The investment case for IBM (IBM, Financial) is that it is a company in transition and very close to its goal of achieving top line growth once again. But how long will it take, and what are the numbers that show us that this is actually happening?

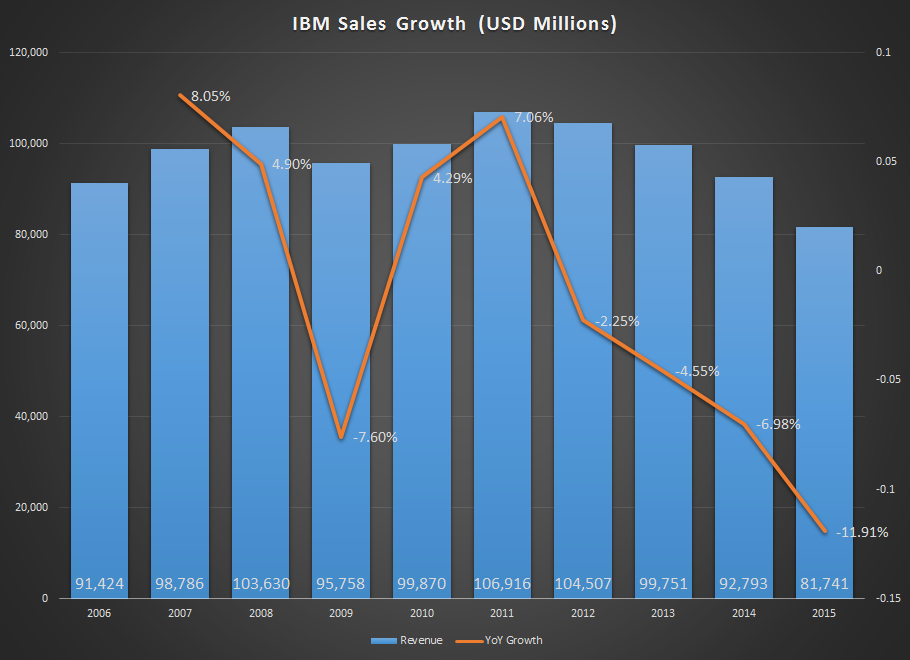

Since 2008, IBM’s revenues have been on the decline. Taking over in early 2012 as CEO, Virginia Rometty has been mandated to drive several key initiatives IBM is calling its strategic imperatives. The idea behind this is to steer the company toward future-ready business lines with higher profitability than its legacy units. Those legacy units continue to drag the company down even as new businesses keep growing by leaps and bounds.

Source: Morningstar

The big question in everyone’s mind is this: how long does it take for a 105-year-old company to reinvent itself in a sustainable way? Let’s dig into a few key numbers to see what’s happening under the hood and how long it will be before the company is growing profitably once again.

