It is a bit of a surprise that Oracle (ORCL, Financial) is still trading near its all-time high, especially since the company’s revenue has been relatively flat since 2012. The growth of the cloud industry directly impacted Oracle’s traditional business model, selling hardware and software to enterprises that manage their own infrastructure and the company is now fighting tooth and nail to reinvent itself as a “SaaS company”, in the words of Larry Ellison, former CEO.

The database king realized its mistake of staying away from the cloud business and jumped into it with both feet a few years ago. More recently, they bought NetSuite (N, Financial), in which Oracle’s co-founder, Larry Ellison, owns about 45.4% of common stock. The move was intended to add a bit more muscle to their cloud push, especially in the SaaS space where chief rival Salesforce.com (CRM, Financial) sits with the world’s most popular CRM application. On the other side of the fence is also SAP (SAP, Financial), the world leader in Enterprise Resource Planning (ERP).

That is two major players to contend with at this point and NetSuite could be the edge they have been looking for in the fight against Salesforce and SAP.

What are the implications of the NetSuite deal?

“NetSuite is really pioneering cloud and this will certainly add to Oracle,” said Bill Kreher, an analyst at Edward Jones & Co. “I think acquisitions are certainly consistent with the company’s long-term pedigree and strategy. You’ve got to pay for that type of growth.”

- Bloomberg

But what is the real motivation behind investing $9.3 billion in a cloud-based company?

NetSuite is particularly strong on the Enterprise Resource Planning (ERP) front. According to the company, they are the most deployed cloud Enterprise solution in the world, with more than 30,000 companies spread across 160 countries.

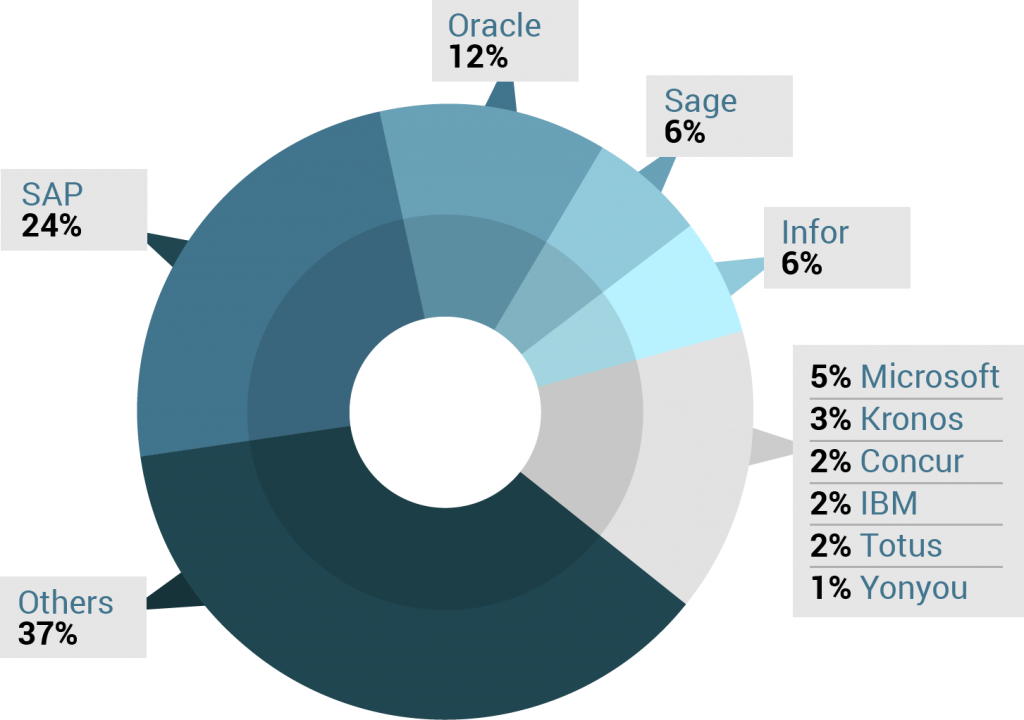

Oracle is already the number two player in ERP after SAP, but they have half the market share than the German software company. The Global ERP market is expected to reach $41.69 billion by 2020 and the only real competitors in this space are SAP and Oracle.

