One of the hot political topics these days is income inequality, but one of the groups of Americans that’s the most mistreated by Washington, D.C., is the millions of Americans who have responsibly saved for their retirement.

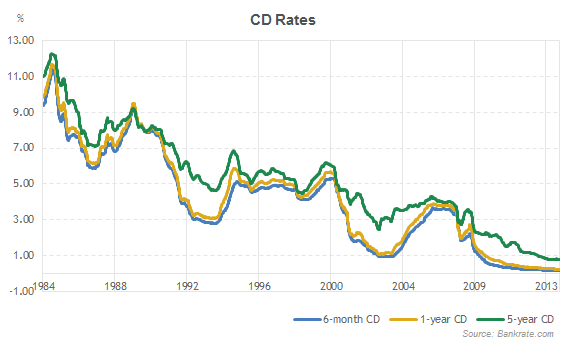

When I entered the investment business as a stock broker at Merrill Lynch in the 1980s, savers could routinely get 7-9% on their money with riskless CDs and short-term Treasury bonds.

In fact, I sold multimillions of dollars’ worth of 16-year zero-coupon Treasury bonds at the time. Zero-coupon bonds are debt instruments that don’t pay interest (a coupon) but are instead traded at a deep discount, rendering profit at maturity when the bond is redeemed for its full face value.

At the time, long-term interest rates were at 8%, so the zero-coupon Treasury bonds that I sold cost $250 each but matured at $1,000 in 16 years. A government-guaranteed quadruple!

Ah, those were the good old days for savers, largely thanks to the inflation-fighting tenacity of Paul Volcker, chairman of the Federal Reserve under Presidents Jimmy Carter and Ronald Reagan from August 1979 to August 1987.

Monetary policies couldn’t be more different under Alan “Mr. Magoo” Greenspan, “Helicopter” Ben Bernanke, and Janet Yellen. This trio of hear-see-speak-no-evil bureaucrats have never met an interest-rate cut that they didn’t like and have pushed interest rates to zero.

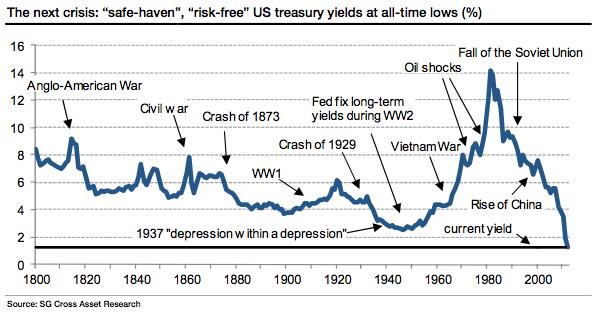

The yield on the 30-year Treasury bond hit an all-time record low last week at 2.45%. Yup, an all-time low that our country hasn’t seen in more than 300 years!

These low yields have made it increasingly difficult to earn a decent level of income from traditional fixed-income vehicles like money markets, CDs and bonds.

Unless you’re content with near-zero return on your savings, you’ve got to adapt to the new era of ZIRP (zero-interest-rate policy). However, you cannot just dive into the income arena and buy the highest-paying investments you can find. Most are fraught with hidden risks and dangers.

So to fully understand how to truly and dramatically boost your investment income, you absolutely must look at your investments in a new light, fully understanding the new risks as well as the new opportunities.

There are really two challenges that all of us will face as we transition from employment to retirement: longer life expectancies; and lower investment yields.

Risk #1: Improved health care and nutrition have dramatically boosted life expectancies for both men and women. We will all enjoy a longer, healthier life, which means more time to enjoy retirement and spend with friends/family, but it also means that whatever money we’ve accumulated will have to work harder as well as longer.

continue reading: https://www.mauldineconomics.com/connecting-the-dots/income-inequality-americans-savers-treated-like-dogs