The global e-commerce market is growing and large. Borderfree, Inc. (NASDAQ:BRDR) provides solutions to simplify the international shopping process. It offers a most comprehensive global cross-border e-commerce platform. Its customers consist of top retailers and brands, including Macy's, J Crew, Under Armour, Sephora, etc. In fact, less than 60% of retailers sell internationally. As they move to global e-commerce, BRDR can offer turn-key solutions and proven business model to increase customer sales. The difficulties retailers have to face if they chose to do e-commerce themselves without the help of BRDE are listed below:

(click to enlarge)

Source: Company Presentation

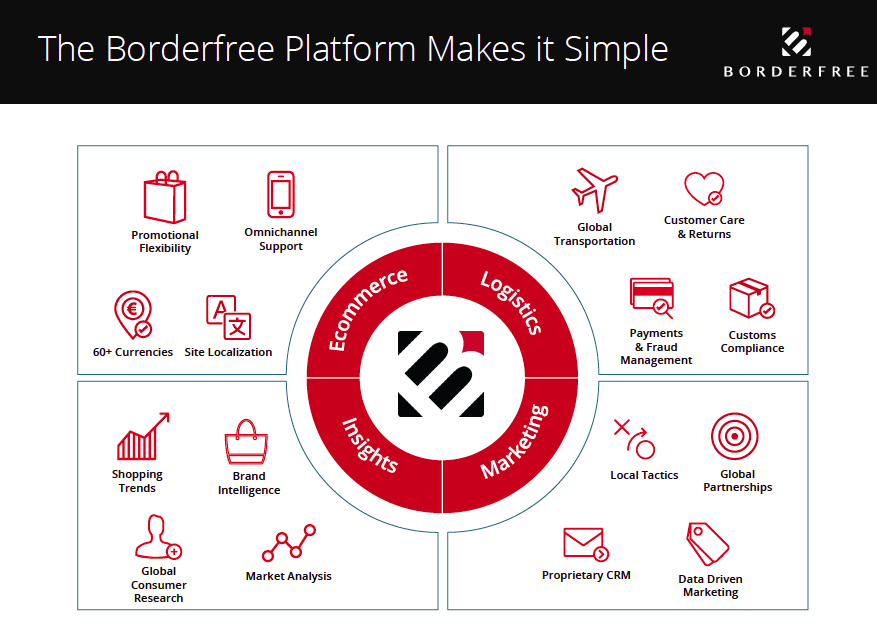

Since dealing with global e-commerce is complicated, this provides a great business opportunity for BRDR to offer retailers a simple solution with detail below:

(click to enlarge)

Source: Company Presentation

In another word, BRDR helps its clients to convert products into the local currencies. Plus BRDR bears the fraud risk by accepting and processing payments. Lastly, BRDR handles the international fulfillment process for its clients. This poses accounting regulatory requirements, taxes, tariffs and other inherited risks. To compensate for the risks, BRDR charges approximately 14% for its global e-commerce platform to account for the foreign exchange risk, together with handling and processing of products globally.

I believe BRDR has first mover advantage to explore the global e-commerce market by offering a platform. As the global e-commerce is forecasted to rise, the future potential of BRDR cannot be underestimated. Currently, BRDR is just a $340 million market cap business with around $95 million in net cash. The net cash gives financial flexibilities to BRDR. Plus, the market cap of BRDR is very small relative to the global e-commerce business opportunity. Therefore, I believe that BRDR is a asymmetric risk/reward profile investment.

Financial strengths

With $95 million net cash relative to $340 million market cap, it is undeniable that BRDR has pristine balance sheet.

