

- Gurus' Stock Picks

- Insider Transaction

- Earning Reports

- CEO Shareholder Letters

- Press Release

- Earnings Call Transcripts

- Instant Alerts

- Podcast

Industries

- Aerospace & Defense

- Agriculture

- Asset Management

- Banks

- Beverages - Alcoholic

- Beverages - Non-Alcoholic

- Biotechnology

- Building Materials

- Business Services

- Capital Markets

- Chemicals

- Conglomerates

- Construction

- Consumer Packaged Goods

- Credit Services

- Diversified Financial Services

- Drug Manufacturers

- Education

- Farm & Heavy Construction Machinery

- Forest Products

- Furnishings, Fixtures & Appliances

- Hardware

- Healthcare Plans

- Healthcare Providers & Services

- Homebuilding & Construction

- Industrial Distribution

- Industrial Products

- Insurance

- Interactive Media

- Manufacturing - Apparel & Accessories

- Media - Diversified

- Medical Devices & Instruments

- Medical Diagnostics & Research

- Medical Distribution

- Metals & Mining

- Oil & Gas

- Other Energy Sources

- Packaging & Containers

- Personal Services

- Real Estate

- REITs

- Restaurants

- Retail - Cyclical

- Retail - Defensive

- Semiconductors

- Software

- Steel

- Telecommunication Services

- Tobacco Products

- Transportation

- Travel & Leisure

- Utilities - Independent Power Producers

- Utilities - Regulated

- Vehicles & Parts

- Waste Management

Clean Energy Stocks Tumble on Solar, Wind Credit Repeal

Enphase and AES lead losses after Trump orders tighter renewables rules. 1 hours ago

Boeing Revives China Deliveries

China resumption fuels Boeing's best month since last summer 1 hours ago

Paramount-Skydance Merger Extension Kicks In as Trump Lawsuit Clears

The extension follows Paramount's $16 million settlement with Trump over a 60 Minutes dispute. 2 hours ago

Palantir Hits Back at UK Doctors in NHS Data Fight

MPs raised concerns about the company's military ties, data handling, and compatibility with NHS values. 2 hours ago

Hershey Names Wendy's CEO Kirk Tanner as New Chief Executive

Michele Buck, Hershey's current CEO, will step down after more than seven years in the role. 2 hours ago

