One of David Einhorn (Trades, Portfolio)’s new positions is Amaya (AYA, Financial).

Previously, the company had its main listing on the Canadian Exchange before transferring to the U.S.

Amaya’s main asset is the leading online poker room, Pokerstars. In online poker, there is a network effect and there are clear advantages to being number one in the market. It is not just that the room with the most players has the most liquidity or games available, but Pokerstars gets the most players together for its tournaments. That leads to these tournaments being able to advertise the largest prize pools. These prize pools attract more players, which leads to larger prize pools. It takes a lot of marketing spent to break that vicious cycle.

Unfortunately, online poker is in something of a rut. All over the world, governments have cracked down on the market to various degrees (Black Friday in the U.S. is a notable event) and only slowly the process of overly strict regulation has reversed. Meanwhile, the economy took a decided turn for the worse, which helped end the poker boom.

A bit of a history lesson will help to understand the transformation Amaya is currently undergoing, which is the basis for Einhorn’s interest.

The previous owners of Pokerstars kept running the poker room when the U.S. made it clear it did not want its citizens to play on online offshore rooms, or at least not deposit money there. Pokerstars kept taking in U.S. citizens and their money, one of the few rooms to do so, and that decision turned it into the clear leader. However, they did so with a very clean poker client. Clean in the sense it did not offer any other gambling options. Almost all poker rooms have integrated casino games and often also sportsbooks. By keeping its product clean and focused on poker, it thought it could continue to operate in the U.S.

That all fell apart, forcing the previous owners to sell the company. The sale immediately made the company more valuable because with the previous owners gone, Pokerstars' prospects for re-entering the U.S. market became a lot brighter.

Meanwhile, the years have passed and Amaya is back in the U.S. with a poker product in some states and a Fantasy Sports product. The company also recently integrated a sportsbook into its client (depending on jurisdictions) and it now benefits from the same cross-selling opportunities from which its competitors benefited.

It is the sportsbook and Fantasy Sports product called BetStars and StarsDraft in which Einhorn is particularly interested. The company is not really cheap nor expensive when you consider its core operations and strong competitive advantage.

However, the BetStars product is going to show good growth for many quarters to come, as poker users get used to the product and maybe even move existing sportsbook bankrolls over from competitors (where they were previously forced to play). The StarsDraft product is not going to dominate the fantasy sports market right away, but the company should realize a very strong role on it. Previous CEO Baazov said on an earnings call:

“I’d also emphasize that this is not a category in which we will be doing any significant investment in, as they first start cross-selling and leveraging the 1 in 10 U.S. adults we have in the database. And I think the market still has to mature more; it has to appreciate to a size where we would be willing to make a significant investment.”

Meaning, by just buying the existing DFS platform Victiv and leveraging the email databases of both Pokerstars and Full Tilt Poker, rooms that virtually divided up all U.S. market share of online poker players, the firm should be able to grow that segment extremely quickly.

It is just amazing how attractive it is to have DraftKings and FanDuel throw hundreds of millions, if not billions, of dollars at ESPN ads and sponsorship educating the market about DFS, while Amaya just buys a cheap competitor with a great website and can start emailing about the entirety of the U.S. population that has any interest in what I will call “online skill-based gambling” –Â even though that seems somewhat of a contradictus interminus, it really is not.

What firm would you value higher, a company that needed to spend hundreds of millions, or billions, of dollars on ESPN ads to remain leader or runner-up in the space or a firm that has the strongest brand in “online skill-based gambling” and can market at virtually no incremental cost while cross-selling a product in various states?

Truth is, StarsDraft does not have the traction DraftKings or Fanduel has. In fact, Amaya has chosen to offer real money play only in New Jersey, Massachusetts, Kansas and Maryland. This time around, Amaya wants to remain in good standing with U.S. regulators, clearly having learned its lesson. However, the potential to win big in this space is cleary there.

From Investopedia on DraftKings valuation:

A recent undisclosed DraftKings funding round led by new investor Revolution Growth reportedly places the company at a substantial discount valuation in comparison to last summer’s $2 billion post-money valuation while still multiples above the company’s valuation at the end of 2014. While both DraftKings and FanDuel are worth over $1 billion, it may be true that the fantasy sports leagues are facing a slight downturn in light of valuation discounts.

