The world’s largest payments processor continues to grow to this day. New age companies such as Apple (AAPL, Financial), Samsung (XKRX:005930, Financial), Google (GOOGL, Financial) and PayPal (PYPL, Financial), who could have disrupted the payments industry, have already fallen in line and accepted Visa’s control over the payments market, thus making sure that Visa’s moat remains impenetrable in the near future. But with more than $13 billion in annual revenues, does Visa warranty a $172 billion dollar valuation, almost 14 times its sales? The market seems to be expecting the the company to keep growing at double-digit rates, but how possible will that be for a company that saw its sales grow by 9.27% last year?

Visa’s Position in the Payments Industry

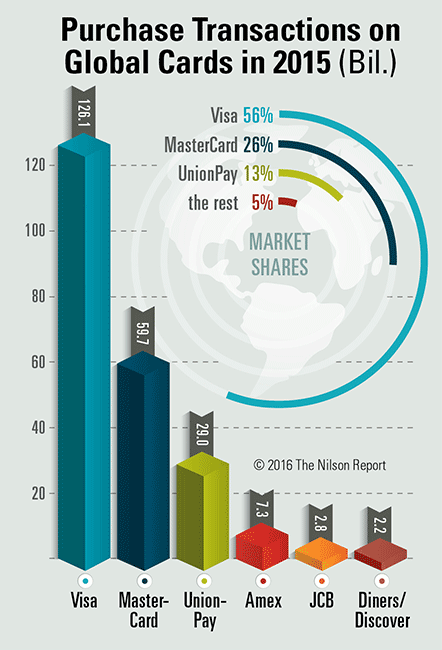

Visa sits at the top of the global electronics payments market, accounting for more than half the transactions around the world in 2015, while MasterCard (MA, Financial) ranks a distant second with less than half of Visa’s volume.

Perhaps PayPal, which is expecting to hit more than ten billion in annual revenues, was the one company that could have disrupted Visa’s future, but even they have recently agreed to work with Visa due to the combined threat posed by tech companies in the digital wallet space.

With the near-term future of the payments master of the world secure, we still want to know if Visa deserves a near 14 times sales valuation.

Where is the Growth Potential Going to Come From?

Visa’s biggest potential comes from the cash-based economy that still accounts for the bulk of transactions around the world. One might have thought that developed nations were mature enough that only a small portion of all transactions would be cash-based. That is not the case, however. The BBC reported last year that 48% of all payments - whether made by consumers, businesses or even financial firms - were still in cash.

Source: BBC

The United States also has a significant volume of cash transactions in the country.

“In October 2012, the average American consumer had 59 transactions, including purchases and bill payments, and 23 of these 59 payments involved cash.” Frbsf.Org

The transition from a cash society to a cashless one is obviously not something that will happen overnight, but it is inevitable. Now add to that the potential of developing nations like India and China and it is obvious how long of a runway for growth Visa still has. As the dominant player in the space, they have the resources to be aggressive in capturing market share.

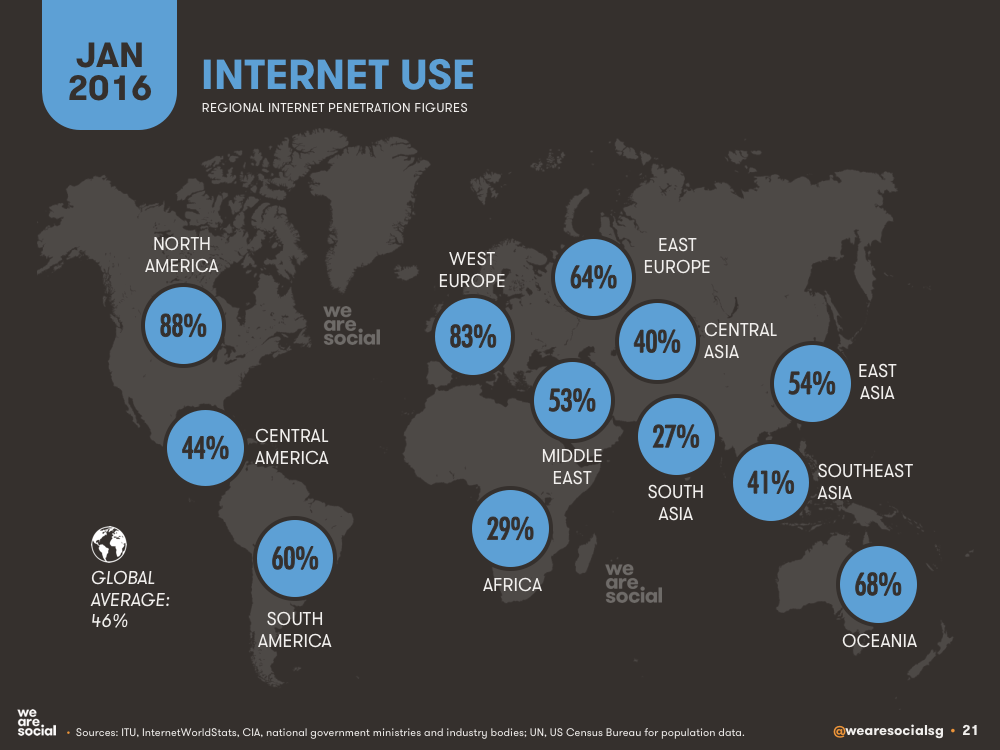

Another combination of factors is internet connectivity and the growth of e-commerce. As internet penetration grows in these regions, more and more people will be introduced to electronic payments, thus expanding the potential market for Visa. Take a look at the Asian and African markets and you will see what I mean.

My Take on Visa

As such, the company still has lot of ground to cover in the developed markets, but when you throw in developing countries as well, the runway Visa has is huge.

I believe Visa can and will grow steadily over the years, but at near 14 times price to sale valuation and 22 times forward earnings, most of the upside seems to be priced in, leaving very little margin for error. I love the company, but I am not able to recommend the stock at this price point.

That said, this is a company that every investor should have in their portfolio, so the best approach would be to buy small amounts of stock during dips and do it over a period of time so your cost basis is kept low and your returns keep growing.

Disclosure: I have no positions in any of the stocks mentioned above and no intention to initiate a position in the next 72 hours.

Start a free 7-day trial of Premium Membership to GuruFocus.