Over the past few months, I’ve been writing about several companies in pharma, restaurants and other industries. During that time, I’ve come across several duopolies in specific industries. The deeper I looked, it seemed that these were ideal investment destinations for long-term investors. They were at the top of their game, they had solid moats preventing new players from threatening their dominance and they were in a position to pay some handsome dividends.

That journey has lead me to the two top communications companies in the U.S., AT&T (T, Financial) and Verizon (VZ, Financial). In one sense, they are similar to utility companies that keep the lights on, in a manner of speaking. However, there’s one big difference: These companies operate in a highly disruptive segment where the speed of innovation is astounding. And that’s exactly what makes them such appealing investments.

You can’t invest in one without the other, so it’s best that you understand where they stand on stability and the ability to keep paying and growing their dividends. These are not high-growth companies; they are the mules of the investment world, carrying heavy loads but nevertheless progressing up the mountain one step at a time.

Revenues, growth and innovation

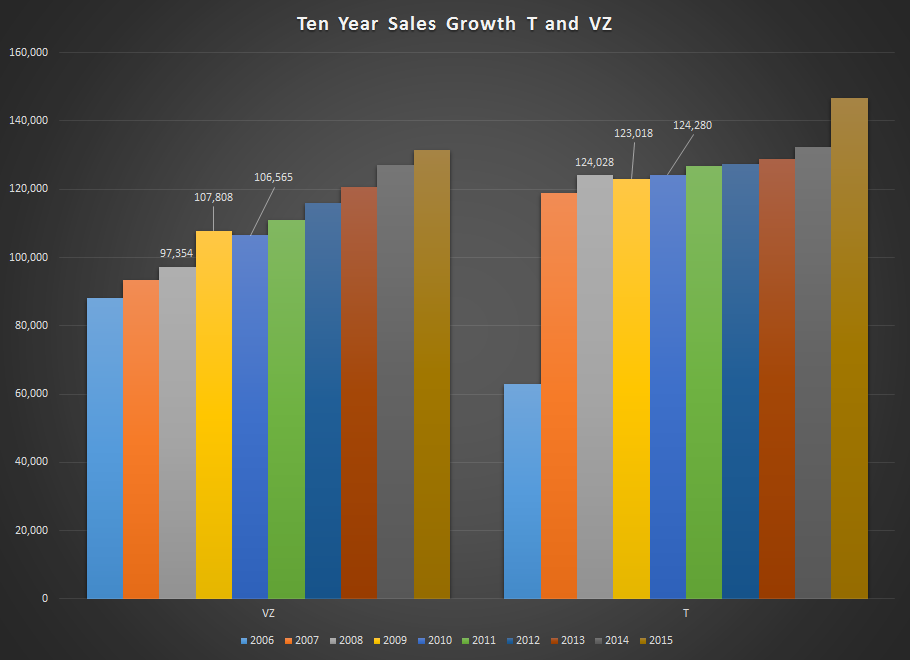

Together, these companies have a combined revenue of more than $270 billion and enjoy a market capitalization of $489 billion, a testimony to their size and scale. The other important factor of note is the way both of these companies blazed through the great recession. Verizon increased its top line during that time, while AT&T held its ground, a clear indication of their resilience to economic ups and downs. The downside of such resilience is, of course, the slow and steady growth that we can expect these companies to have, instead of the high and fast growth that other companies might boast.

If you want stability, this is as good as its gets; if you want blazing fast growth, look elsewhere.

Though their markets are pretty much saturated at this point, it does not mean that these companies are slow to innovate. Case in point is how Google tried to muscle in on the fiber internet market and provide GB-speed internet to the market but fell short of the goal.

In a nutshell, Google’s plans to roll out high-speed internet connectivity in Atlanta, Georgeia, fell flat when Comcast and AT&T beat them to it. In fact, AT&T already provides the new GigaPower service in over 20 metros, with plans to launch in 36 more, while Google only serves four cities with a total user base of under 100,000.