Business strengths

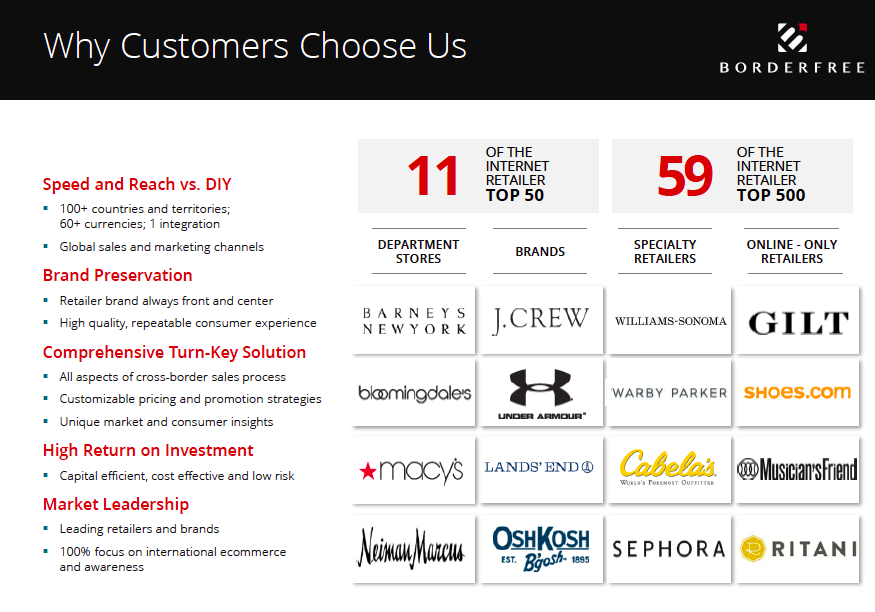

(click to enlarge) Source: Company Presentation

Source: Company Presentation

Despite being a small cap company, BRDR has eleven of the internet retailer TOP 50 as customers. In addition, BRDR has 59 of the internet retailer TOP 500 as customers. Relative to its competitors, BRDR has much more exposure to TOP customers. That's why BRDR is the leader in the global ecommerce platform, and this advantage should warrant a premium for BRDR valuation.

Valuation

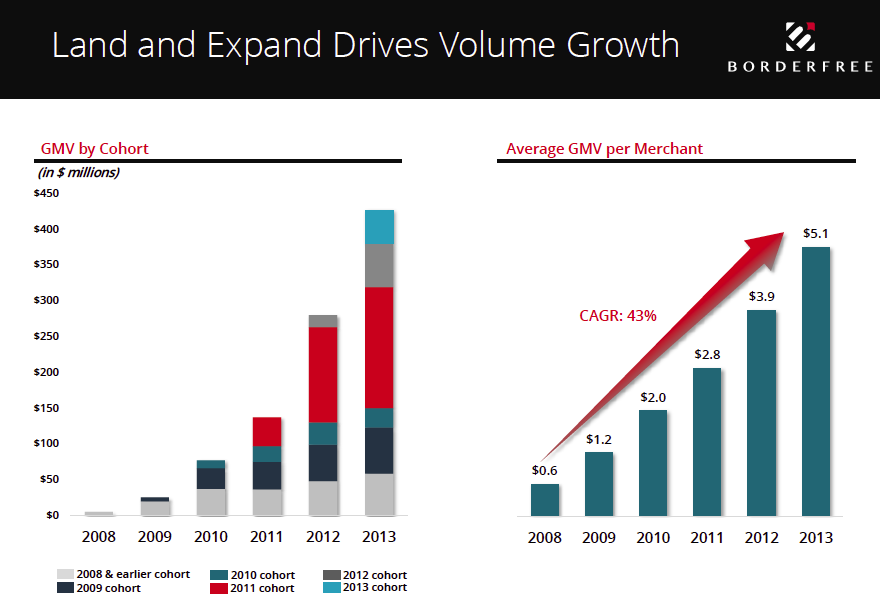

When we consider the valuation of BRDR, we have to assess the potential large market opportunity in the global e-commerce market. What's more, BRDR achieved 79% e-commerce revenue CAGR between 2011 and 2013, together with high e-commerce revenue retention rate.

