Netflix (NFLX, Financial), one of the world’s largest video on demand service providers, is having a nightmare 2016. The stock has lost an eye-popping 35.6% of its value from its 52-week high of $133.27. But the key factor to note here is that, despite all the drawdowns affected by subscription shockers during the first and second quarter of the current fiscal year, the stock is still trading above 5 times sales. Welcome to the world of hyper-growth stocks — if you are not careful they will burn you for sure.

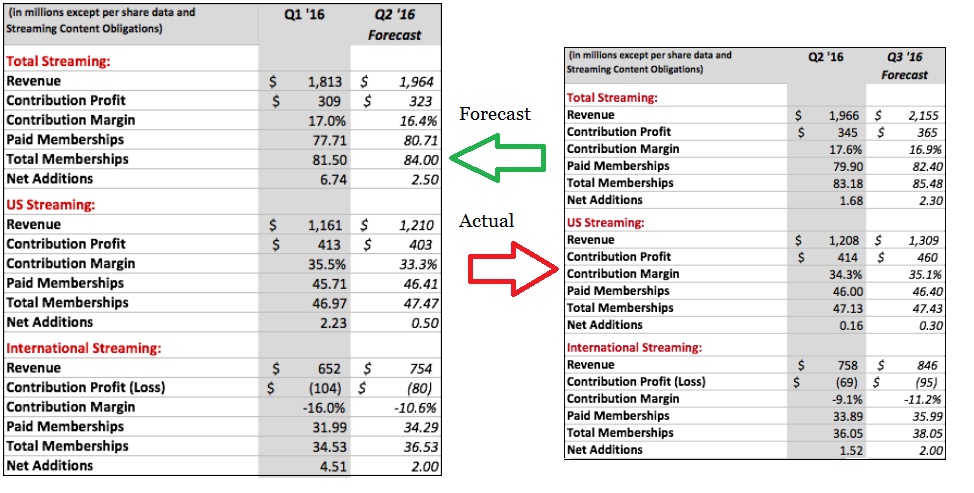

During the second quarter Netflix added 1.7 million subscribers, but the problem was that in its first quarter call, the company forecasted 2.5 million net adds for the second quarter, with 500,000 coming from the U.S. and 2 million from rest of the world. But in reality it was only able to manage 1.68 million net adds, with 160,000 from the domestic market and 1.52 million from International markets.

Although the company exceeded its goal for contribution profit, the unusually high rate of churn for the quarter was responsible for the dismal net additions. According to CEO Reed Hastings in a conference call with investors Monday, he said competition was not the likely explanation for the hit.

"Well, the obvious explanations other than this are competition, which we're pretty confident that it is not a factor because we got this slight uptick in churn in multiple countries the same week and—of course that's not a competitive signature—including Canada, where many of the other SVOD services don't operate," he said in a conference call with investors on Monday." - CNBC

Hastings may have a point, but the reality is that Netflix has more than 45 million paid members in the U.S. and though it may not have reached peak penetration yet, it cannot grow at the same rate it did five years ago. And when you throw in the increasing competition, Netflix can only expect slow and steady growth in its home market —Â not the rapidfire growth it enjoyed in the past.

In a way, the slowing growth in mature markets does help explain why Netflix wanted to expand to so many countries in such a short period of time. Netflix knows that this is an age where investors are looking more at user base growth than earnings per share, at least for companies such as Netflix, Facebook (FB, Financial) and other consumer-facing companies. So the international push did make sense, and the company now offers its content in more than 190 countries.

The investment angle

Here’s my question: What's wrong if they face a bit of a headwind for a few quarters? It’s perfectly normal for any company to have its ups and downs during its growth phase but as an investor, whenever you are buying a company with high price-to-sales ratio, you better get ready for the inevitable roller coaster ride to follow. Even small shocks to such stocks can have disproportionate effects, and that’s what Netflix is going through this year — and it continues to trade at nearly five times sales.

This is not a buy-and-forget stock. If you want in, buy small amounts whenever the company has a subscription shocker like this one. It has given a guidance of 2.3 million net additions for quarter three, with the U.S. and International estimated split being 330,000 and 2 million, respectively. If it misses, it's going to get hit again, most likely. And that’s the time to add to your position.

Netflix is going through a market problem right now, not a business problem, so let’s all try and remember that. It’s not like it has become the worst company in the world in two quarters. Its business case is solid, it is operating in an area that looks deep into the future and it is the leader in its segment. But wherever success goes, the competition will follow, and with each passing day competition is increasing for Netflix, at least in its home turf. Don’t expect growth to be the same as before unless at least a few of the larger international markets start to yield.

Disclosure: I have no position in any of the stocks mentioned, and no intention to initiate any position in the next 72 hours.

Start a free 7-day trial of Premium Membership to GuruFocus.