My previous articles on the pension footnote was well received from the readers. This gives me enormous courage and motivation to write more about the footnote disclosures of other less understood areas. This article is an attempt to explain the maths behind the potential dilutive effects of stock awards related to the share-based compensation footnote disclosure.

One of the hidden perils in common stock investing is the potential of massive dilution from share based compensation awarded to management. The most common forms include stock options, stock appreciation rights, restricted stock units (RSU), and restricted stock awards (RSA).

An incomplete understanding of the aforementioned share based compensation awards and their dilutive effects could pose a great threat to an investor’s return in the common equity. In this article, I will share with the readers the system that I use to assess the dilutive effects of stock options and restricted stocks.

I assume most readers should be familiar with the concept of stock options and how they work. However, RSUs and RSAs may sound not as familiar as stock options.Essentially both RSUs and RSAs are compensation offered by a company to its employees in the form of the company stocks according to a vesting plan and distribution schedule after achieving required performance milestones (performance based) or upon satisfying the minimum service period requirement (service based). The main difference between RSU and RSA is whether the company issues stock at the time of grant.

Let me use Colgate-Palmolive Company (CL, Financial) as an example to illustrate the dilution calculation. Before proceeding further, I want to clarify that this calculation is an estimate so you may not get the most accurate result as you would like to. Regardless, I think the following calculation will give you a good educated guess.

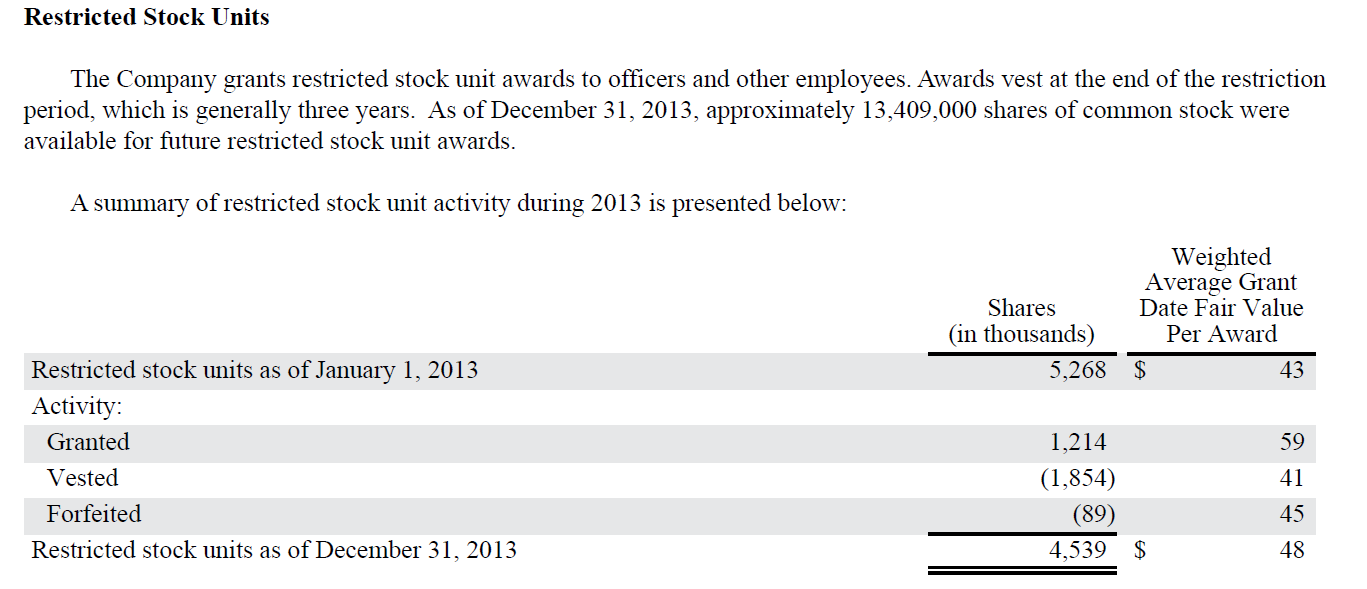

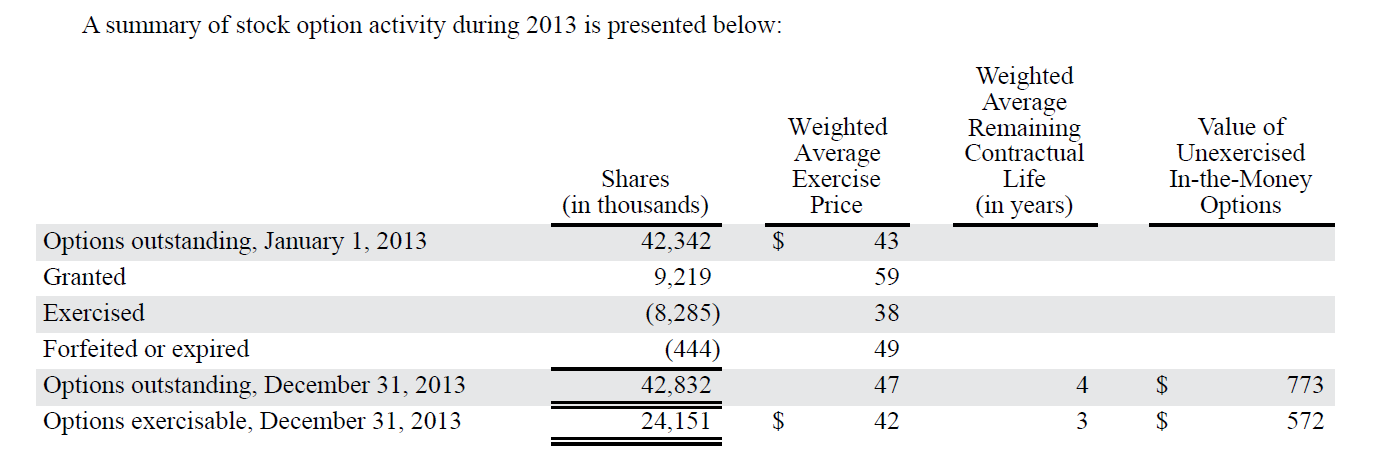

Below are excerpts from the 2013 annual report of the Colgate-Palmolive Company.

Â

A common mistake I have observed is that an investor often takes the shares of options and RSUs outstanding as the potential dilutive shares. This ignores the facts that

1. Compensation expenses are tax deductible, which generate cash savings.

2. The company will receive cash for option exercise and they can use it to buy back shares.

The formula I use to calculate the potential dilution is as follows:

Again, these are educated guesses as we don’t know the real value of the restricted shares and exercise price of the options.

You can tell that if you don’t do the calculation and just add up options and restricted units outstanding, you will get a massive dilution of 47,371,000 shares. With our arguably good enough calculation, the dilution is only 16,174,730 shares, or roughly â…” lower.

Now it’s your time to try it on some technology companies.