The casual observer may conclude from Buffett’s continued buying of Phillips 66 (PSX, Financial) he is bullish on oil, but that’s not necessarily the case.

Phillips 66 is primarily a refiner with 14 facilities. Together these produce in excess of 2 million barrels every day. In addition the company owns a chemical joint venture, CPChem, 60-plus natural gas processing facilities and 62,000 miles of pipeline.

If you take a look at how Phillips 66's share price has developed over the past few years, you’ll see it isn’t as vulnerable to the oil downturn as many other companies in the space. It’s possible the oil collapse had a negative effect, but if it did, it only slowed Phillips 66 down:

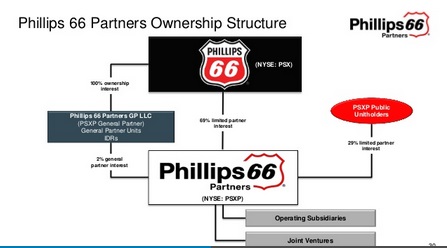

The first place I started looking to see if there was anything interesting there was the balance sheet. There are clues to what Buffett may see in the outfit, but ultimately I don’t think the balance sheet can fully explain his enthusiasm. What struck me as interesting was the fact that Phillips 66 also holds a 71% interest, including the general partner interest, in Phillips 66 Partners LP:

This stake is worth at least $3.3 billion, which translates to the value of 71% of the Phillips 66 Partners LP, but it is actually worth more due to the general partner interest.

A second interesting asset is the 62,000 miles of pipeline the company owns. I love asset valuations as it is a very simple way to demonstrate or show value present. My conservative but rough estimate is that the replacement value of the company’s network of pipelines is worth approximately $18.6 billion. That’s close to half of the company’s market cap. I got there by putting a replacement price of $300,000 on each mile of pipeline and multiplying it by the 62,000 miles owned. The figure comes from the Oil and Gas Journal, but it applies to 12-inch pipe, which is the smallest kind of pipeline the company owns in a large quantity. It also owns many miles of larger pipe, which are more expensive, but I wanted to keep my valuation conservative.

Unfortunately, I don’t have a good way to appropriately value the company’s core refinery assets or chemical company assets. I did work on valuing the company’s storage assets, but its capacity probably adds up to being worth a conservative $1 billion in total.

Capital allocation

What struck me as typical of a Buffett investment was the company’s emphasis on appropriate capital allocation and a strong emphasis on growing the existing dividend (about 2.8%) and buying back shares while making reinvestments into the business as well:

Over the last several years the company has attained very strong RoIC generally above 14% and up to 19%.

Phillips 66 is an independent refiner with 14 refineries with a total throughput capacity of 2.2 million barrels per day. Its DCP Midstream joint venture holds 61 natural gas processing facilities, 12 NGL fractionation plants and a natural gas pipeline system with 62,000 miles of pipeline. Its CPChem chemical joint venture operates facilities in the U.S. and the Middle East and primarily produces olefins and polyolefins. Phillips 66 also holds a 71% interest, including the general partner interest, in Phillips 66 Partners LP.

Success in refining is primarily a function of the difference in the amount the refiner pays for oil and the amount at which it sells the refined product. As such, the short- and long-term risks depend on movements in the prices of crude oil and gasoline. Supply interruptions or increased demand that drive up oil prices, as well as demand destruction or economic slowdowns that depress gas prices, are the primary risks.

Conclusion

Buffett is likely attracted to the company because of the valuable asset base that puts a floor under the company’s share price. Management’s emphasis is on prudent capital allocation and returning cash to shareholders but especially its stable cash flows from the refining business. Refineries effectively buy crude and sell refined oil so aren’t as vulnerable to low crude prices, but they are somewhat vulnerable to sudden swings in the price of oil. With the company just having experienced the big swing down, that risk has somewhat abated unless you expect much lower oil prices; the current cash flow is quite substantial with the company trading at 8x operating cash flow, 7.7x EV/EBITDA and a P/E of 8.8.

Phillips 66Â is not a great play if you think oil must go up and want to leverage that theory but it does have some upside exposure to a better oil environment while having the characteristics of a business that will survive throughout a prolonged commodity bear market.