Pfizer (PFE, Financial) is one of the world’s largest drug manufacturing companies with $223 billion in market capitalization. Only the more diversified Johnson & Johnson (JNJ, Financial) is ahead of Pfizer with more than $300 billion in market cap.

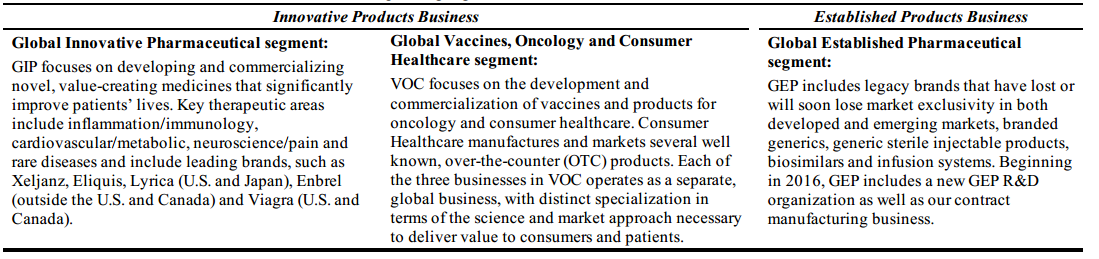

Pfizer reports its earnings through three segments: GIP or Global Innovative Pharmaceutical, Global Vaccines, Oncology and Consumer Healthcare (VOP) and Global Established Pharmaceutical (GEP).

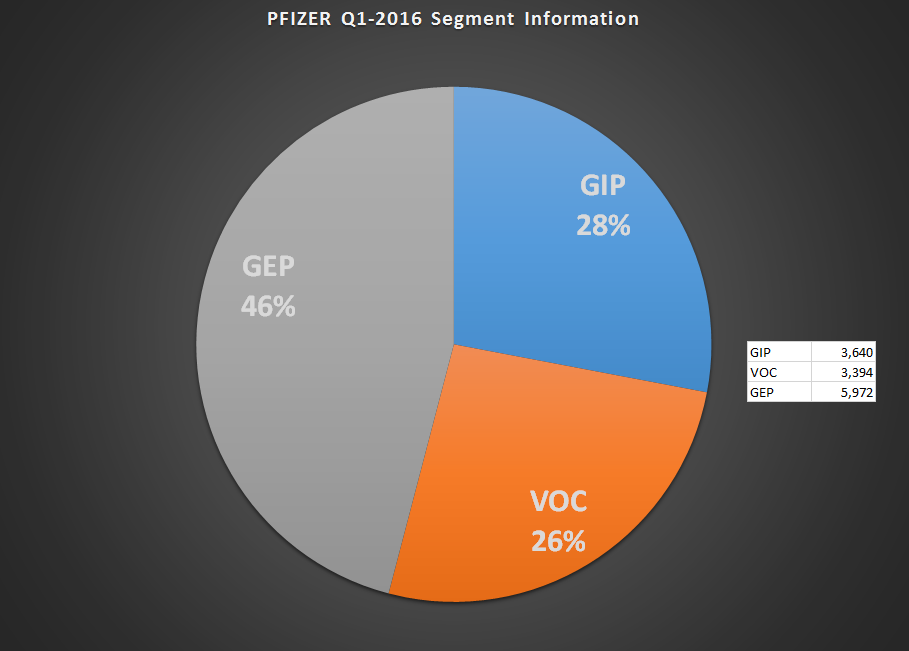

Of the $3.394 billion from the VOC segment, $822 million came from consumer health care. Pfizer is a hard-core drug-manufacturing company, which means it will have to constantly add billion-dollar drugs to its portfolio and make sure that a patent expiry on one of its star performers doesn’t push it over the cliff.

The industry landscape has changed so much over the years. Generic drugs and biosimilars are always waiting for a drug’s patent to expire so they can take over. And in many cases, they don’t even wait anymore.

Big name drugs are always under constant threat as competition tends to follow wherever the money goes. When you are a company with more than $13 billion in quarterly earnings, things are indeed going to be difficult for you. How do you keep increasing that number? You need to keep adding more drugs to your portfolio and, at that scale, even continual innovation may not be enough. So when you don’t have it in your pipeline, then you obviously have to buy one to fill that pipeline.

Big drug companies have no choice but to constantly buy pipelines; and even then, it may not be enough. Add all the litigation and expensive research cycles to go with it, and drug companies are often caught between a rock and a hard place.

If you want validation on how the life sciences industry has become “not as attractive” anymore, look no further than Warren Buffett (Trades, Portfolio)’s portfolio. The buy-and-hold-forever oracle dumped his GlaxoSmithKline (GSK, Financial) stake in 2014, and he has been trimming his positions on Sanofi (SNY, Financial), Johnson & Johnson and Procter & Gamble (PG, Financial) as well. So much for pharma being a defensive sector; Buffett’s portfolio hardly has any exposure to the segment.

