Guru Mario Gabelli (Trades, Portfolio) just appeared on Fox News; in addition to his general outlook on the economy and the market, he also shared three investment ideas.

Gabelli thinks the economy is going to do well in the U.S. Consumer wealth is high, wages are rising, unemployment is low. The U.S. consumes a lot of oil and with oil at such a low price, there is a lot of spending power that is going to come in. He also expects Europe will start to do better. A summary of his expectation is a continued slow, moderate, sustainable recovery.

The volatility earlier in the year, he explained, was due to concern about the impact of energy and mining combined with weakish consumer numbers. Prolific analysts were coming out and calling a recession. Things just came together to cause a drop. That’s how public markets should work.

Gabelli really likes the defense sector, health and wellness, water and content and its distribution. From the defense industry he offers up three specific picks:

Honeywell

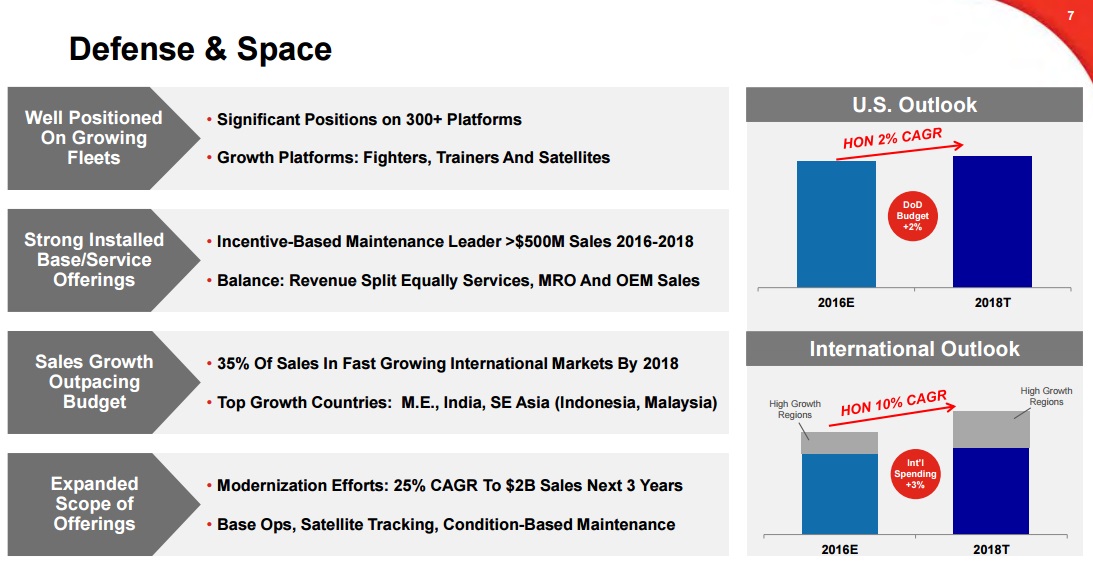

Gabelli really likes the defense sector because the U.S. military has underspent recently. It is an obvious play to him. Honeywell (HON, Financial) is a prolific choice within the sector. The $86 billion behemoth trades at an EV/EBITDA of 11.8x, and it has a safe balance sheet with a modest net debt load of just $5 billion. The company indeed expects to do well in the Defense & Space segment; see the slide from the company’s most recent investor presentation below, showing the outlook for the Defense & Space segment:

(Source: company presentation)

The only problem with this pick is that the defense industry is maybe good for one-eighth or so of the company’s revenue. If you have a high conviction on the industry, you are diluting that idea a lot.

Kaman Corp.

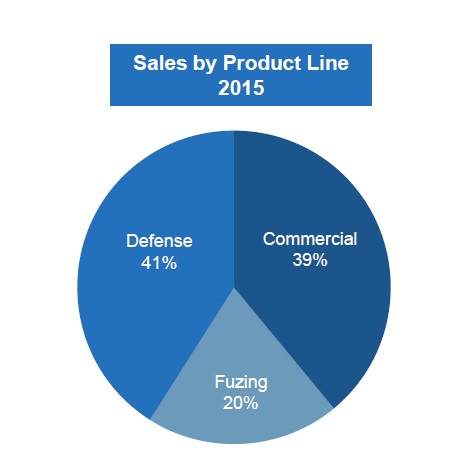

The smallest of these Aerospace & Defense picks is Kaman Corporation (KAMN, Financial). As Gabelli tells it, the company makes tapered roller bearings and bomb fuses. The company would say it makes complex metallic and composite aerostructures for commercial, military and general aviation and solutions for missile and bomb systems. It isn’t the cheapest among the three with a forward P/E of 15x and an EV/EBITDA of around 11.3x. It has the worst balance sheet with about $420 million of debt against $140 in EBITDA.

Between these three it does appear Kaman is the most levered on the Defense industry. Not all of its products are used in weapons, but it does seem to end up with the military a lot. Below you can see a breakdown of sales by product line taken from the company’s most recent investor presentation:

I’d say Kaman has the most direct exposure to the Defense industry, but it comes at a price.

Textron

Textron (TXT, Financial), a $9 billion market cap weapons and aerospace company, is another one of his favorites. This company has the same problem as Honeywell in the fact that it is diversified beyond Defense. Bell helicopters, Cessna and Beechcraft are some of its aerospace brands. However, Gabelli thinks the guy who's running it, CEO Scott Donnelly, is doing a great job. With a forward P/E of 12x and an EV/EBITDA of 8x, it appears a little bit cheaper compared to Honeywell. Just like Honeywell it appears to have a sound balance sheet. Net debt only exceeds annual EBITDA by a slight margin.

Image: Textron CEO Scott Donnelly