Now that NetSuite has joined hands with Oracle, they have a real shot at closing the gap with the industry leader SAP.

Why cloud-based?

With more and more companies ready to take the cloud route, offering services in the “as-a-service mode” is extremely important, because if you do not do it, someone else is going to. By buying NetSuite, Oracle can make sure that their offerings on the as-a-service model now cover all of their existing clients. That is one of the best ways to prevent market erosion and intense competition. Instead of waiting for someone else to come in and steal them away, Oracle has deftly bought a company that can bridge that gap and keep customers within the family, as it were.

On the CRM front, Oracle is in a head-on collision track with Salesforce, which has literally run away with the market. But Oracle is not going to back down that easily, not when its core businesses continue to decline and it continues to depend heavily on SaaS, PaaS and Cloud growth for its future.

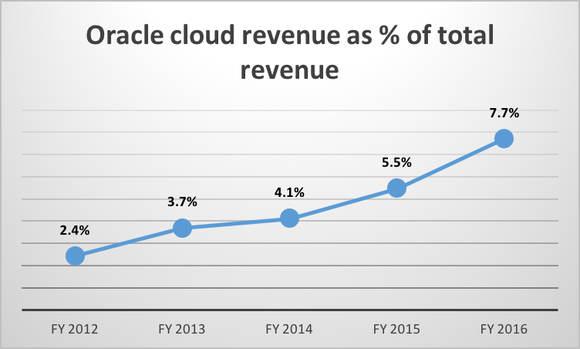

Cloud, SaaS and PaaS revenue for the 4th quarter was $691 million, up 67% from last year, Cloud Infrastructure-as-a-Service (IaaS) revenue was 169 million, up 8% and total cloud revenue for the quarter was $860 million, up 50% from last year.

Oracle expects their SaaS and PaaS revenue to exceed the dollar declines in new software licenses in fiscal 2017 and the company expects its overall sales to start growing from this year.

Lawrence Ellison, from second quarter  earnings call (bold text by author):

“We would like to accelerate our SaaS and PaaS growth and make sure we’re at least double, growing at least double the rate of our closest competitors. And we think we have a fighting chance to be the first SaaS company to make it to $10 billion in revenue.

We’re a major player in ERP and HCM. We’re almost the only player in supply chain and manufacturing. We’re the number one player in marketing. We’re very competitive. We’re number one – tied for number one in service. And we compete against Salesforce.com and sales automation. But in all of these areas, we compete on Salesforce.com, which is the largest SaaS company is really focused on sales automation and some of the other customer experience aspects. They just bought Demandware. They are making acquisitions. They are growing their business, but they are in the customer experience sales area.

They don’t compete in the largest category, which is ERP, also not HCM, again supply chain and manufacturing again and we think that gives us a huge advantage that our footprint is wider. And some of these mid-market companies can simply get in all Oracle footprint run their entire enterprise in the cloud on Oracle. That is something that Salesforce can’t offer and we think that’s going to service very well and allow us to keep these very high growth rate, while we go for that to be first at $10 billion, okay that’s one thing. So we want to be one in number one. We think we need to be number one, we think we will be number one in SaaS and PaaS.”

As Larry Ellison says, ERP is indeed a huge market and their nemesis Salesforce is not there yet. Now, with Netsuite, we can expect Oracle to stay ahead of the curve and possibly retain their position in the ERP market, while inching closer towards breaking SAP’s dominance.

ERP and HCM are indeed Oracle’s strong areas on the software side and Oracle is now utilising their dominant position in both areas to accelerate their cloud business. Oracle seems to have plan to become the first SaaS company in the world to hit that elusive $10 billion mark. There is no doubt in my mind that they will be able to do it, but the road ahead is long and arduous and their vision will not see the light of day until the end of the 2017 fiscal year. That will be the time their stock really makes some fancy moves, as the company completes its transition from a software and hardware provider to a cloud services provider.

Disclosure: I have no positions in any stocks mentioned and no plans to initiate any positions within the next 72 hours.

Start a free 7-day trial of Premium Membership to GuruFocus.