A closer look at 2016

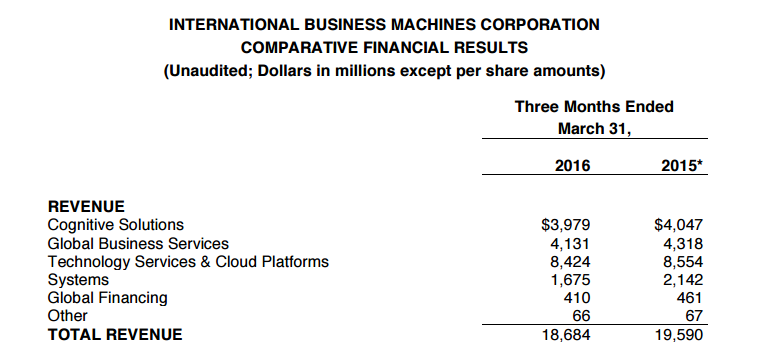

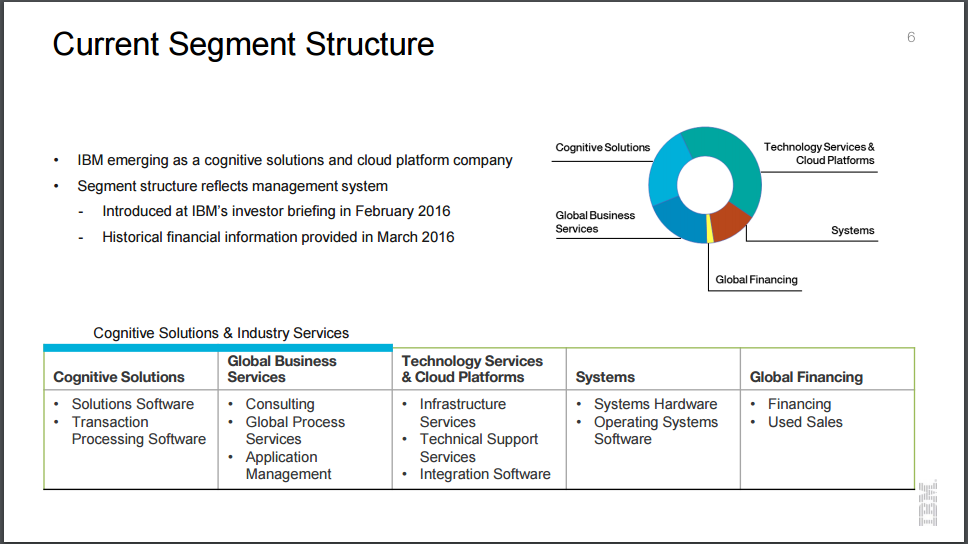

One of the significant changes in this year’s first quarterly report is the company’s reporting segments. The move was intended to better capture the growth of relatively new business lines such as cloud and cognitive solutions – to cite the two most important offerings.

Source: IBM Press Release

A look at its segmentwise report for the first quarter doesn’t paint a pretty picture. The company continues to lose ground in every area from Cognitive Solutions to Global Financing, with nearly a $1 billion dip year over year. That’s happening because the new reporting lines represent a mix of legacy and new businesses.

Source: IBM Quarterly Release

For example, even though its cloud revenues are growing at double-digit levels, the segment itself posted negative growth because it also includes tech support and integration software-related income in addition to cloud infrastructure services. That clearly shows that cloud IaaS needs more time to offset the decline in the other units included in the segment – and that’s what we’re really after with this article.

On a more positive note, overall revenue was up 1.9% for the segment on a constant currency basis, but that’s hardly the kind of growth Rometty wants. Her goal is to build the strategic imperatives into something more cohesive and profitable than its legacy businesses ever were while laying the foundation for sustainable growth in those areas.

Essentially, its first-quarter report shows traces of that growth and profitability but with legacy lines of business still impeding overall improvement.

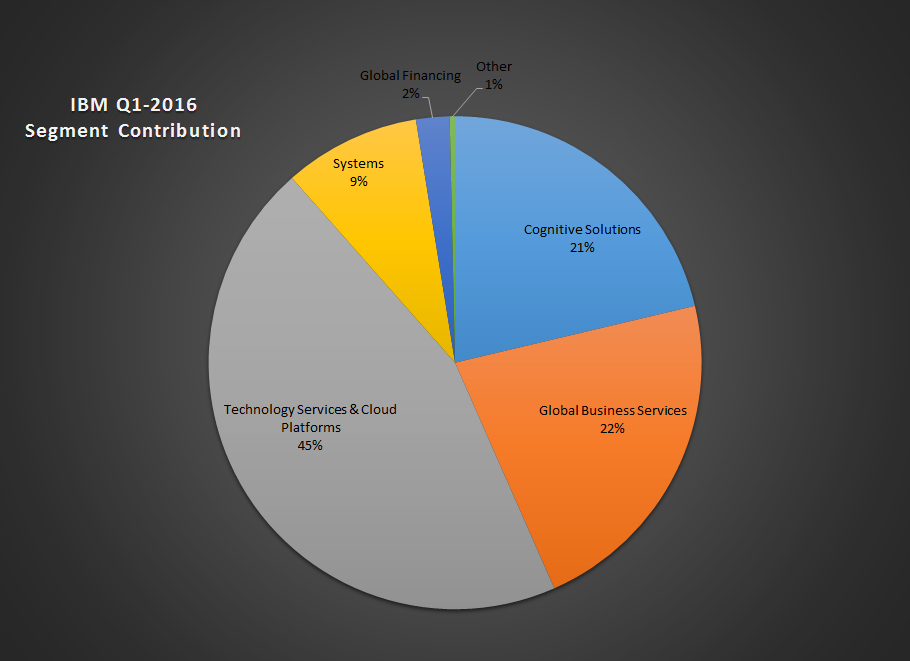

Zooming in even further on 2016

Source: IBM Q1-2016 Report

There’s no doubt that cloud and cognitive form the cornerstones for IBM’s reinvented structure; with a two-thirds contribution to overall revenue, these are the areas for aggressive focus and effort.

In a recent press release, IBM announced that the IDC has officially recognized IBM as the world's No. 2 provider of cloud infrastructure services – proof that its push on strategic imperatives is beginning to bear fruit.