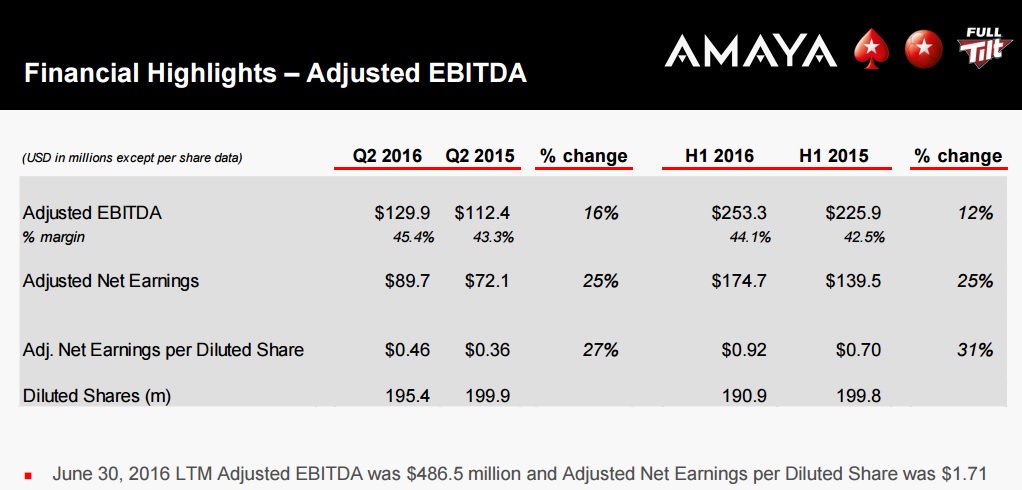

If DraftKings and FanDuel are worth over $1 billion, while mostly spending money and StarsDraft holds very promising cards in this market, owns the biggest most successful platform in a space where the network effect is important, generated 46 cents of adjusted earnings in USD per diluted share last quarter:

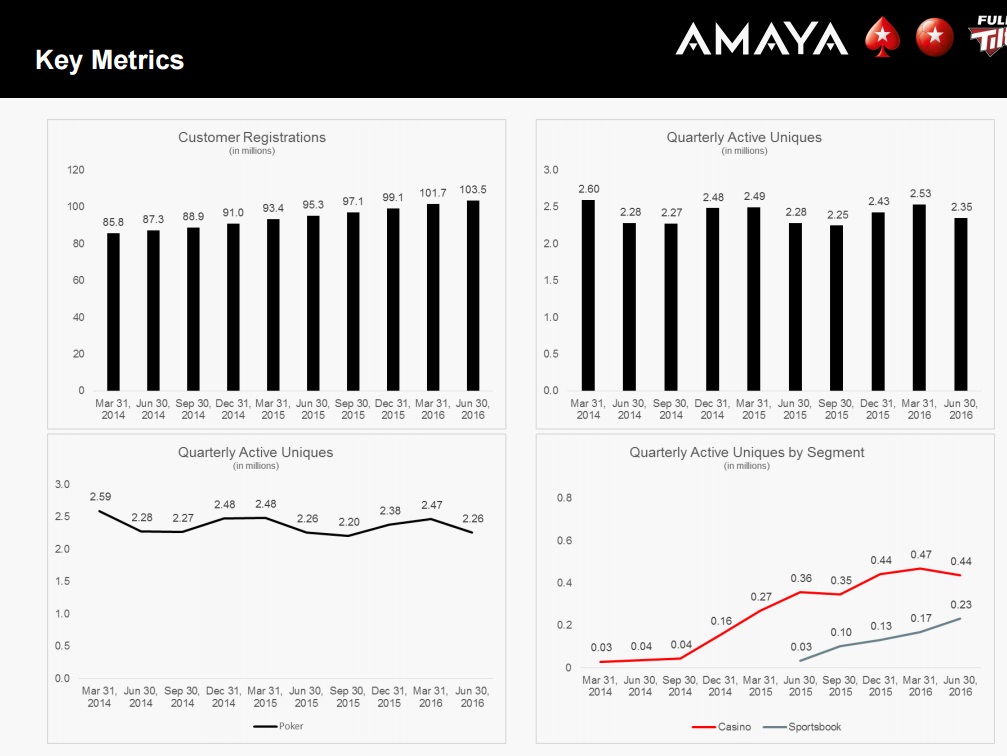

And has only recently started cross-selling a Sportsbook offering to its 100 million registered users:

Would it surprise you to learn the market cap of Amaya is only $2.26 billion? It certainly is surprising to me. I bought Amaya Gaming shares quite a bit higher and am now contemplating if I should expand it into a relatively very large position. GuruFocus provides the fundamentals in an easy format and they are certainly attractive enough (especially PFCF and POCF):

If I can give one takeaway, it is that Amaya gaming is not super cheap or super expensive on an as-is basis. However, there are clear catalysts that could unlock tremendous value for Amaya shareholders; 1) All U.S. states adopting clear poker regulations that at least allows Amaya into the market, 2) U.S. states arriving at a clear regulatory stance towards DFS and, 3) the Sportsbook expansion to continue. At the current share price we are paying a fair price for operations, but getting these upside options thrown in for free.

Disclosure: I own shares.

Start a free 7-day trial of Premium Membership to GuruFocus.