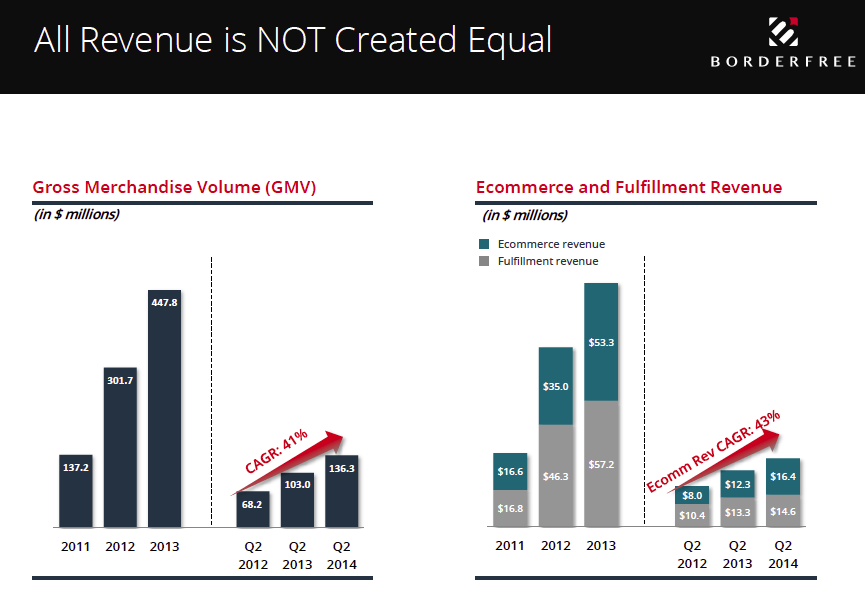

(click to enlarge)

(click to enlarge)

Source: Company Presentation

As shown above, BRDR consistently grew its Gross Merchandise Volume "GMV" from $137 million in 2011 to $447 million in 2013. In addition, BRDR has demonstrated its capabilities to grow its e-commerce and fulfillment revenues from $33 million in 2011 to $110 million in 2013. If we look further into the details, BRDR has been actively managing its average GMV per merchant, which increased from $0.6 GMV per merchant to $5.1 GMV per merchant.

| Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | Stabilized Yr. |

| Year | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 |

| Sales | 134.07 | 154.18 | 177.30 | 203.90 | 234.48 | 269.66 | 310.11 | 356.62 | 410.11 | 471.63 | 495.21 |

| EBITDA | 10.73 | 12.33 | 15.96 | 18.35 | 23.45 | 26.97 | 37.21 | 42.79 | 53.31 | 66.03 | 74.28 |

| EBIT | 7.37 | 8.48 | 11.52 | 13.25 | 17.59 | 20.22 | 29.46 | 33.88 | 43.06 | 54.24 | 61.90 |

| Net Income | 4.88 | 5.61 | 7.61 | 8.75 | 11.58 | 13.32 | 19.35 | 22.25 | 28.26 | 35.56 | 40.56 |

| EBIT x (1 - Tax Rate) | 4.79 | 5.51 | 7.49 | 8.61 | 11.43 | 13.15 | 19.15 | 22.02 | 27.99 | 35.25 | 40.24 |

| - Capital Expenditure | 4.02 | 4.63 | 5.32 | 6.12 | 7.03 | 8.09 | 9.30 | 10.70 | 12.30 | 14.15 | 14.86 |

| + Depreciation & Amortization | 3.35 | 3.85 | 4.43 | 5.10 | 5.86 | 6.74 | 7.75 | 8.92 | 10.25 | 11.79 | 12.38 |

| - Change in Noncash Working Capital | 7.25 | (1.21) | (1.39) | (1.60) | (1.84) | (2.11) | (2.43) | (2.79) | (3.21) | (3.69) | (1.41) |

| Adjusted Free Cash Flow | (3.12) | 5.95 | 7.99 | 9.19 | 12.09 | 13.91 | 20.03 | 23.03 | 29.15 | 36.59 | 39.17 |

