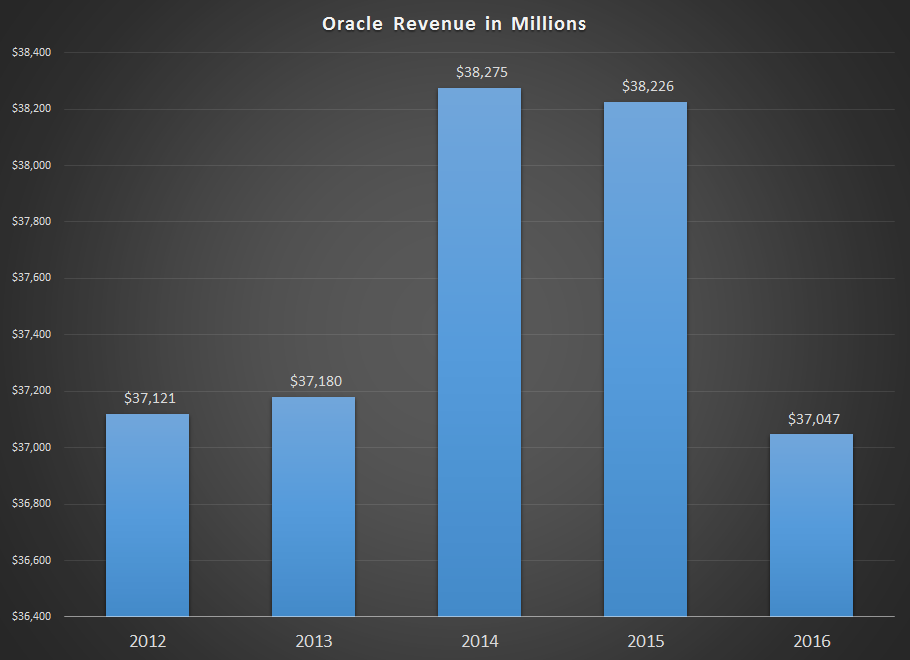

Oracle’s (ORCL, Financial) fourth quarter results were in line with analyst expectations, with the database king reporting earnings of 81 cents per share and quarterly revenues of $10.59 billion, agonisingly close to last year’s $10.71 billion.

Oracle is going through a huge transition phase right now, something I wrote about in detail recently in "Oracle and the Gaping Legacy Hole." As a company that made its mark and its money by selling software, hardware and services to companies that were managing their own IT infrastructure, that business model came in the direct line of fire of a burgeoning cloud infrastructure industry.

What parts are growing?

Oracle’s sales have been declining since 2014 and is yet to be arrested, and the only way they can do that is to continue their cloud push with the strengths they possess in SaaS (Software-as-a-Service) and PaaS (Platform-as-a-Service), as well as through their presence in the IaaS (Infrastructure-as-a-Service) segment.

The infrastructure component of their cloud business, along with Managed Cloud Services, brought in 2% of overall revenues during the fiscal 2016, in line with what they achieved last year. This fiscal year, that figure was $646 million, while the 2015 figure was $608 million, showing a 6% year over year growth.

But Cloud IaaS is not the strong suite of Oracle - at least not yet. If Oracle wants to stay in the game their key drivers will have to be SaaS and PaaS. Oracle has already built a lot of expertise in the CRM (Customer Relationship Management) and ERP (Enterprise Resource Planning) areas and if they play the cloud card there, they will obviously have a unique selling proposition. Oracle knows this, and that’s exactly what they have been trying to do after being late to the cloud party.

To put that in perspective, SaaS and PaaS came in at 66% (68% on a constant currency basis) revenue growth, representing $690 million in revenues for the fourth quarter. Compare that with the 6% growth in cloud infrastructure and you’ll see what I mean.

"We added more than 1,600 new SaaS customers and more than 2,000 new PaaS customers in Q4," said Oracle CEO, Mark Hurd. "In Fusion ERP alone, we added more than 800 new cloud customers. Today, Oracle has nearly 2,600 Fusion ERP customers in the Oracle Public Cloud -- that's ten-times more cloud ERP customers than Workday."

"We expect that the SaaS and PaaS hyper-growth we experienced in FY16 will continue on for the next few years," said Oracle Executive Chairman and CTO, Larry Ellison. "That gives us a fighting chance to be the first cloud company to reach $10 billion in SaaS and PaaS revenue. We're also very excited about the availability of version 2 of Oracle's Infrastructure as a Service (IaaS) -- which will enable us to speed up the growth of our IaaS business, which customers want to buy in conjunction with our SaaS and PaaS."

- Oracle

Estimated timeline for Oracle’s second growth cycle

With $690 million in the fourth quarter, Oracle is looking at an annualized run rate of $2.76 billion. As of now, most of their competitors are growing at the above 50% range. If Oracle can keep matching that year-over-year, then the company can get to $10 billion in annual revenues from this segment in two to three years.

It's a lofty ambition considering that they will have Salesforce.com to compete with on the CRM side and Microsoft’s and Amazon’s own offerings on the cloud side, not to mention IBM’s fast-growing Bluemix platform for cloud developers.

The next four quarters will give us a very clear picture of how this game is going to play out. Almost all the companies in the cloud segment are growing at a furious pace. Amazon (AMZN, Financial), Microsoft (MSFT, Financial) and IBM (IBM, Financial) are growing as integrated cloud providers, while Salesforce and Oracle (ORCL, Financial) are growing in the SaaS segment.

The cloud growth for all these companies is driven by the elevated demand for such services. More and more businesses are moving to the cloud - whether to a private model or a private-public hybrid model. As such, the industry itself isn’t going to see slower growth any time soon.

That’s exactly why Oracle’s next four quarters will be critical to their top line growth, and also why SaaS and PaaS will be the metrics to keep your eye on as a stakeholder or potential investor. Although I suspect healthy top line growth will take at least another six to eight quarters, the next fiscal should tell us whether they’re on track.

Disclosure:Â I have no position in any of the stocks mentioned and no intention to initiate any position in the next 72 hours.

Start a free 7-day trial of Premium Membership to GuruFocus.Â