Agrium Inc. (AGU, Financial) is a major U.S. retail operator and a wholesale fertilizer operation that serves farmers. In addition the company also operates a couple of hundred stores in Canada and Australia. The retail outfits sell the fertilizers in addition to other commodities required by farmers like crop chemicals and seeds. The fertilizer business is doing pretty well, but it should be taken into account that this is an even more cyclical business than the farming retail operation overall.

Financial state

The company has quite a bit of net debt –Â approximately $4.7 billion which it can serve with a TTM Ebitda of $1.7 billion. Only a small part of the debt is maturing in the next few years and the average interest rate of 5% is pretty low. The company also has a $2.2 billion of undrawn credit facility. It looks quite manageable, but there are safer companies out there from a risk perspective. Management is expecting to decrease the debt-to-EBITDA ratio in the coming year.

Management

Recently new management was installed. Chuck Magro, a company man, succeeded Michael Wilson as CEO in early 2014. Magro previously held the job of chief operating officer since 2012. Before that he held a number of roles at the company from executive vice president, corporate development, and chief risk officer to VP manufacturing. It will be hard to top Wilson as he managed to grow the company like a well fertilized weed. That said, Magro probably learned a thing or two from him and Wilson remains on the board. The company’s strategy and culture of making small acquisitions and integrating them well will probably continue to be executed. Using growth in book value over the past 10 years as a proxy to judge capital allocation skills Wilson definitely gets a thumbs up:

Risk

It is not yet possible to export liquid natural gas from the U.S. but a couple of companies are working hard to make it happen, like Cheniere Energy (LNG, Financial). Although a boon to the U.S. economy, this threatens the U.S. record low gas prices which is an important input for fertilizer companies. Without the low gas prices margins on fertilizer will decrease.

Farming is a cyclical business. When prices for crops are high, farmers rent out/buy and work more acres and when prices are low they scale back. The weather plays a large role in the supply/demand curve and all these uncertainties together make it tough to predict Agrium’s business. When prices for crops are low the company’s retail operation is likely to suffer and when they are high it will prosper. Low crop prices remain a threat.

Valuation

What is not immediately apparent when looking at the company’s EPS is that currently CapEx is elevated while cash flow is soon going to be lifted. The company is completing a ammonia facility refresh that should be done in the first quarter of 2016. The urea plant project should be done by the end of 2016. This cuts two ways and will improve FCF per share by a ton going forward. This is the main reason I was interested to take a closer look here. Management commented as follows on the earnings call:

We are committed to ensuring we deliver on our capital allocation vision and strategy, and as Chuck just discussed, we're willing to make difficult decisions if projects are not meeting return expectations. We expect our total capital expenditures to come in at our previous range of $1.2 billion to $1.3 billion for 2015, and $800 million to $900 million in 2016.

Using parts of managment guidance and in part my own (probably highly conservative) estimates I came up with a 2017 FCF model:

| Agrium Valuation 2017 | Â | Â | Â |

| $ million | Â | Â | Â |

| Â | Â | Â | Â |

| Revenue | 18000 | Forward estimate when Mooresboro is up and running (expected mid 2016) | |

| EBITDA | 2500 | Â | EBITDA margin |

| Less: interest expense | -160 | Â | Â |

| Less: Capital Expenditures | -800.0 | Â | Maintenance CapEx |

| Less: taxes | -300.0 | Â | Estimate based on effective tax rate last 10 years |

| Free cash flow | 1240 | Â | Â |

| Â | Â | Â | Â |

| Shares outstanding | 142 | Â | Â |

| Â | Â | Â | Â |

| Free cash flow per share | 8.7 | Â | Â |

| Â | Â | Â | Â |

| Â | Â | Â | Â |

| FCF Multiple | Â | Â | Â |

| 8 | 69 | Â | Â |

| 10 | 87 | Â | Â |

| 12 | 104 | Â | Â |

| 14 | 122 | Â | Â |

| 16 | 140 | Â | Â |

| Â | Â | Â | Â |

| Â | Â | Â | Â |

| Current Price | 97 | Â | Â |

| Upside | 7% | Â | Â |

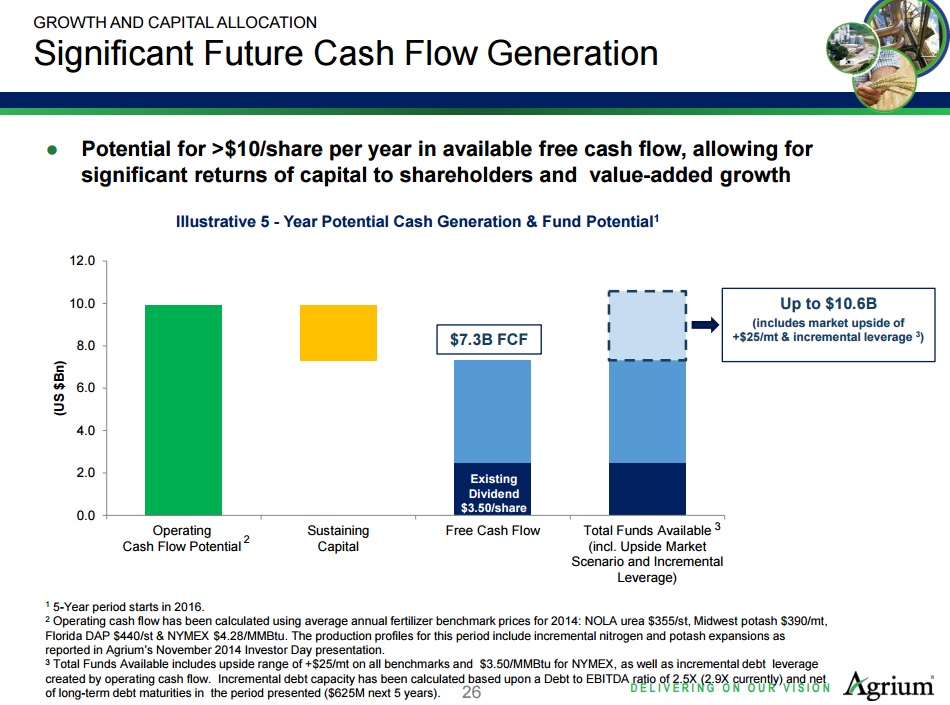

If these assumptions are ballpark right, the shares are about fairly valued or perhaps even a little bit overvalued. It is only fair though to also show you that the company’s management team is a lot more positive. In its roadshow management showed the slide below indicating its possible the company will achieve much higher FCF per share:

source: Company roadshow presentation

Outlook

The company bought back about a million shares recently and is expected to to buy back quite a few more shares. Increasing demand for calories, driven by a growing world population which is also slowly “upgrading” its diet to include more meat, should help Agrium continue to grow. The companies dense network of retail operations gives it an edge over small time competitors which enables it to slowly force them out or buy them up. As the firm continues to gain scale (there is still quite some runway ahead) this enhances its competitive advantage which should ultimately drive margins. That process is going to take a decade to truly move the share price and I have not banked on it in my model. For the true long-term investor, it is something to take into account.