Though I like to select companies that represent an oligopoly or a duopoly for a dividend portfolio, Cisco Systems (CSCO, Financial) is possibly one of the few companies that I would like to have despite the company operating in an extremely competitive environment.

There are several parts of the business that can withstand the competition and allow the company to keep moving forward. When you factor in its financial strength and ability to keep dividends flowing into the next decade, Cisco indeed makes a compelling investment case.

Cisco’s proactive nature

Cisco is one of the few companies that have been proactive about the growth of the cloud industry, but its proactiveness shines through in several parts of the business. In short, it's been able to deal with nearly every curveball thrown at it.

Take the Skype threat, for example. Skype for Business entered the market at a time when corporate offices were highly dependent on Cisco for their video conferencing needs. But Cisco did not wait for such a threat to appear on the horizon. As far back as 2007, it acquired WebEx. Continually developing the product, it added yet another to its ranks – Cisco Spark. The products are intended for different audiences and are equally capable of standing firm against the Skype onslaught that began in 2010 as Lync.

How Cisco is evolving

With the advent of cloud, Cisco is undergoing another kind of transformation. From a business that depended heavily on switching and routing revenues, it is evolving into a cloud solutions provider by focusing more on integrated systems and architecture.

“Over the last few years, we have been transforming our business to move from selling individual products and services to selling products and services integrated into architectures and solutions. As a part of this transformation, we continue to make changes to how we are organized and how we build and deliver our technology. We are focused on how we accelerate what is working and change what is not, simplify our business and our communication, drive operational rigor in everything we do and invest in our culture and our talent.” – From the 2015 Annual Report

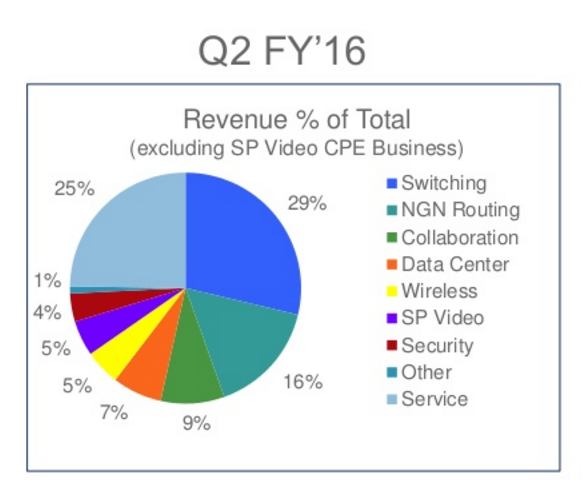

As you can see below, the shifts in revenue distribution bear this out.

Data center and collaboration revenues are showing strong growth even as switching and routing income slowly loses its vicelike grip on the market. Although the third quarter was one of negative revenue growth, the year-to-date figures are still in the black.

Yes, it does still rely on its core businesses to support it, but that’s gradually changing. The change will take several years, but for now it's on the right path. Data center and collaboration incomes now account for more than 16% of overall revenues.

Moreover, it's been fairly effective at arresting the slide of its core businesses to a great extent, only dropping year over year from $11.02 billion to $10.95 billion year to date. These businesses are still very much a part of the majority of enterprise-level companies around the world, and that’s not going to go away overnight.

The best part about Cisco, however, is not its evolution: it’s the financial muscle that ably supports that evolution.

Cisco’s financials

Cisco is the fourth-largest company in the world in terms of cash on hand. With $63 billion-plus in cash and investments, its books are solid, and it has less than $25 billion in long-term debt.

That’s what makes it a truly great dividend investment.

Moreover, its dividend burden as of the last reported quarter is around $4.5 billion, and it paid out around 35% of its free cash flow as dividends. Free cash flow for the period was $12.69 billion while capital expenditures are in the region of $1.2 billion, and the numbers have been at that level for quite a while.

That’s a good place to be if you want to attract dividend investors, and that’s exactly the case I’m making for Cisco. But the real “meat and potatoes” of that case is actually its revenues. After all, financial strength means nothing if you cannot keep adding to it year over year.

As you can see, Cisco’s revenues show an upward trend despite the highly disruptive nature of the industry it's in. And with revenues related to cloud and IoT (Internet of Things) on the uptick, the company will be able to maintain that upward trend in overall revenues.

Note to investors

This is not a high-growth company like Facebook (FB, Financial) or Amazon (AMZN, Financial). It’s a stalwart in its own industry, but that industry gives very little leeway for rapid growth. Cisco is optimizing its gains on any area that lends itself to such strategies, but I see slow and steady growth over a period of time.

The best part about investing in Cisco is the fact that they’re only trading at a forward P/E ratio of under 13. And with a dividend yield upward of 3%, there’s no reason not to recommend a BUY for this stock.

Disclosure: I have no position in any of the stocks mentioned and no intention to initiate any position in the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.