Goldman, BofA Lift S&P 500 Targets Again

Strong profits, fading rate fears and dividends underpin the rally. 2 hours ago

Retail - Cyclical

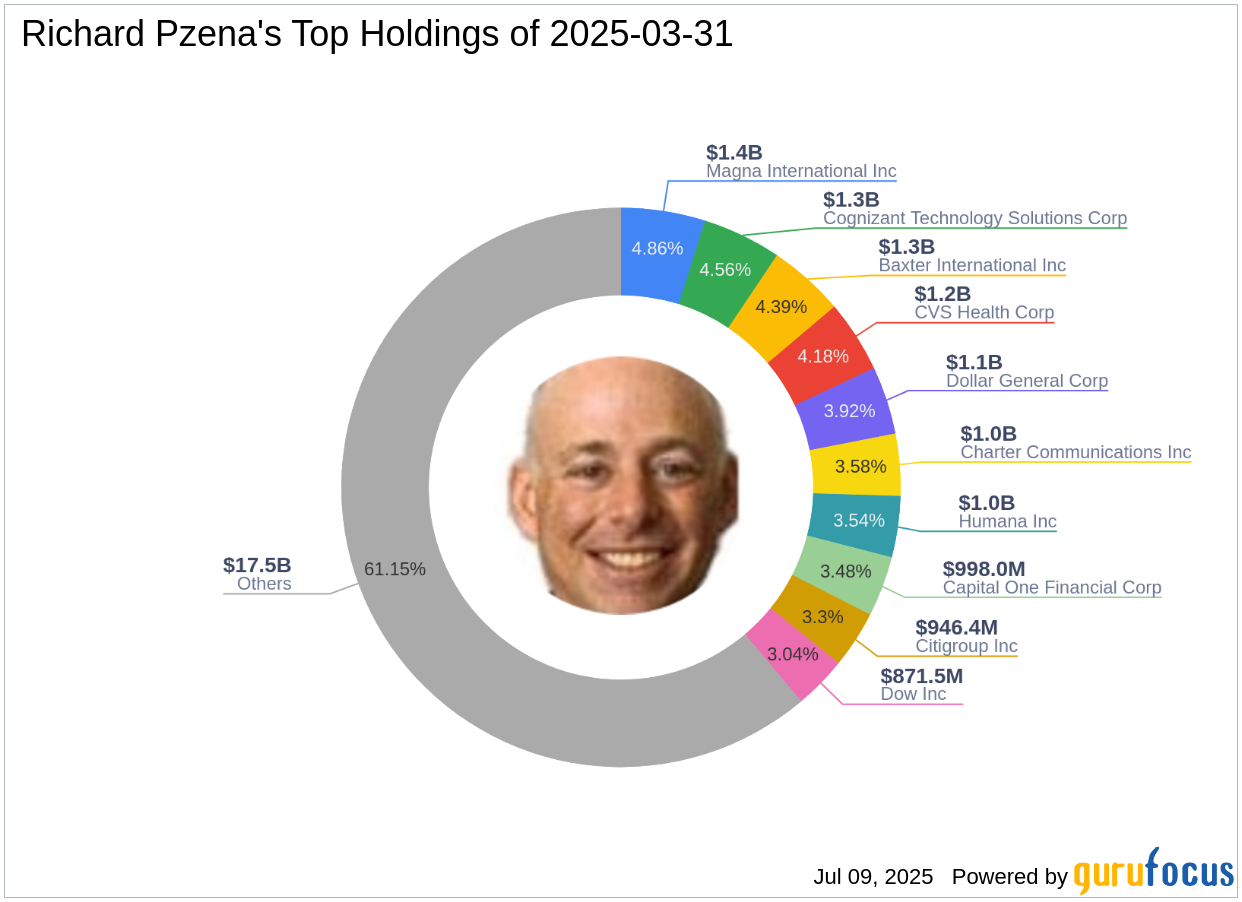

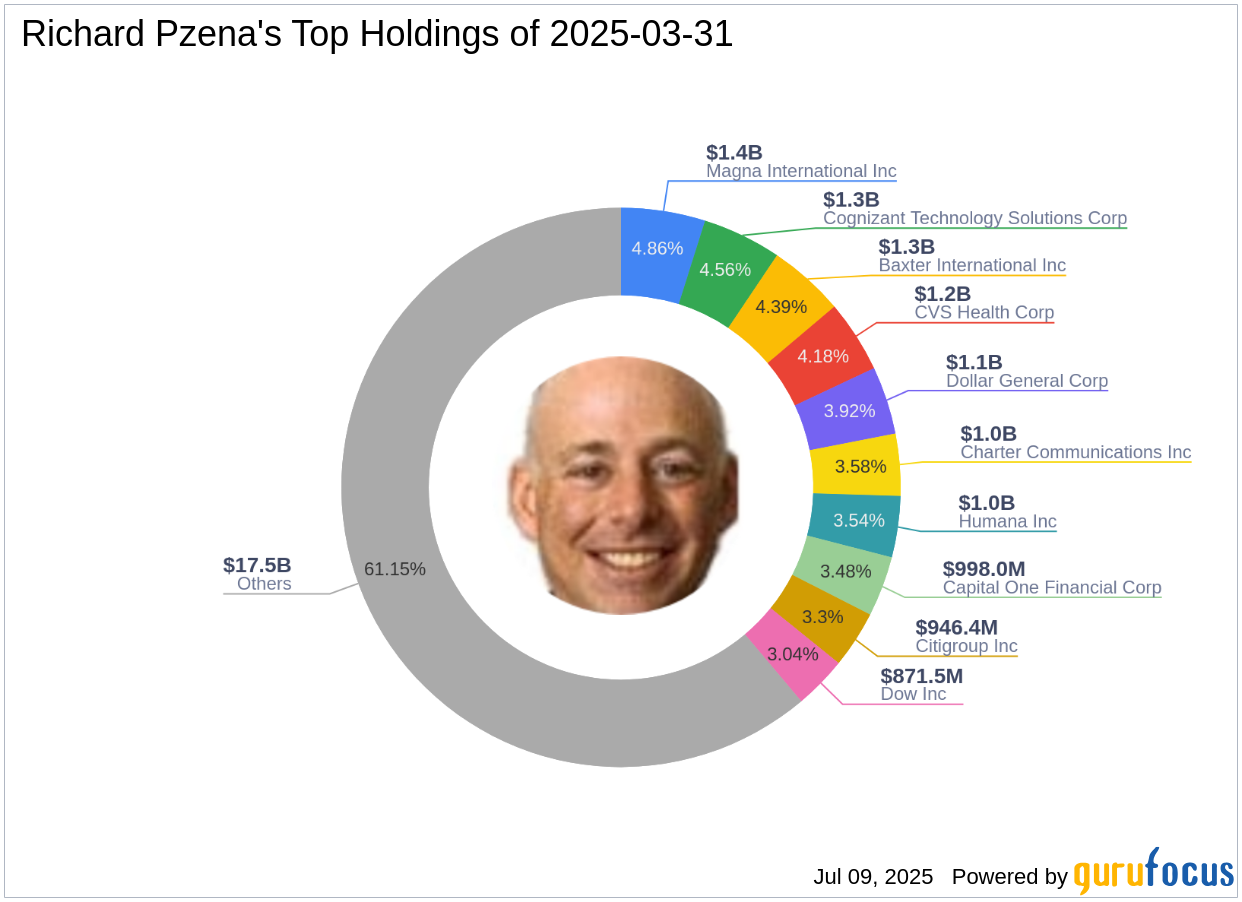

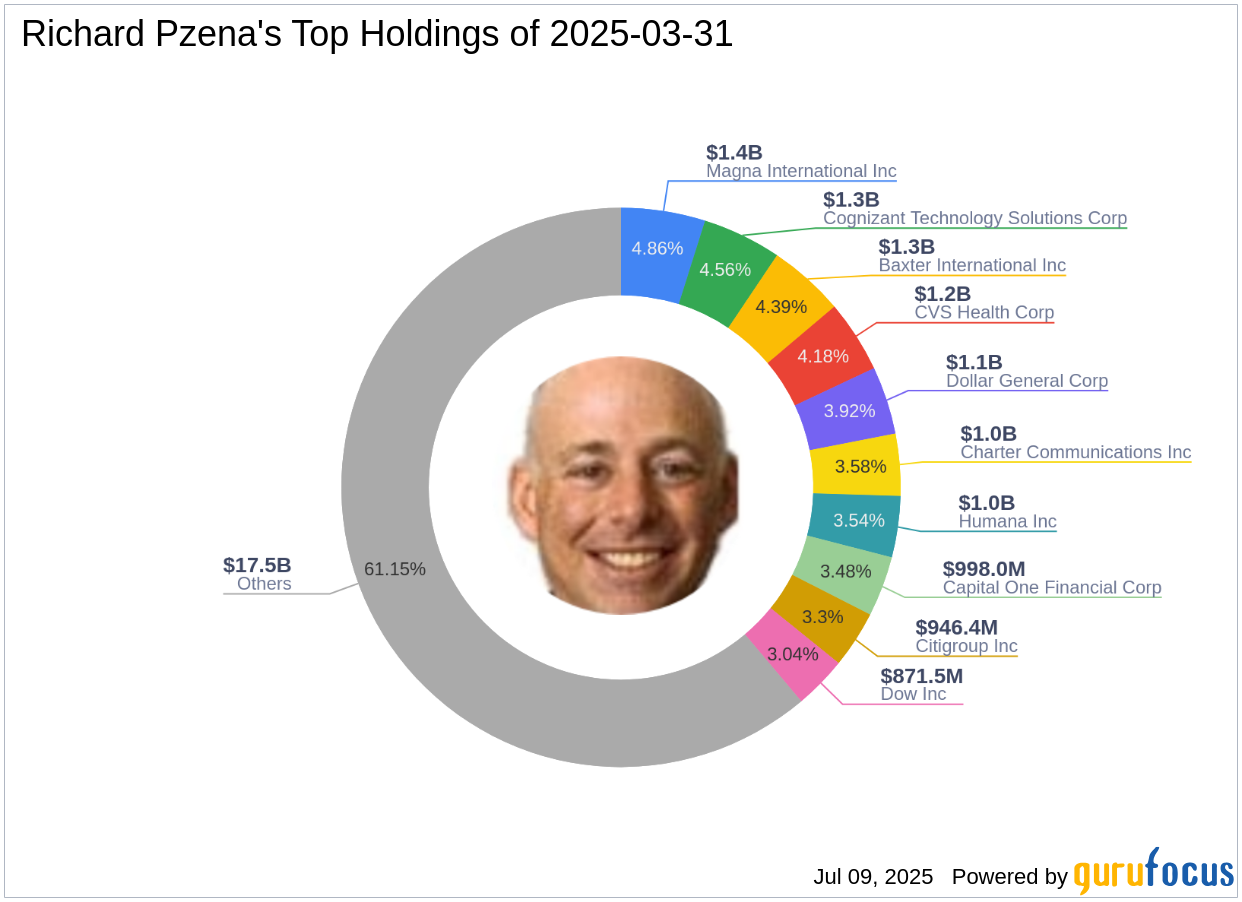

Richard Pzena's Strategic Acquisition in Haverty Furniture Companies Inc

9 hours ago

Medical Devices & Instruments

Richard Pzena's Strategic Acquisition in Varex Imaging Corp

9 hours ago

Farm & Heavy Construction Machinery

Richard Pzena's Strategic Acquisition of The Shyft Group Inc Shares

9 hours ago

Solar Stocks Plunge as Trump Tightens Green Energy Tax Perks

