In my opinion, Costco (COST, Financial) is the one retailer that has the ability to withstand any onslaught from the online retailer players - even major ones like Amazon (AMZN, Financial). The reason is that their entire consumer base is built on memberships and that contributes to customer loyalty. Not only does this allow Costco to keep its rates low, but it also gives them one of the highest membership renewal rates in the industry.

Once you are Costco-ed, you are forever Costco’s.

What’s the Problem with Costco?

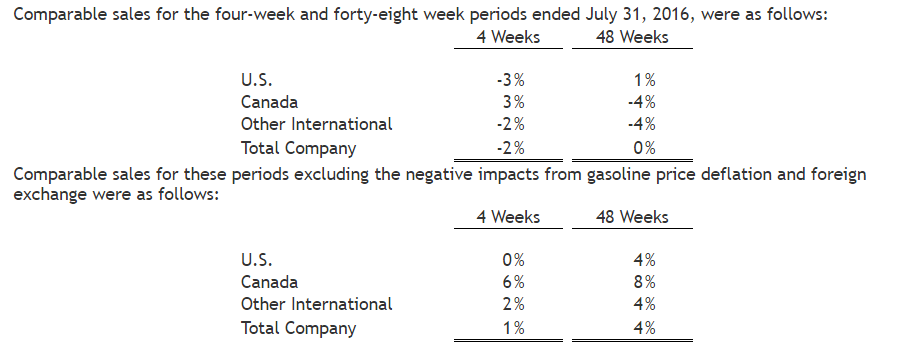

Though the overall stock price trend is upwards, Costco’s stock has barely kept its head above the water and the stock has returned a mere 4.58% since the start of this year. A still-strong U.S. dollar, food deflation and lower gasoline prices have hurt the company’s same store sales growth, which steadfastly remained positive since 2010 before starting to edge lower in the last four quarters.

To be fair, had any other company reported flat same store sales for a forty-eight week period, the stock price would have taken a serious hit. Costco has actually moved up a bit, thanks to the company’s sales numbers doing well when gasoline impact is excluded.

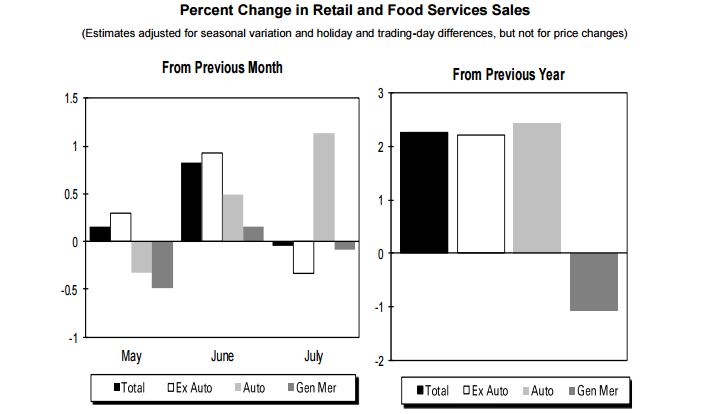

Another point to Costco’s credit is that although overall U.S. retail sales were flat for the month of July, after staying positive during the April to June period, Costco has done a lot better than the market on the store sales front, as most of the downside pressure actually came from lower gasoline prices and stronger U.S. dollar.

Despite the trouble on the gasoline price front, sales have been chugging along, with the company reporting a 2.13% increase in the first three quarters of this fiscal compared to last year. Costco opened 19 new warehouses during this period and the company is planning to open 29 new locations, 21 of those in the United States. The new stores will obviously help boost their top line as well as the bottom line, thus providing a nice cover for their same store sales.

“Last month, the U.S. Department of Agriculture updated its food price outlook for 2016 and predicted the cost of food at home would edge up 0.25 percent to 1.25 percent. That compares with 1.2 percent food-inflation rate in 2015 and the 20-year historical average of 2.5 percent.”

- CNBC

With the U.S. going through a period of food deflation, it is really hard to see Costco’s same store sales getting back to pre-2015 levels. Moreover, oil prices might linger around the current levels for much longer and, to make matters worse, the dollar is expected to remain strong as well, forcing Costco’s sales growth to be entirely dependent upon their store expansion.

For investors, that is not a terrible thing. It gives you a chance to load up on COST over the next four months of the calendar year 2016. Do not expect the stock to do amazingly well thereafter because it will take time for comps to recover in this kind of macroeconomic scenario. But do expect gains in a couple of years from now, when online retail has done the worst to brick and mortar stores and Costco is still left standing strong on its memberships.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

Start a free 7-day trial of Premium Membership to GuruFocus.