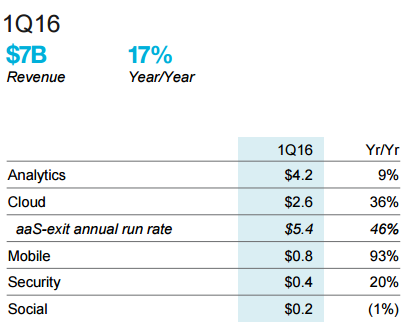

Source: IBM Quarterly Release

If we look a little bit closer, IBM has $7 billion worth of business lines per quarter that are growing, mostly at double-digit levels, with cloud and analytics bringing in the bulk of the gains at $2.6 billion and $4.2 billion. These businesses will not only bolster the top line directly but will likely lead to add-on revenues from technical support, consulting and so on.

The only issue here is that the 17% overall growth in strategic imperatives does not yet match the quantum represented by the gradual 5%-plus decline in legacy businesses.

A little extrapolation

Now, if we extrapolate that to the next two years using the actual growth figures for the two key strategic imperatives, this is what we’ll see:

| Amounts in Billions | Â | Â | Â | Â |

| Component | Growth Rate | Q1 2016 | Q1 2017 | Q1 2018 |

| Analytics | 9% | $4.20 | $4.58 | $4.99 |

| Cloud | 36% | $2.60 | $3.54 | $4.81 |

| Â | Â | Â | Â | $9.80 |

So, in two years, assuming current growth rate continues on strategic imperatives, we’re looking at a TTM figure of slightly under $40 billion. That figure is now $28.9 billion as of the first quarter – or 37% of its TTM revenue.

Its current legacy business brings in about $50 billion-plus annually so even at a decline rate of over 5%, it’ll hold above the $40 billion mark for the next two years. That is around the point at which IBM’s transition will take effect from a top line point of view.

The moment strategic imperatives are able to consistently contribute to 50% of overall revenues is when IBM will start to show consistent revenue growth. After that, it’s a question of continued growth that will happen on the back of an ongoing aggressive push around its cloud business – whether it’s Watson, SoftLayer, Bluemix or any other support service it's launched in recent years.

The icing on the cake

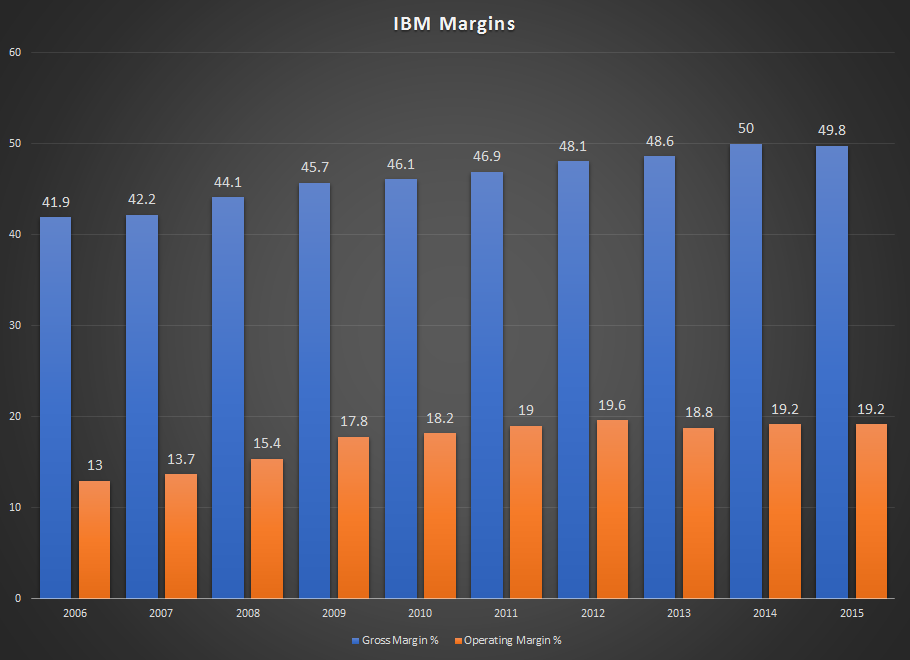

Along with top-line growth, Rometty wants to implement business lines that are more profitable as well, and you can see that happening even now.

Source: Morningstar

Despite the pain that the company has been going through for the past few years, this is one area that it's had razor-sharp focus on – and it's more or less consistently kept its operating margins above the 19% level since Rometty took over. That’s already far more efficient than it was 10 years ago.

The investment angle

If you’ve been on the fence about IBM stock, this is the time to get off and get into its camp. According to my estimates, in two years or less, IBM will be growing revenues once again, and this time its margins will be stronger and its business lines will be more suited to carry the company forward into the next decade and beyond.

If you invest now, you’ll need to be patient until you see its efforts bear fruit, but at a forward P/E ratio of around 11, the market isn’t expecting the company to grow. That’s why this is the perfect time to invest so that five years from now you can be sitting on some handsome returns, and the 3.5% dividend yield will be a bonus.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.