Looking on the bright side, you could say Google shook a few giants awake and made them move faster to provide high-speed internet to their users, but it's probably not what Google had in mind.

My point is this: If Google (GOOGL, Financial) —Â with all its money and reach — took so much time (six years) and effort to make even a small dent in the market that these players operate in, how much more prohibitive will it be for smaller players?

That’s the kind of “stayability” I’m looking for. And now that we have that out of the way, let’s look at their dividend yields and financial strength.

Dividend yields

Dividend.com Verizon

Dividend.com AT&T

Both companies look very attractive from a dividend yield perspective. Normally, a high dividend yield with a high payout ratio would be a red flag for me but in this case, I’ll make an exception. The reason is that this is a capital-intensive business. Building and maintaining massive communications networks requires skilled manpower — and lots of it.

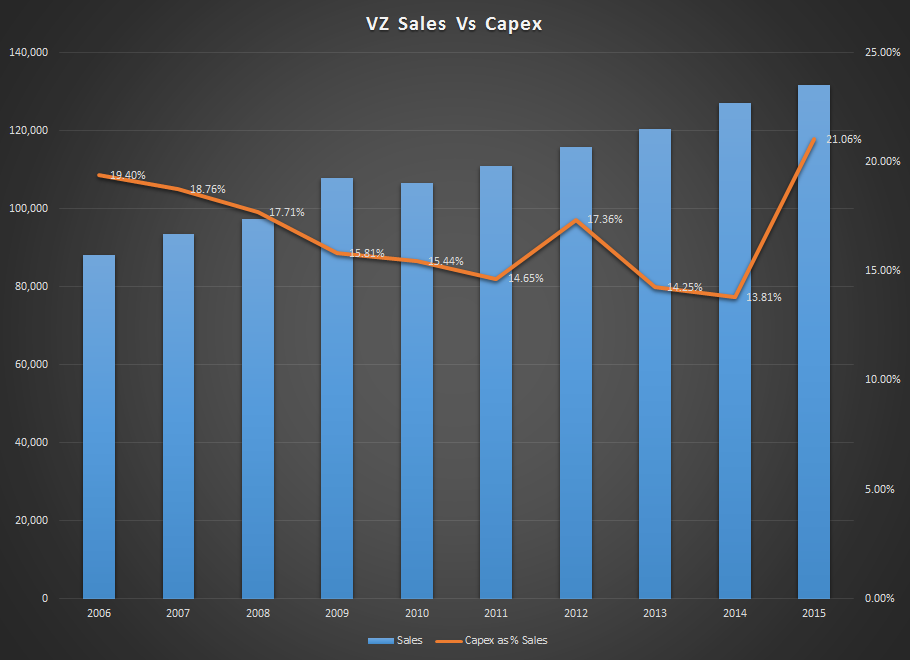

Verizon has a massive workforce of around 180,000 employees; AT&T has a quarter of a million. Verizon’s capital expenses for 2015 were 21% of revenue, while AT&T spent 13.63% of revenue on capex. You need to spend a lot of money to stay relevant in this market, and it’s nearly impossible for a newcomer. It's even harder for old players to recover once they’ve let the competition walk away with market share —Â case in point being Sprint (S).

And that’s another reason I think these are solid companies. Despite having such high overheads, they’re able to provide high returns for investors. And, at sub-70% payout ratios, they’ve still left room for themselves to grow those dividends further.