| FREE CASH FLOW (FCFF) VALUATION MODEL | Â |

| Present Value of Free Cash Flow | $83 |

| Present Value of Terminal Value | $438 |

| Value of Operating Assets | $522 |

| Value of Cash, Marketable Securities & Non-operating assets | $121 |

| Value of the Firm | $642 |

| Value of Debt | $2 |

| Value of Common Equity | $640 |

| Value of Common Equity Per Share | $20.30 |

It is rare to find any company with the potential to double. BRDR is one of the companies capable of delivering such an outstanding return. According to my DCF model, I assume that the revenues will grow by approximately 15% per year for the next 10 years, and I discount the future cash flow at 8.8% weighted average cost of capital. At first glance, the sales growth might be an aggressive assumption. But given the long-term growth rate for retailers subscribing to BRDR's global e-commerce platform, BRDR should be able to deliver such high growth rate for a long period of time. In addition, BRDR has a volume-based business model. As more and more retailers sign up onto the BRDR platform, the profit margins of BRDR will disproportionally increase. With the expected high profit margins and strong revenue growth, BRDR should be worth as much as almost twice its current value.

Management team

Michael DeSimone has been the CEO of BRDR since 2007. He has more than 20 years of foreign exchange and cross-broder payment experience at leading global financial institutions. As foreign exchange risk is one of the major risks of doing global e-commerce, Michael's expertise in foreign exchange is critical for the success of BRDR. In the past, Michael DeSimone held senior management roles in Travelex, Citibank, and Thomas Cook Financial Services. In addition, his regular appearance on top news organizations, including CNBC, FOX, Bloomberg and Women's Wear Daily, shows his importance and influence in the industry.

Ed Neumann has been the CFO of BRDR since 2010. He had more than 20 years of experience in finance and operations. He spent a decade at Charming Shoppes Inc, a leading multi-brand, multi-channel apparel retailer. According to his biography on the Borderfree website, Ed was instrumental in transitioning Charming Shoppe's e-commerce business into a fast growing and highly profitable operation.

Brian Dhatt has been the chief technology officer of BRDR since March 2013. I noticed that Brian had working experience in the Gilt City of Gilt Groupe, an online retailer of discounted luxury goods. I am also impressed by the fact that Brian led the platform and brand in Gilt City to scale for extreme traffic within an award-winning user experience. Brian also had experience in founding Sugar, Inc and served as the chief architect of Bestbuy.com.

Overall, the management team consists of many well-qualified senior members to run BRDR in my opinion.

Risks

First, since BRDR deals with global e-commerce, it faces foreign currency risk. If foreign currency rate goes against BRDR, BRDR might incur adverse impact on its probabilities. Second, BRDR faces high customer concentration risk. Third, the business of BRDR is global e-commerce. Therefore, it is subject to the global economic health and customer spending. But the good news is that as BRDR has a high probability to expand its global footprints in future, it can become much more geographically diversified. Forth, BRDR faces the risk of insourcing and loss clients to its competitors. Some of BRDR's clients might choose to invest in their own e-commerce global platform or join other third-party platform venders instead of BRDR. As the industry is evolving rapidly and BRDR is still a small-cap company, there is high uncertainty related to investment in BRDR. Therefore, BRDR is more suitable for investors with high risk tolerance. Fifth, as both Home Depot (NYSE:HD) and Target (NYSE:TGT) face security breach issues, BRDR should not be immune to potential security issues in the future as BRDR has BRDR account profile for consumers to log into their personal accounts with saved credit card information and mailing address. However, the positive side is that the BRDR personal accounts are very useful for analyzing how to do target marketing in the future, and the accounts can be very valuation asset for BRDR in the future.

The bottom line

The future prospects of BRDR are bright. I believe global e-commerce should enjoy a high growth rate for the forseeable future. BRDR is the company for investors to capitalize on this trend. As technology changes rapidly, it is difficult to predict whether there might be any future competitors with better technology to replace BRDR. However, given all the information we have as of today, such a scenario seems to have a low possibility. As I have already disclosed many risk factors in the risks section, I believe that BRDR is more suitable for investors with high risk tolerance despite the lucrative potential return to invest in BRDR.

Disclosure: I am not a securities broker/dealer or an investment adviser. You are responsible for your own investment decisions. All information contained should be independently verified with the companies mentioned, and readers should always conduct their own research and due diligence and consider obtaining professional advice before making any investment decision.