Is buying pipelines a bad strategy? No, not at all. But the problem for Pfizer at the current size is that it has to be constantly at it in order to keep that position.

The big problem with that approach is that a long-term investor finds it very hard to predict the business’ future prospects. For example, can Pfizer double its current quarterly revenues in the next 10 years? What is a reasonable growth rate that can we can use to model our expectations on? These are the questions that have become extremely hard to answer, and possibly explains why Buffett is totally out of this sector.

Where does that leave Pfizer then?

Pfizer seems to be on the right track. It is constantly building its own pipeline and at the same time staying in the market to buy companies. In May the company announced that it will be acquiring Anacor Pharmaceuticals (ANAC, Financial) for approximately $5.2 billion.

“The acquisition will give Pfizer access to a nonsteroidal topical gel, crisaborole, which is currently under review by the U.S. Food and Drug Administration for the treatment of mild to moderate eczema.” – Reuters

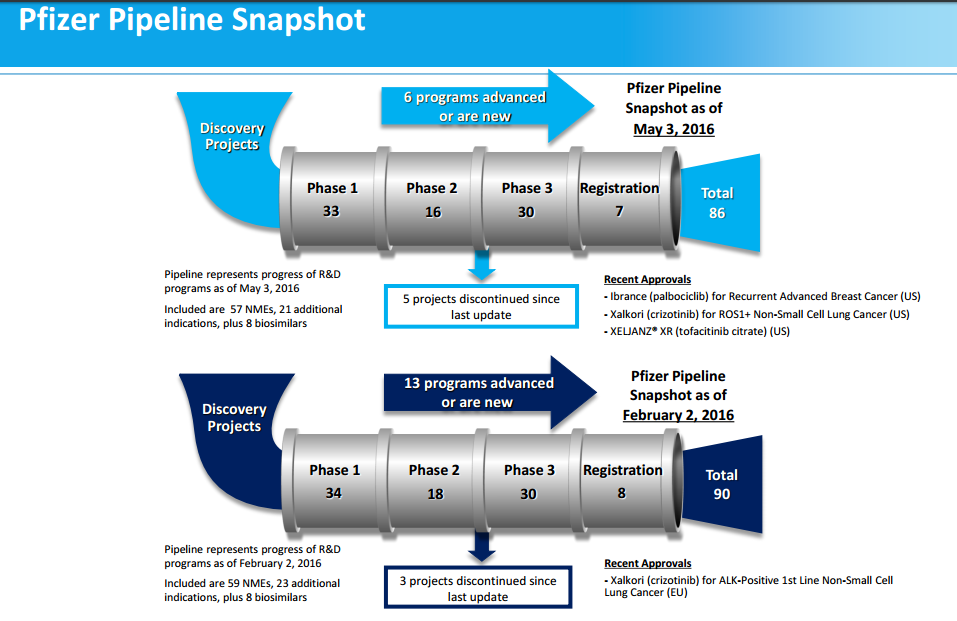

And this year seems to have been a good start for the company with revenues jumping by 20% compared to last year and operating income going up by 27%. With respect to pipelines – the other crucial factor to determine the company’s future performance – Pfizer has 30 programs in Phase 3 and 8 programs in the registration stage.

Mikael Dolsten, president, Worldwide Research & Development during Q1- Earnings:

"We have 85 projects spread across Phase 1 to Phase 3 registration. And let me just mention a couple that we think will be really unique and differentiating. We already touched base on 4-1BB, on OX-40 and the triple I-O combo.

"Lorlatinib in the ALK and ROS space is generating very interesting data that we will start to share. We have a novel ADC called PTK-7 that we'll also see some real interesting response rates.

"In the immuno-inflammation field, in addition to Xeljanz, we now have four different immuno-kinases going into Phase 2, with several highly specific JAKs going to inflammatory bowel disease, dermatological inflammation and lupus. So we will share more data around those, but I think that will really move the entire JAK field over time into new areas and with the new profiles.

"In rare disease, we have a growing sickle cell franchise with rivipansel and a plan to start PD-9 as a way to prevent occurrence of difficult-to-treat rare disease episodes."

A note to investors

In the short to medium term, Pfizer seems to be a safe bet. With $19.443 billion in cash and short-term investments and LTD of $27.824 billion at the end of first quarter, the company has plenty of room to dip into its own pockets to keep the drugs flowing.

But the problem I have with Pfizer is more of a sector-specific one, where the predictable nature of the business is virtually nonexistent for the long term. If you invest in Pfizer or any other drug major, don’t expect earth-shattering returns and always enter with a nice margin of safety – like buying the stock only on dips.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.