Financial strength

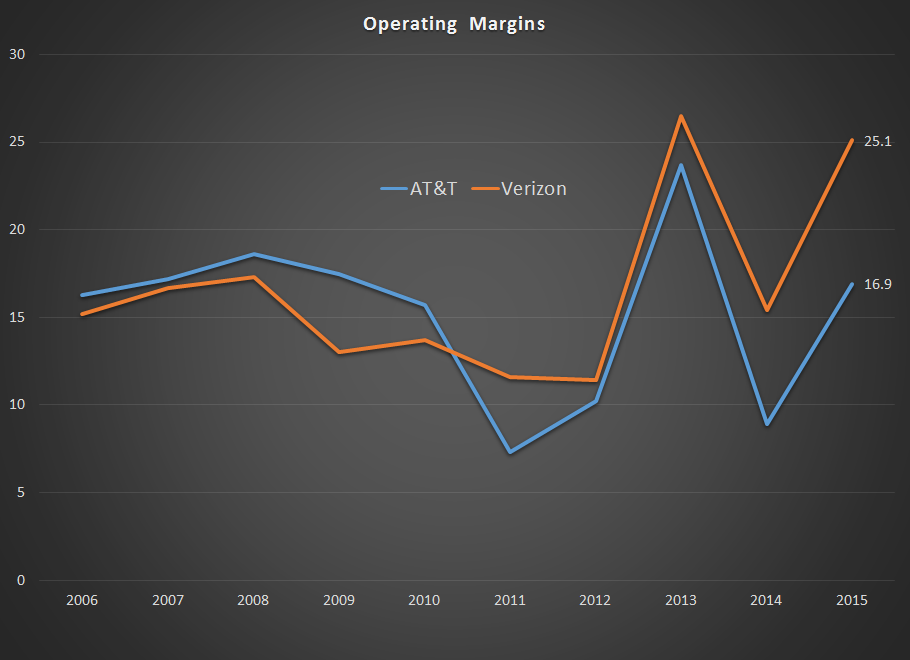

Both companies enjoy double-digit operating margins, with Verizon showing more stability on the front, while AT&T’s numbers showing heavy fluctuation.

Capex for these two telecommunications giants are in the $15 billion to $20 billion range, but the upside is that there is very little in the way of competitors who can put up that kind of money without already having a huge presence.

Just looking at the capital expense requirement, you’ll see that both these companies have to depend on debt to keep moving forward, whether it’s to buy other companies or to fund their paybacks to shareholders.

As such, both these companies have a considerable amount of debt load.

At the end of the most recent quarter, AT&T had long-term debt of $118 billion, with Verizon not too far behind at $103 billion. But Verizon has been slowly chipping away at its debt, and the company says that it wants to get back to an A- credit rating, which is always good to hear from a company of this size.

“Verizon Communications Inc.'s strong performance since acquiring full ownership of Verizon Wireless puts the company in a position to recapture its A3 rating, but it may decide to forego the higher rating if the current low interest rate environment persists, making the company's debt attractive to yield-hungry investors," Moody's Investors Service said.

"Moody's had downgraded Verizon's long-term debt rating to Baa1 from A3 in September 2013, at the time of the acquisition, with Verizon stating that it would restore its A rating by 2019.”

Note to investors: The T-VZ combo

If you want to add stability to your portfolio, then look no further than AT&T and Verizon. The yields are attractive Moody's had downgraded Verizon's long-term debt thanks to the debt load these companies are carrying, which I am sure the companies will start to climb down on once interest rates start moving northward.

To use a loose analogy, these companies differ from another capital-intensive industry: automobiles. In the highly cyclical and volatile automobile game, high debt can easily push a company into bankruptcy when recession hits. This is not the case with telecomm. AT&T and Verizon can both survive another recession Moody's had downgraded Verizon's long-term debt — should that occur — and keep on ticking because communication and accessibility are two of the last things people are going to let go of even in the worst of times.

Despite high debt and high capital expenditures, T and VZ have impressive operating margins and strong financials to back them up. They are also exploring new revenue streams through buyouts, so that’s going to further strengthen their top lines.

On the whole, it doesn’t get much better than this. I would recommend adding periodically to your position in both companies using a dollar-cost averaging approach or simply reinvesting your dividends over and over again. Over time, this T-VZ combo could become a nice little nest egg that you can retire on.

Disclosure: I have no position in any of the stocks mentioned and no intention to initiate any position in the next 72 hours.

Start a free 7-day trial of Premium Membership to GuruFocus.