Green Brick Partners (GRBK, Financial) is a land development company with a bank of land in favorable parts of the Dallas and Atlanta areas. In addition it owns controlling interests (of exactly 50%) in four homebuilding companies.

The company was set up and customized around 2008 by guru David Einhorn (Trades, Portfolio), of Greenlight Capital and Jim Brickman, who was going to lead it. Brickman has 35 years of experience in the business. Einhorn owns ~50% of the equity and Brickman around 10% through various names. They called it Green Brick. Get it?

Daniel Loeb came in around 2015 and put up $175 million at $10 per share. Right now you can buy it at around $7.5, and Loeb is increasing his stake (see GuruFocus' real time buys). At $7.5 your cost basis should still be significantly below that of Loeb’s Third Point's. More on valuation later.

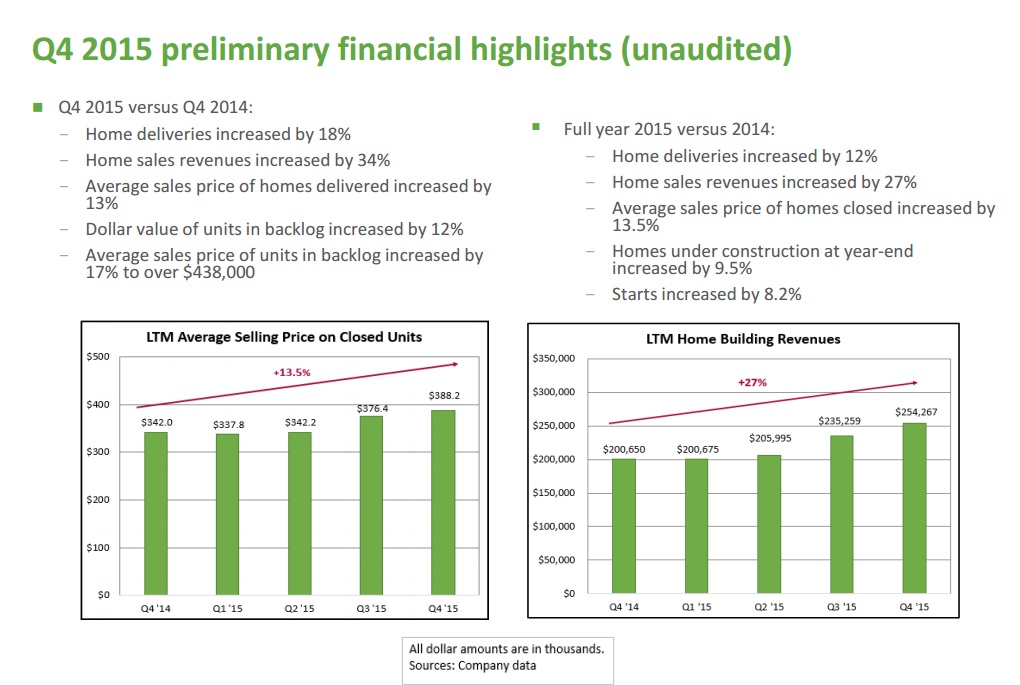

The short-term outlook is favorable with especially the Dallas market doing well, but Atlanta isn’t doing badly either. The slide below shows how home deliveries are up, home sale prices are up, and the company is actually selling higher-priced homes out of its inventory.

Management is also very positive about its outlook and sees significant opportunity for growth in 2016 and beyond. Green Brick has a very conservative balance sheet with only about $10 million in net debt against an EBITDA of $34 million. When the opportunity presents itself Brickman will pounce and load up debt to capitalize on growth.

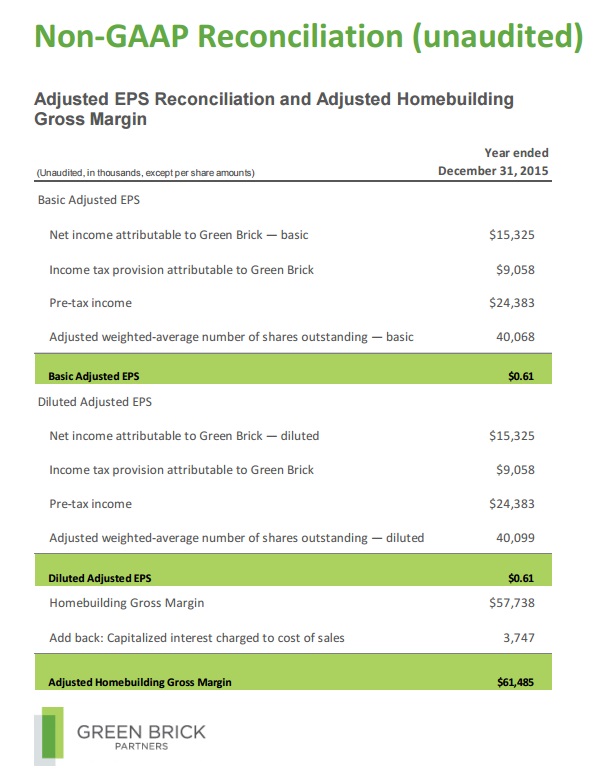

But the company is already making money:

It basically makes money in two ways:

- By selling land from its land bank once it's developed. This means value is added, and remember this land was acquired back in 2008 so its value is probably understated on the books.

- By building and selling homes, a value-added strategy. The company only receives 50% of this revenue stream as the rest goes to the operating homebuilders.

Valuation

At 1.07x book and a P/E of around 6x the company is quite cheap although its 12x EV/EBITDA multiple falls in a more conventional value range. There are actually 1.2 million shares short, but I’m not convinced of the wisdom in that as about 90% of the shares are with insiders (CEO, Einhorn and Loeb) and institutions.

With 20% of the limited remaining float short, it’s asking to get short squeezed. But this short interest may have caused some price pressure exactly because of the limited float. Lately, the stock is recovering fast which makes sense to me given its undervaluation.