Allergan (AGN, Financial) stock has dropped a lot because of rumors Pfizer (PFE, Financial) will walk away from their deal.

Pfizer made no attempt to pretend the deal was about anything but lowering its tax bill by relocating its headquarters to Ireland, Allergan’s homestead. The Irish tax rate compares favorably to the U.S. at 12.5%; when you are making billions in profits, it’s worth it to pay a couple of lawyers to figure it out. It seems the U.S. Treasury is now inventing new ways to apply rules just to spite Pfizer, and it looks like that’s working.

Whether you think that’s awesome or despicable, the fact is we can now buy Allergan shares at $236 a piece.

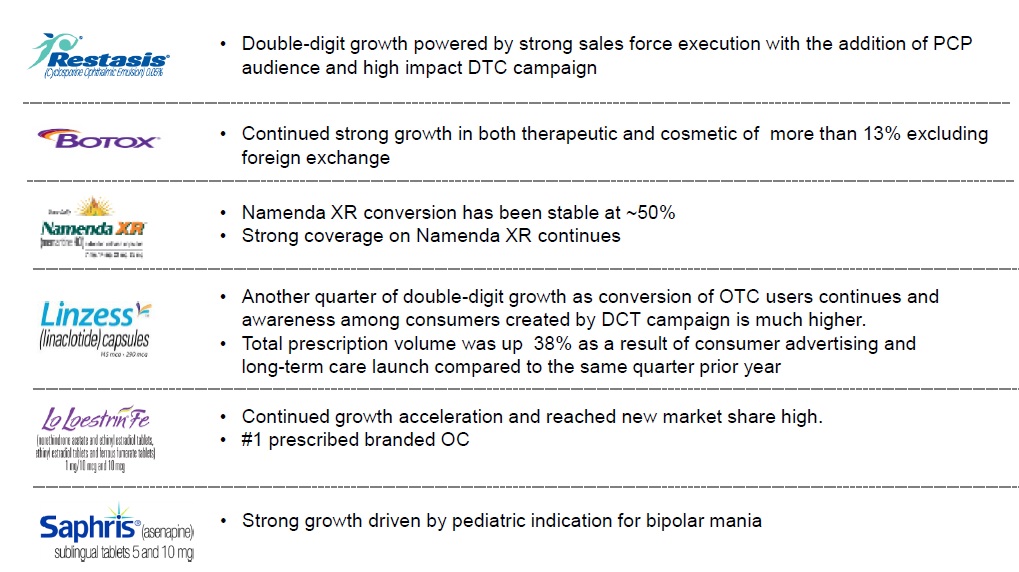

Allergan is a diversified drug firm with a $100 billion market cap and a drug portfolio with global appeal. It may be most famous for the cosmetic Botox ($2 billion in sales annually):

Source: company presentation

However, it also has a strong pipeline of drugs coming online, promising healthy future cash flows. An added benefit of the merger falling through would be that Pfizer likely owes Allergan $400 million in that case – a nice windfall to pick up for our stress.

Allergan is something of a serial acquirer like Valeant (VRX, Financial), but contrary to that more aggressive peer it isn’t known for its “brilliant” accounting. Management is known to be a little more conservative. Remember how it walked away from the Valeant deal engineered by Bill Ackman? Allergan spoiled the fun there, but in retrospect it looks pretty smart.

Managing revenue growth of nearly 25% per year for over 10 years is phenomenal. Management didn’t do just that but also grew EPS nearly as much. You are probably thinking it slashed R&D (and consequently cash flow from future drugs) to do so. Good thinking! But no. Spending on R&D doubled as a percentage of sales since 2006.

If you bought in 2006, you owe the management teams a round of Guinness!

Allergan is also divesting its generic segment, where it lacks scale (third in the U.S.), which should boosts RoIC.

The debt load is a bit on the high side, though. Allergan has almost $40 billion in debt. Luckily Teva (TEVA, Financial) is paying about $40 billion for Allergan’s generic business. If that deal doesn’t fall through, we will see a reduction in EBITDA, probably an improvement in margins and debt falling to zero.

Currently, Allergan looks fairly expensive on an EV/EBITDA basis of 25x but on a forward P/E basis of 13.68x it looks much more affordable. Considering how well the management team did over the past 10 years, it seems prudent to pay up a little bit here.

Allergan is also widely owned by gurus like John Paulson, Steve Mandel (Trades, Portfolio), Jana Partners (Trades, Portfolio), Lee Ainslie (Trades, Portfolio), Daniel Loeb (Trades, Portfolio) and many others.