Green Energy Selloff Deepens as Trump Moves to Cut Subsidies 15 hours ago ★★★★☆

Metaplanet Eyes Digital Bank as Bitcoin Reserves Top 15,000 BTC

Metaplanet now holds 15,555 BTC and plans to acquire cash-generating businesses. 15 hours ago

Why HSBC Is Betting Billions on Britain's Rich--Just as They Start to Flee

The bank is launching 50 wealth hubs and hiring 200 bankers--even as the UK's wealthiest pack their bags. 15 hours ago

Joby Aviation Shares Take Off on Middle East Progress

Dubai Milestone Propels Joby Shares to New Heights 15 hours ago

Trump's ?Big Beautiful Bill? Could Boost Bitcoin, Analysts Say

Trump's new budget raises the U.S. debt ceiling by $5 trillion but includes no direct crypto reforms. 15 hours ago

Tether's $8B Secret Gold Vault Revealed--And Why It Could Spark a Crypto Showdown

As regulators crack down on stablecoins, Tether doubles down on gold in a bold move that's raising eyebrows worldwide. 15 hours ago

Apple's Top AI Executive Ruoming Pang Departs for Meta's Superintelligence Team

Apple AI leader Ruoming Pang has left the company to join Meta. 15 hours ago

Manufacturing - Apparel & Accessories

Key Companies Benefiting from the 2025 Club World Cup

17 hours ago

Survey

We'd love to learn more about your experiences on GuruFocus.com and how we can improve!

Take Survey

Follow Us

Disclaimers